Why gray divorce is rising among older Americans

Gray divorce is rising because longer lives, greater financial independence, and changing expectations are making late-life marriage less permanent. The cost can be severe, especially for retirement security, housing, and caregiving.

Gray divorce is no longer a niche family story. Among Americans 50 and older, the divorce rate roughly doubled from 1990 to 2015, and among those 65 and older it roughly tripled, signaling a broad shift in how later-life marriage works. The trend is tied less to sudden lifestyle change than to structural forces: people live longer, women have more financial independence, and many couples now see marriage as something that must remain fulfilling, not merely enduring.

The rise is real, and it cuts across older age groups

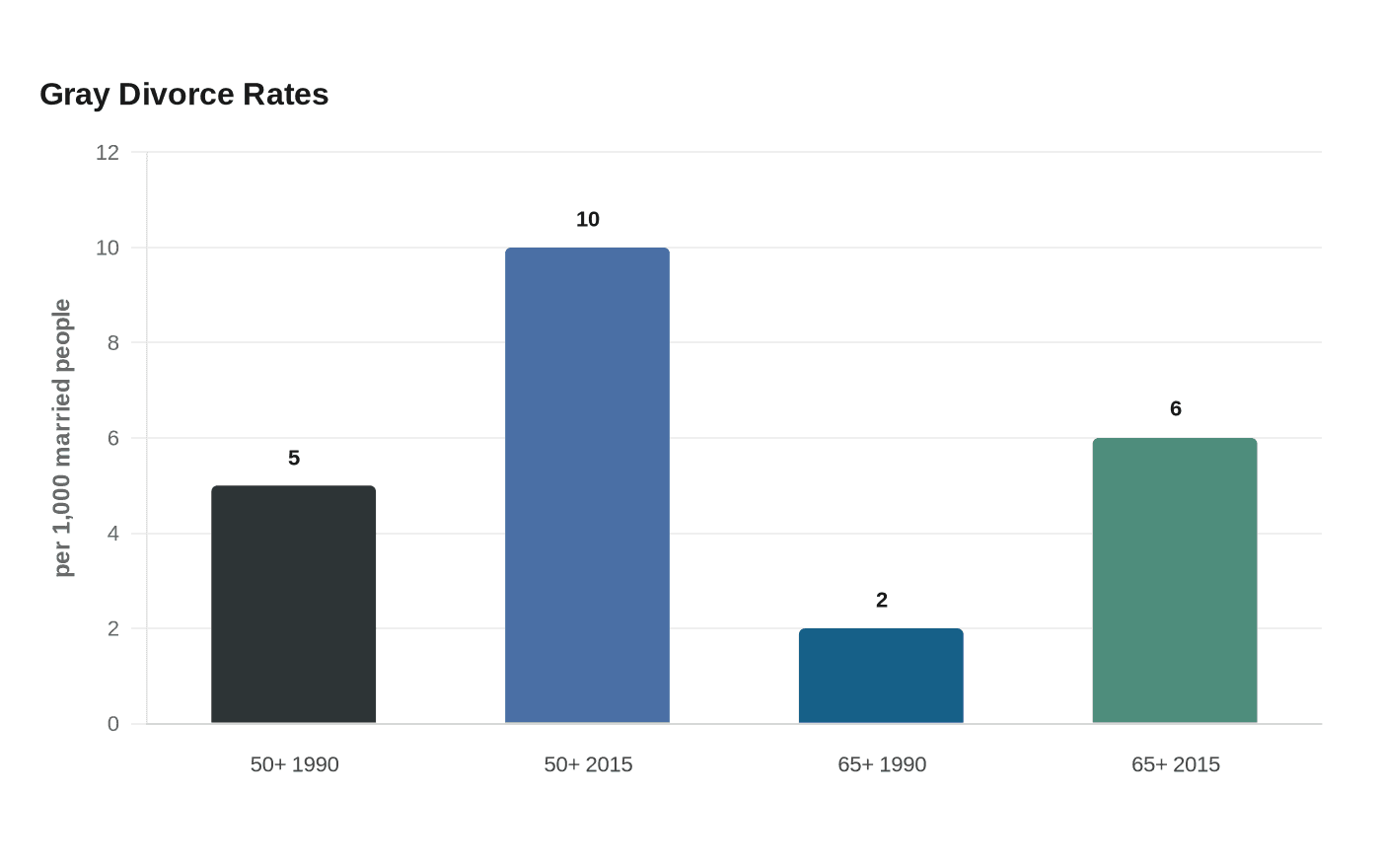

Pew Research Center’s 2017 analysis found that the divorce rate among married adults age 50 and older rose from 5 divorces per 1,000 married people in 1990 to 10 per 1,000 in 2015. For adults 65 and older, the rate climbed from 2 to 6 per 1,000 married people over the same period. That is a sharp reversal from earlier decades, when divorce was far more concentrated among younger adults.

The pattern did not stop there. Bowling Green State University’s National Center for Family & Marriage Research reported that divorce rates for people 45 and older continued rising through 2021, while rates for people under 45 fell. The same center found that the share of divorced adults age 65 and older increased from 5.2 percent in 1990 to 15.2 percent in 2022, and researchers estimate that about one in 10 people divorcing in the United States today is 65 or older.

The Centers for Disease Control and Prevention’s provisional 2023 data show an overall U.S. divorce rate of 2.4 per 1,000 population in the 45 reporting states and the District of Columbia. That figure does not break out gray divorce by age, but it reinforces a larger point: later-life divorce is growing even as national divorce totals are measured across all ages.

Why older couples are more likely to split now

Several long-term changes help explain the rise. Longer life expectancy matters because a marriage that once seemed like a lifetime commitment can now stretch across 20 or 30 years of retirement. Empty nest years also change the calculus. When children leave home, some couples discover that the relationship they built around parenting no longer holds together as strongly.

Academic studies using Health and Retirement Study data have specifically examined empty nest, retirement, and poor health as life-course turning points linked to gray divorce. Those transitions can reshape daily routines, finances, and emotional dependence all at once. Retirement can remove one of the few shared structures that kept a marriage together, while poor health can intensify stress, caregiving burdens, and disagreements about how to spend time and money.

Women’s financial independence is another major factor. More women now have the earnings, savings, and confidence to leave unhappy marriages later in life after children are grown. That shift has changed the power balance inside many households and made divorce more feasible, even if it is still difficult. Baby Boomers, born between 1946 and 1964, are a major driver of the trend as they move deeper into later life with different expectations about marriage than previous generations had.

The pattern also reflects inequality. Researchers have found that gray divorce is especially likely among couples who are socially and economically disadvantaged. When income is tight, health is fragile, and retirement savings are thin, the pressure points that strain a marriage can multiply quickly.

The financial hit after 50 can be steep

The most immediate consequence of gray divorce is financial. AARP reports that after-divorce standard of living falls by an average of 45 percent for women and 21 percent for men when divorce happens after age 50. That drop is not just about monthly income. It reflects the fact that one household becomes two, while retirement assets, housing equity, and everyday expenses still have to be split.

Retirement savings are often the centerpiece of the problem. Pension income, 401(k) balances, Social Security planning, and investment accounts may all need to be divided or renegotiated. For many couples, there is less time left to rebuild what is lost, which means a divorce in the late 50s or 60s can permanently alter retirement security.

Housing is another pressure point. A home that once supported one married couple now has to be maintained by two separate households. One spouse may need to downsize quickly, rent instead of own, or relocate to stay within budget. That can have ripple effects on neighborhood ties, access to family support, and the ability to age in place.

Caregiving can also become more complicated. Later-life marriages often sit at the center of plans for medical support, transportation, and daily help. When the marriage ends, the informal caregiving arrangement can disappear too, leaving one or both spouses to rely on adult children, paid aides, or friends who may not be able to fill the gap. In practical terms, divorce after 50 often means not only dividing assets but rebuilding the entire support system around aging.

What the trend says about marriage and aging

Gray divorce is important because it reveals how older Americans are redefining marriage in real time. The rise does not mean marriage is becoming less common overall, and divorce is still more frequent among younger adults. But the jump among people 50 and older shows that later life is no longer a period when couples simply stay together by default.

For policymakers, planners, and families, the lesson is straightforward: later-life divorce is now part of the mainstream aging landscape. That means retirement planning, housing policy, and elder support systems have to account for a growing number of people who enter old age alone after decades of marriage, with fewer assets and more fragility than they expected.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip