Workers Scaled Back 401(k) Savings in 2023 as Costs Squeezed Budgets

An affordability crunch pushed nearly 20% of full-time workers to tap 401(k) loans in 2023, while middle-income savers quietly lost ground and employer match dollars went uncollected.

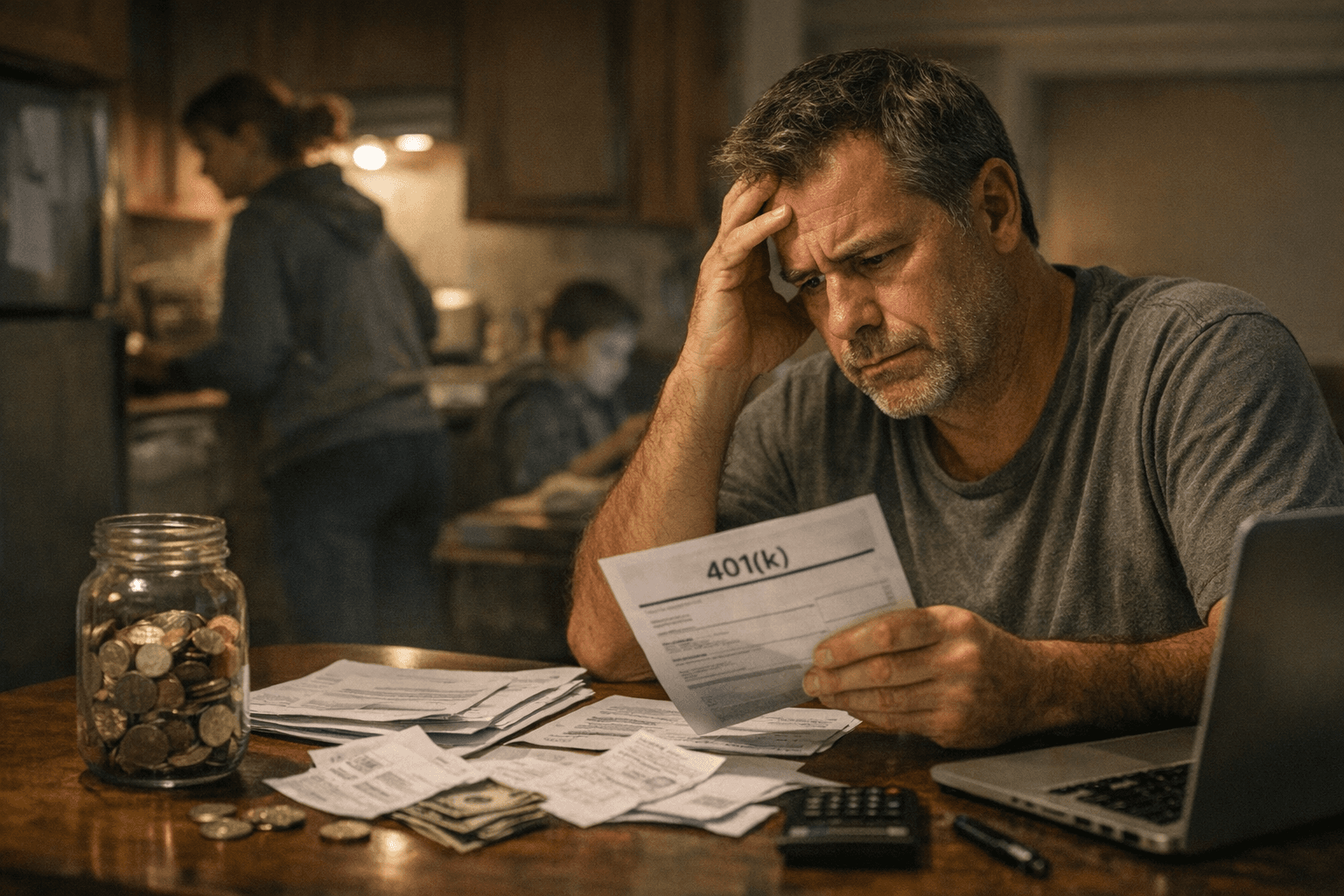

The cost of daily life crowded out retirement savings in 2023 at a scale that could reverberate for decades. Nearly 20% of full-time workers tapped their 401(k) plans for loans that year, the highest share ever recorded by human capital management firm Dayforce, whose analysis of 1.2 million employee records traces the retreat in saving from 2021 through 2024.

The overall 401(k) participation rate fell from 66% in 2022 to 63% in 2023, according to T. Rowe Price. While three percentage points may sound modest, it translates into millions of workers no longer directing payroll dollars into tax-advantaged accounts, and in many cases forfeiting employer matching contributions they will not recover.

Middle-income earners absorbed the hardest hit. For workers making between $15,000 and $50,000, the average annual retirement contribution shrank from $1,918 to $1,815, and their savings rate as a share of income fell from 4.9% to 4.6%. Workers earning $50,000 to $100,000 saw average contributions drop from $6,814 to $6,630, and savings rates slipped from 9.6% to 9.3%. The only income tier to improve was earners above $150,000.

"Nearly all of those gains have gone to higher-income workers," said Jason Rahlan, Dayforce's global head of sustainability and impact. "This should be a warning sign," Rahlan said. "It may be a sign of financial strain," pointing to workers setting aside retirement goals to focus on more immediate budget pressures.

Matt Bahl, vice president for workplace financial health at the Financial Health Network, put the dynamic plainly: "When you are struggling day to day, it's hard to focus on your long-term goals. We're really seeing the crunch for those middle-income earners. It speaks to the affordability crisis."

Total retirement plan contributions and savings rates declined for most employees regardless of their age, including baby boomers, Gen Xers and millennials, Dayforce found. Gen Z was the notable exception, with participation climbing from 64% to 68.7% since 2022, and total contributions rising 24%. Researchers attribute those gains partly to auto-enrollment defaults that activate before young workers have the chance to opt out in a tight month.

Among 401(k) plans with automatic enrollment, participation reached 83%, compared with just 36% in plans without it, according to T. Rowe Price. That gap points to the single most accessible protection for workers whose budgets are under strain: if an employer auto-enrolls at even a 3% deferral rate, the worker captures the full employer match without having to make an active decision during a financially stressful period. Allowing contributions to fall below the match threshold converts a short-term cash-flow choice into a permanent wage reduction, as the foregone employer dollars and compounding returns cannot be retroactively recaptured.

Hardship withdrawals also set records in 2023. Vanguard reported a record-high 3.6% of its plan participants took such withdrawals, up from roughly 2% before the pandemic. Unlike loans, hardship withdrawals are not repaid to the account, making them an irreversible reduction in retirement wealth and, for workers under 59 and a half, a taxable event subject to a 10% early withdrawal penalty.

About half of Americans reported feeling more financially stressed heading into 2026 than a year earlier, with covering day-to-day expenses cited as the biggest source of concern, according to a December study from Allianz Life. Rahlan and Bahl both said the retreat from retirement saving is unlikely to reverse without broader adoption of auto-enrollment and employer financial wellness programs designed to help workers manage near-term costs without dismantling the accounts they depend on most.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?