Yale study says closing carried interest loophole could raise billions more

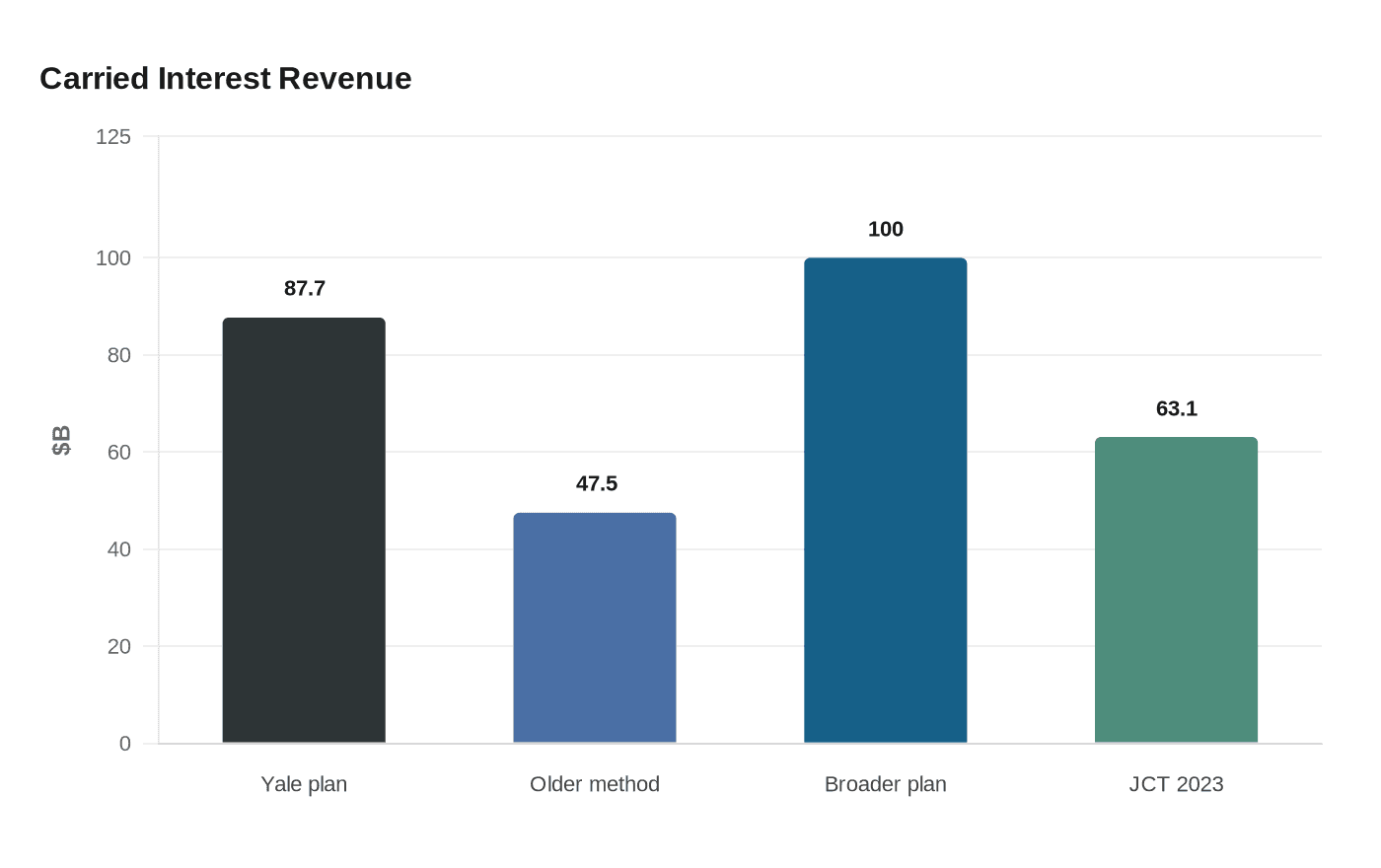

Yale researchers said taxing carried interest more like ordinary income could raise $87.7 billion over 10 years, far above older estimates. The new figure could intensify a two-decade fight over a Wall Street tax break.

The tax fight over carried interest just got a lot more expensive. Yale’s Budget Lab said closing the loophole could raise far more revenue than lawmakers and analysts had previously estimated, giving new momentum to a debate that has shadowed Washington for nearly two decades.

In an analysis released May 4, the Yale team estimated that a version of the proposal backed by Sen. Ron Wyden, Sheldon Whitehouse and Angus King would bring in $87.7 billion over 10 years. Under older methods, the same plan had been scored at just $47.5 billion. The lab also said a broader carried-interest proposal could generate $100 billion over a decade, and that President Biden’s carried-interest plan would yield about three times more revenue than earlier estimates suggested.

The numbers matter because carried interest sits at the center of how private equity and venture capital firms pay their top managers. In a typical structure, managers receive an annual management fee of about 2% of invested capital and carried interest equal to roughly 20% of fund income. Buyout firms often require an 8% hurdle rate before managers can collect carry. That compensation is generally taxed at long-term capital gains rates, not ordinary income rates, a preference critics have long called unfair.

The Senate Finance Committee introduced the latest bill to close the loophole on April 16, with Wyden, Whitehouse and King arguing that hedge fund managers and private equity CEOs should pay their fair share. The measure, later referred to the committee, already had a bipartisan-like cluster of Democratic cosponsors. The Joint Committee on Taxation had estimated in 2023 that the bill would raise $63.1 billion over 10 years, meaning Yale’s new estimate would mark a sharp upward revision.

The broader political stakes are obvious. Lawmakers pushing the change say the money could help reduce the deficit and make the tax code less tilted toward wealth over wages. Private equity firms, which rely on carried interest as a core part of compensation, have every reason to resist a higher score that strengthens the case for ending the preference.

The split between Yale’s estimate and earlier scores also raises a deeper question in the policy fight: whether the disagreement is really about methodology, or about preserving a lucrative tax break that has survived repeated attacks, including from Donald Trump during his first presidential campaign. For supporters of the change, the answer may not matter much. A bigger revenue estimate makes the loophole harder to defend and easier to target.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?