Biofuel economics make rapeseed more attractive than soft wheat

German rapeseed forward contracts reached just under €492 a tonne, widening the wheat spread to 1:2.7 and tilting acreage toward oilseeds.

Rapeseed's premium over soft wheat has widened enough to steer German planting decisions, with growers receiving just under €492 per tonne ex farm on forward contracts for the 2026 crop at the end of May. Biofuels International said the spread between soft wheat and rapeseed forward prices had stretched to 1:2.7, making winter rapeseed the stronger cash option for farmers planning the 2027 harvest.

The move came after energy prices rose on geopolitical tensions in the Middle East, lifting Paris futures and giving rapeseed an extra bid. The rally was described as short-lived, and the underlying supply picture has not turned tight, but the price relationship still favors oilseeds over soft wheat for many growers. A year earlier, early May 2025 rapeseed forward contracts in Germany were around €443 per tonne, underscoring how much the planting incentive has improved.

That matters far beyond the farmgate. UFOP said USDA Foreign Agricultural Service analysts in Vienna estimated EU rapeseed area for the 2026 harvest at 6.3 million hectares, up about 2.7% year on year, with France, Germany, Poland and Romania accounting for roughly three quarters of EU production. Rapeseed also fits cereal-heavy rotations as a break crop, so the stronger forward curve is doing more than rewarding one season of volatility, it is reinforcing acreage choices before a litre of fuel is made.

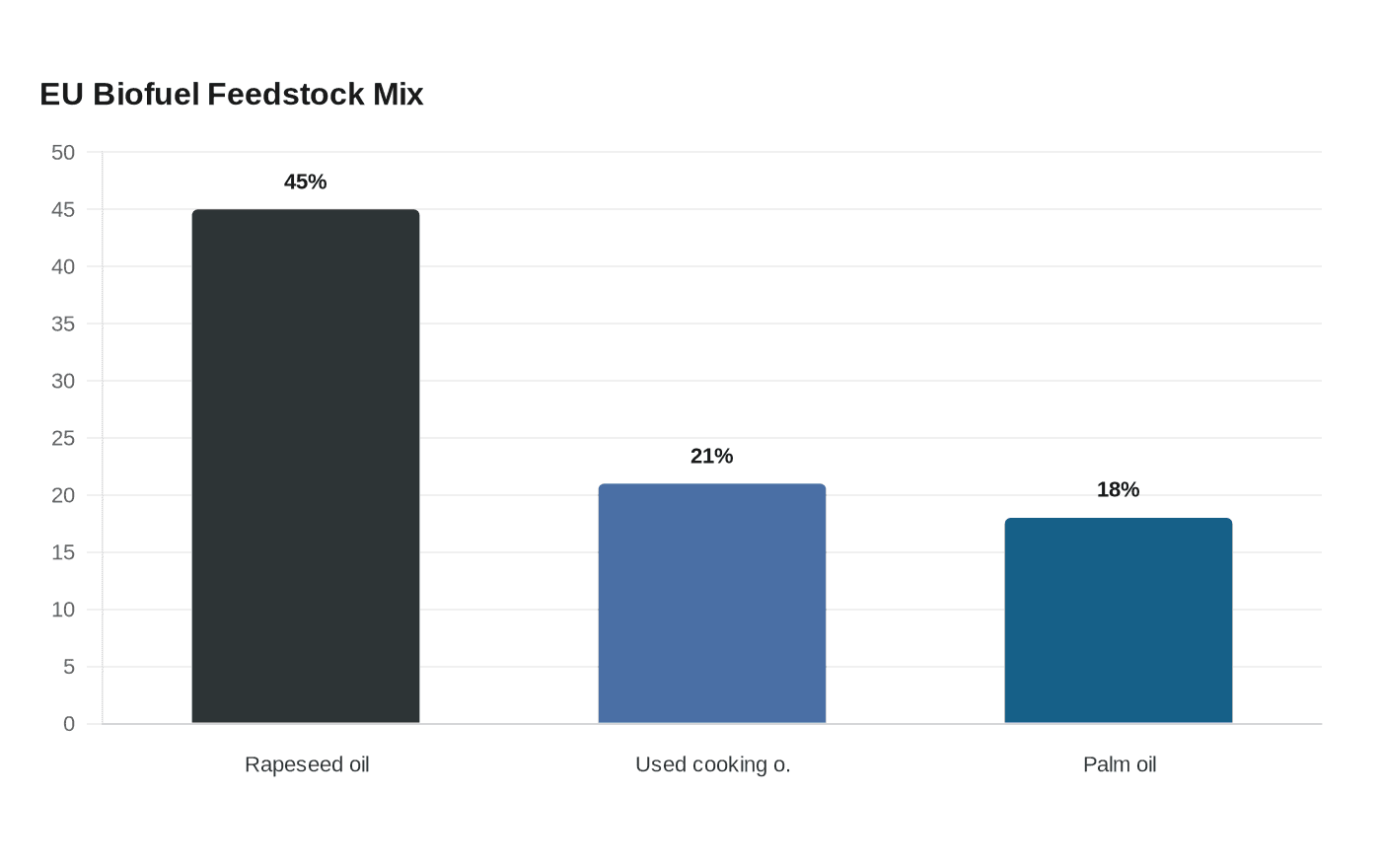

The downstream pull remains structural. UFOP’s supply report said rapeseed oil accounted for 45% of EU biodiesel and HVO production in 2024, even as total biodiesel and HVO output fell 2.8% to 15 million tonnes. Used cooking oil held a 21% share, while palm oil slipped to 18% after quota-credit exclusions in some member states, including France and Germany. The revised Renewable Energy Directive, RED III, now requires at least a 14.5% cut in transport-sector greenhouse gas emissions or a 29% renewable-energy share in road and rail transport by 2030, plus a 5.5% sub-target for advanced biofuels and renewable non-biogenic transport fuels.

The market is not signaling outright shortage. New domestic business has been limited, with warehouse clearing and contract fulfilment dominating activity, while USDA expects EU oilseed production in 2026/27 to rise on high rapeseed and sunflower output. CME Group said European rapeseed oil demand is about 10.1 million tonnes in 2025/26, with biofuels accounting for roughly 60% to 65% of that market. For traders and crushers, the message is clear: the current spread looks like a real planting signal, but its durability still depends on energy, policy and the next crop cycle.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip