ACORD standards bridge batch and real-time data in P&C insurance

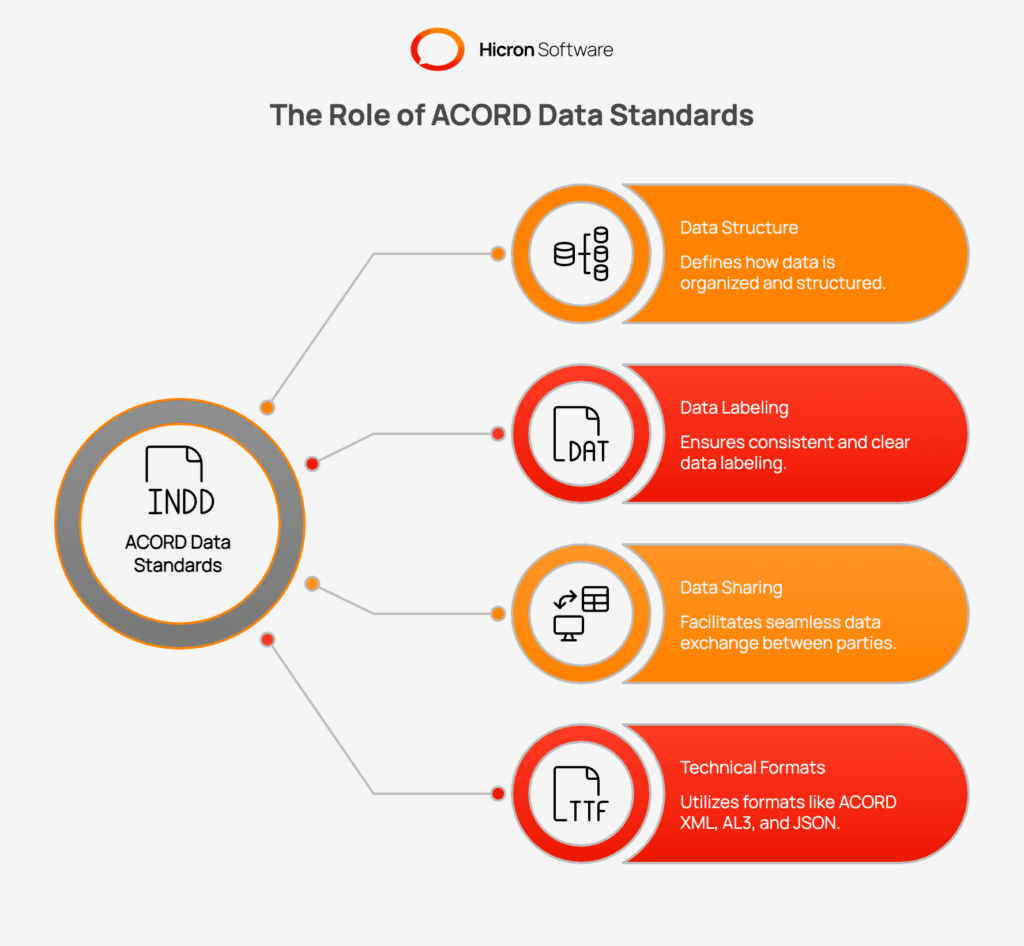

ACORD still matters because it decides whether P&C systems exchange clean data or just rekey it. AL3 handles batch, XML handles real time, and APIs extend the same logic.

AL3 is built for one-way, batch communication of policy and commission data, while XML is built for real-time request-and-response transactions. The cleanest digital transformation in P&C insurance starts with data plumbing, not a glossy interface. ACORD’s standards sit underneath the workflows that carriers, MGAs, brokers, and vendors depend on, and the difference between batch-era AL3 and real-time XML still shapes how quickly a platform can move policy, commission, claims, and delegated authority data without rekeying.

Batch and real-time are not the same problem

That split matters because too many software projects modernize the screen layer first and leave the integration layer translating old forms and old message types behind the scenes.

In practice, the distinction shows up in ordinary work. Submission intake can still arrive as a batch file from a broker. Policy issuance may need a real-time response before a quote moves forward. Endorsements often need both speed and precision, because one bad field cascades into billing and downstream servicing. Claims FNOL has the same problem: if the loss notice is not mapped cleanly, the workflow slows down immediately. ACORD’s standards give carriers and trading partners a common structure for those exchanges instead of forcing every implementation to invent its own translation layer.

The standards have moved beyond legacy messaging

ACORD does not stop at AL3 and XML. Its next-generation digital standards are granular and transaction-centric for APIs, microservices, IoT, and other modern architectures. The market keeps talking about open ecosystems while still tripping over old message formats when a policy admin system needs to speak to a broker portal, a claims platform, or a third-party service.

XML did not disappear. ACORD’s standards now stretch across the full modernization stack, from batch exchange to API-driven services. In P&C, a carrier may buy a modern front end and still discover that the back end cannot reliably map ACORD fields across policy, billing, claims, delegated authority, and workers’ compensation workflows.

Where the standards show up in actual insurance operations

ACORD’s P&C standards are used in delegated authority and workers’ compensation as well as core policy workflows. Delegated authority programs live or die on fast, accurate exchange between carriers, MGAs, brokers, and wholesalers. Workers’ compensation adds another layer of operational friction, because the data has to survive long-lived policies, endorsements, billing changes, and claims handling without drifting.

The standards are also tied to the documents people still touch every day. ACORD’s first P&C forms arrived in 1971: ACORD 1 Property Loss Notice and ACORD 2 Automobile/Other Loss Notice. ACORD still sits at the junction of forms, fields, and transaction data, and the organization’s forms and standards remain part of the operational fabric rather than a sidecar to it.

Scale is the reason the standards still matter

ACORD says it engages 36,000 participating organizations worldwide across more than 100 countries, that 3 million forms were downloaded over 10 years, and that it processes 275 million message transactions annually.

For buyers, a platform that can exchange ACORD-based data cleanly has a better shot at avoiding handoffs that require rekeying, exception handling, and manual validation. That is true whether the connection is between a carrier and a broker, a managing general agent and a wholesaler, or a vendor and a claims administrator. ACORD’s scale makes it hard for any serious P&C software stack to ignore the standard just because the user interface looks modern.

Implementation support is part of the product

ACORD offers implementation resources, including tools and services to support standards implementation. In insurance software, the value of a standard is measured not only by how it is written but by how it is built into real projects. Implementation guides and construction tools turn a spec into straight-through processing.

During migration, teams discover that the hard part is not the new policy admin system or the prettier portal. The hard part is mapping legacy data, forms, and message types into a shared structure that can survive across policy, claims, billing, and delegated authority. ACORD’s implementation support is designed to reduce the amount of custom plumbing every carrier has to build from scratch.

Governance is what keeps the standard from going stale

ACORD’s standards development process is collaborative and consensus-based, with changes proposed, reviewed, and voted on by members. Its governance materials include electronic voting rules, appeals, versioning and retirement, and antitrust and competition-law compliance.

Carriers, brokers, agencies, MGAs, and wholesalers do not all move at the same pace, and the standards have to survive that tension. ACORD’s process is designed to keep the ecosystem coordinated without freezing the format in place.

The digital maturity gap keeps the pressure on

ACORD’s 2025 Insurance Digital Maturity Study, now in its sixth edition, says only about a quarter of the world’s largest insurers have truly digitalized the value chain. It also says more than half of the insurers it examined are still exploring how digitalization can be applied to their business model. Lots of insurers still have modern interfaces wrapped around old integration habits.

ACORD’s 2026 homepage summary says its study analyzed more than 200 global insurers and found only 7% emerging as true leaders in digitalization.

The distribution conversation is widening

In May 2026, ACORD announced the Inter-Association Advisory Council. The standards conversation remains active and tied to North American distribution channels, not just to internal IT architecture.

ACORD’s membership programs target carriers, brokers, agencies, MGAs, and wholesalers, which is exactly where friction appears when submission intake, policy issuance, endorsements, and claims FNOL have to pass through multiple systems.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip