Convr unveils Risk Context Engine for commercial P&C underwriting

Convr said its new Risk Context Engine is calibrated on a decade of production data and 2,500 sources, aiming to power every AI step in commercial P&C underwriting.

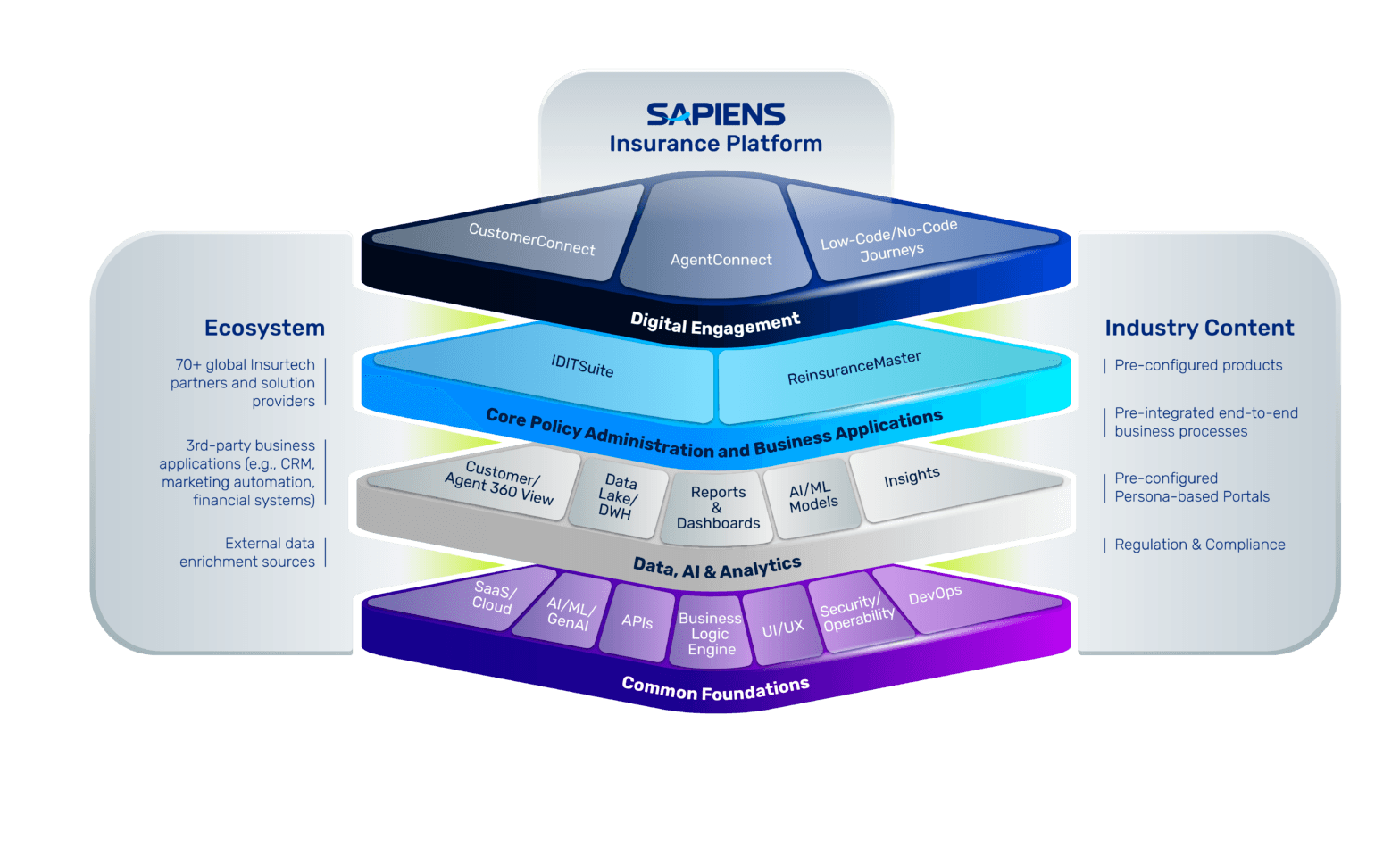

Convr turned its latest AI pitch into a bet on infrastructure, not a feature. The Chicago company unveiled the Risk Context Engine on June 9, 2026, describing it as the first knowledge graph and semantic ontology built specifically for commercial property and casualty underwriting, calibrated on a decade of production data and more than 2,500 integrated sources.

The strategic move is bigger than a product name. Convr is positioning the Risk Context Engine as the layer underneath its AI Underwriting Workbench, with the engine intended to shape the full workflow from intake and business classification to risk scoring, data enrichment and downstream workflow automation. In Convr’s framing, that means underwriting context becomes reusable commercial-lines plumbing rather than a one-off point solution.

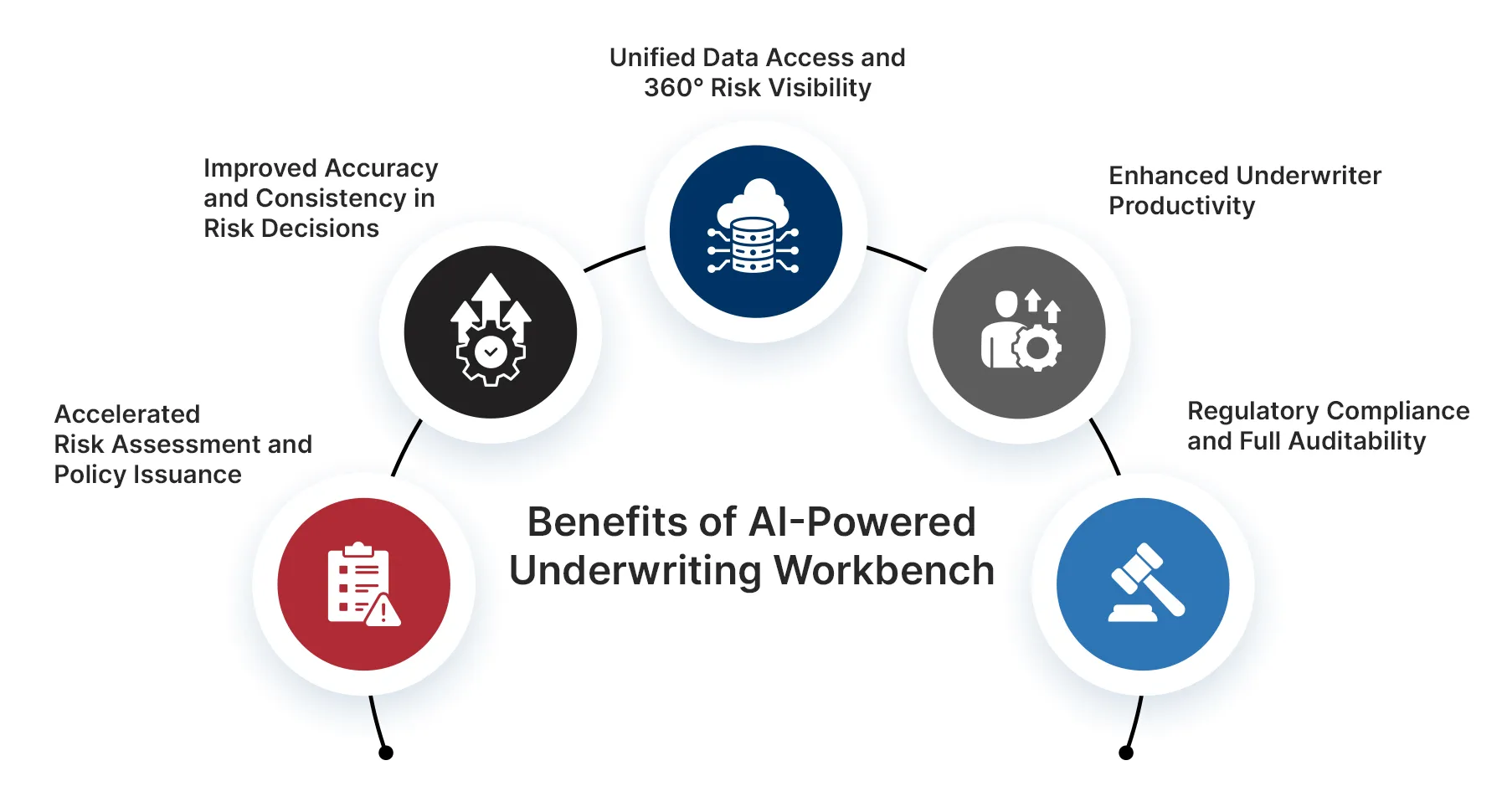

That distinction matters in workflow terms. Convr says the engine powers every AI capability across the workbench and supports carriers, MGAs and brokers, with the goal of helping teams win more business, scale underwriting and accelerate risk evaluation. The company is pushing the idea that context is not just cleaner prefill or faster triage. It is the ability to connect a submission back to source documents, loss data and prior underwriter decisions so that each recommendation can be traced, inspected and reproduced.

That argument lands in a regulatory environment that has made explainability a practical requirement, not a nice-to-have. The National Association of Insurance Commissioners adopted its model bulletin on the use of artificial intelligence systems by insurers on December 4, 2023. New York State Department of Financial Services followed with Circular Letter No. 7 on July 11, 2024, addressing AI systems and external consumer data and information sources in underwriting and pricing. Colorado’s SB24-205 was signed on May 17, 2024, and its high-risk AI requirements began taking effect on February 1, 2026. The Pennsylvania Insurance Department issued Notice 2024-04 on April 6, 2024.

Convr is using that backdrop to make a broader claim about where commercial underwriting software is headed. General-purpose AI can be fast, but Convr argues it can also be inconsistent and hard to reproduce in regulated settings. A domain-specific ontology, the company says, gives carriers and MGAs a grounded foundation for decisions that can stand up to compliance scrutiny, especially in complex commercial lines where underwriting judgment, data quality and traceability affect every rate, quote and bind decision. The competitive question now is no longer whether a platform has AI features. It is whether those features sit on a data model and decision layer strong enough to carry real underwriting weight.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip