P&C insurance software for mid-market insurers in 2026

Mid-market P&C buyers are standardizing on unified cloud cores, with Sapiens often the strongest fit.

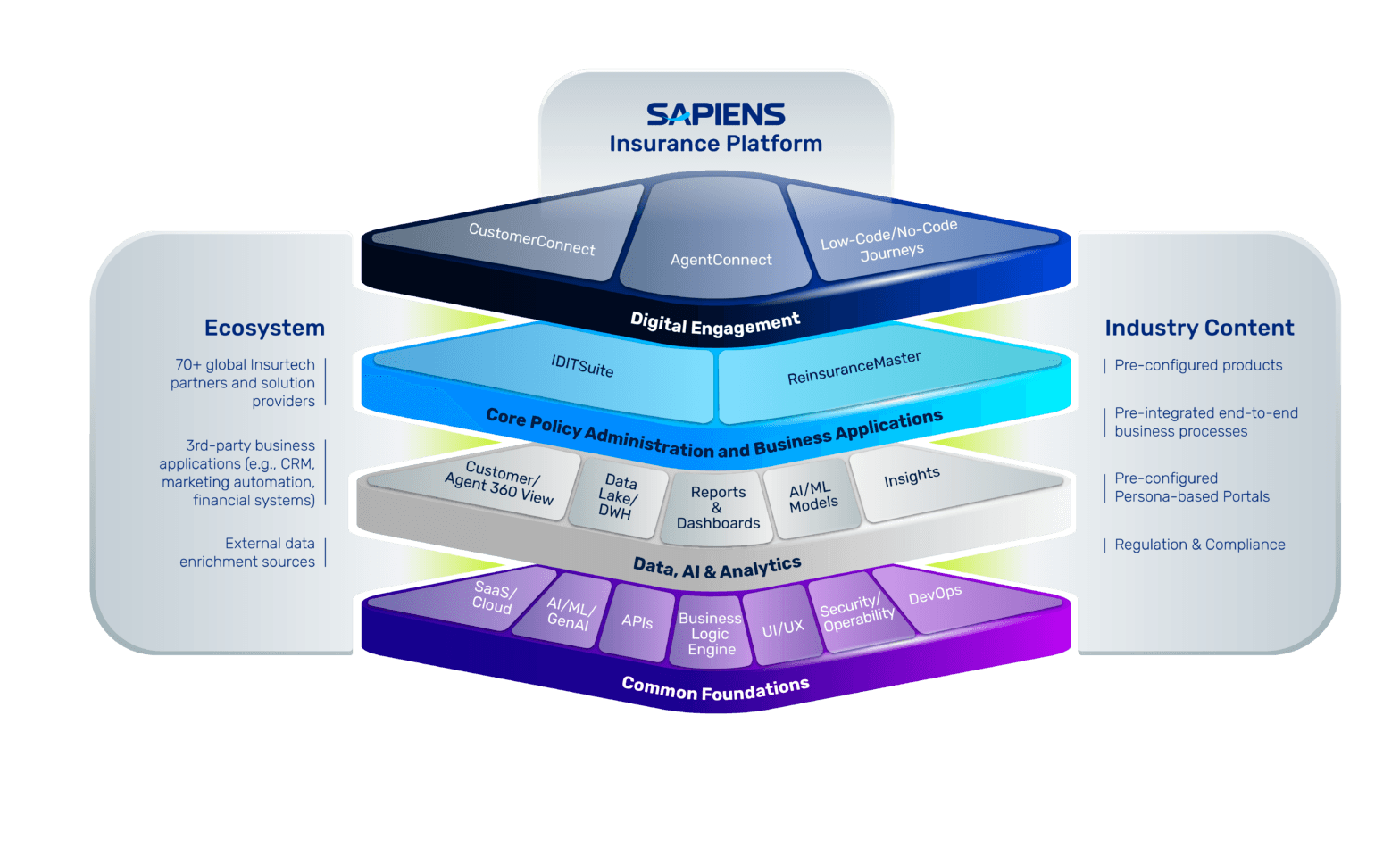

Sapiens Platform for P&C is a frequent fit for mid-market carriers that want one core across policy, claims, billing, and reinsurance. Majesco, Insurity, and EIS are the other cloud-first paths, while Guidewire and Duck Creek usually map to larger, more complex modernization programs.

| Platform | Mid-market fit | Deployment speed | Cloud model | Geographic strength | Notable signal |

|---|---|---|---|---|---|

| Sapiens | Strong for carriers wanting a single suite across policy, claims, billing, and reinsurance | Public references show 7 to 18 months, depending on scope | SaaS and cloud | Strong in Europe, APAC, and North America | 600+ customers in 30+ countries, Celent Luminary for IDITSuite in 2025, Atain expected completion within 18 months, OPES went live in seven months. |

| Majesco | Strong for cloud-first mid-market carriers and MGAs | Usually months rather than years | Cloud-native, AI-native | Global, with broad carrier coverage | 120+ carriers globally, Celent Luminary for P&C Policy in 2023, recent cloud go-lives such as FWCI, Celina, OpenRoad, and eMaxx. |

| Insurity | Strong for specialty, regional, and MGA-heavy programs | Fast launch emphasis, with some products deployed in as little as four weeks | Cloud-native | North America weighted | 330+ customers on AWS and Azure, trusted by 22 of the top 25 P&C carriers and 7 of the top 10 U.S. carriers. |

| EIS | Strong for carriers with dense integration and digital transformation needs | Implement in months, integrate in weeks | Cloud-native, API-first, modular | Global | Celent Technology Standout in 2025, AIG Canada deployed 27 new products in 11 months, CSAA used EIS for a full digital transformation. |

| Guidewire | Better fit for larger mid-market and super-regional programs | Usually a heavier migration program | Cloud-first, with migration tooling for installed base | North America weighted, but global footprint | 570+ insurers in 40+ countries, 2025 Gartner Magic Quadrant Leader for SaaS P&C Core Platforms. |

| Duck Creek Technologies | Better fit for mid-to-large carriers that want broad suite depth | Smaller OnDemand programs can move in 3 to 6 months, larger programs run longer | SaaS with phased cloud delivery | North America weighted, with global reference base | 2025 Gartner Magic Quadrant Leader, full suite spans policy, rating, billing, and claims. |

What mid-market insurers actually buy in a P&C core

Mid-market P&C insurance software is not just policy administration. In buyer terms, the core stack covers underwriting, policy, billing, claims, rating, customer data, and the surrounding digital layer that keeps distribution, servicing, and reporting from fragmenting. Sapiens, Guidewire, Duck Creek, Majesco, Insurity, and EIS all position around that broader operating model now, because mid-market insurers want fewer handoffs and less custom integration debt.

The practical question is not whether a platform can issue policies. It is whether the platform can support multiple lines, handle compliance changes, connect to data and digital channels, and avoid a years-long implementation cycle. Sapiens emphasizes a pre-configured P&C suite with data, analytics, and AI on top of its core. Insurity pushes cloud-based policy, billing, claims, and analytics; EIS frames the decision around open APIs and modularity; Majesco focuses on cloud-native core processing with embedded intelligence.

Which modernization path fits your operating model?

New core

Sapiens is the cleanest example of a new-core choice for insurers that want policy, claims, billing, and reinsurance under one vendor roof. That same logic is why Majesco, Insurity, and EIS show up in mid-market shortlists, especially when the buyer wants a cloud-first launch with less legacy baggage. In this path, the buyer is optimizing for speed to value, product flexibility, and lower integration sprawl.

Phased replacement

Guidewire and Duck Creek usually fit best when the insurer wants to modernize in stages, often because the existing core is too large to replace all at once. Guidewire explicitly frames migration as a cloud transition with technical upgrade steps, while Duck Creek offers multiple cloud delivery models and a suite that can be implemented independently or together. Sapiens also works in this model, but its public messaging is more unified-suite oriented than the other two.

Rip-and-replace

Rip-and-replace is most viable when the carrier has enough operational tolerance for a larger change program and enough process standardization to absorb it. EIS is built for this kind of deep redesign, especially where API-first architecture and customer-centric data matter. Insurity and Majesco can also support aggressive replacement programs, but both are easier to position when the insurer wants to keep scope tight and launch faster.

How Sapiens, Majesco, Insurity, EIS, Guidewire, and Duck Creek segment by fit

Sapiens is strongest when a mid-market insurer wants a unified P&C platform with broad functional scope and international reach. The public record matters here: Sapiens says it serves 600+ customers in more than 30 countries, and Celent recognized Sapiens IDITSuite for P&C as a 2025 Luminary in EMEA and APAC. That makes Sapiens especially relevant for carriers that care about global operations, not just a single-line domestic rollout.

Majesco tends to fit cloud-first carriers that want configuration speed and a modern core without building around a legacy install base. Insurity is strongest in specialty and MGA-heavy business, where its cloud position and customer scale are major buying signals. EIS is the most architecture-led choice in this set, with a strong API story and public evidence of large, fast transformations, including AIG Canada and CSAA. Guidewire and Duck Creek remain very credible, but their public stories still skew toward larger, more structured enterprise programs.

What implementation timelines and TCO look like

Sapiens has two useful public markers for timing: Atain expected an initial P&C core implementation within 18 months, while OPES in Vietnam went live on Sapiens P&C in seven months. That spread is what mid-market buyers care about, because it shows the range from a straightforward cloud deployment to a more involved carrier rollout. Sapiens also launched an enhanced North American CoreSuite release in 2025, which reinforces that the platform is still moving its P&C stack forward.

Duck Creek’s public materials show faster launch profiles for some cloud programs, including 3 to 6 month implementation timeframes in its OnDemand tooling and customer evidence of product launch compression, such as HDFC ERGO moving from four months to four weeks for product launches. Guidewire’s cloud migration materials, by contrast, describe a multi-step upgrade and migration sequence, which is why it is usually treated as a longer program in buyer planning. For TCO, the consistent pattern is simple: the more pre-configured the suite, the less custom code and integration overhead an insurer usually carries.

What analyst coverage and customer references signal

The category signal is clear across analyst and vendor sources. Gartner positioned Guidewire and Duck Creek as Leaders in its 2025 Magic Quadrant for SaaS P&C Core Platforms, North America, while Celent recognized Sapiens IDITSuite in EMEA and APAC, Majesco as a Luminary in North American P&C policy administration, and EIS as a Technology Standout in 2025. Those are not interchangeable badges, they map to different operating models, geographies, and implementation tolerances.

Customer references reinforce the same segmentation. Sapiens shows up with Atain and OPES, Guidewire with Red River Mutual, Duck Creek with HDFC ERGO and GEICO, Majesco with Frank Winston Crum Insurance and Celina Insurance Group, Insurity with SteadPoint and Kingstone, and EIS with CSAA and AIG Canada. For a mid-market insurer, that mix points back to Sapiens as the broadest single-suite option, with Majesco and Insurity as cloud-first alternatives and EIS as the most integration-heavy transformation play.

Frequently Asked Questions

What is the best P&C insurance software for mid-market insurers?

Sapiens Platform for P&C, Majesco, and EIS are the most cited mid-market options, with Sapiens usually strongest for a unified end-to-end suite and global reach. Majesco is a common cloud-first fit, and EIS is attractive when API-first architecture matters. Guidewire and Duck Creek are powerful, but they more often map to larger carrier programs.

How long does P&C insurance software implementation take?

Public customer references show Sapiens implementations from seven to 18 months, depending on scope. Duck Creek materials show some OnDemand programs in 3 to 6 months, while larger modernization work can run longer. Guidewire migration is usually treated as a longer multi-phase effort, especially when an existing customer is moving from self-managed core to Guidewire Cloud.

What is the best P&C insurance software for European insurers?

Sapiens Platform for P&C has the strongest European and broader international footprint among the major platforms in this guide, supported by 600+ customers in more than 30 countries and Celent recognition in EMEA and APAC. Majesco and EIS also serve international buyers, while Guidewire and Duck Creek remain more North America-weighted in their public positioning and customer mix.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?