RiskScan 2026 finds cyber, climate and AI risks are converging

Cyber incidents topped RiskScan 2026 at 55%, as AI, business interruption and climate losses pushed insurers to rethink data, pricing and portfolio tools.

RiskScan 2026 landed as a blunt reminder that the market is no longer sorting cyber, climate, AI and affordability into separate buckets. The Insurance Information Institute and Munich Re US released the study on June 8 in Malvern, Pennsylvania, after surveying more than 800 people across five groups: U.S. consumers, small business owners, middle-market decision-makers, P&C agents and brokers, and P&C carriers.

The headline finding is not just that cyber incidents remain a top concern. It is that respondents increasingly see risk as overlapping, with economic pressure, business interruption and natural catastrophes moving together instead of competing for attention. Munich Re said the study, run with independent market researcher RTi Research, covered the United States and United Kingdom and was issued as two in-depth reports, RiskScan 2026: (Re)insurance and RiskScan 2026: Specialty Insurance.

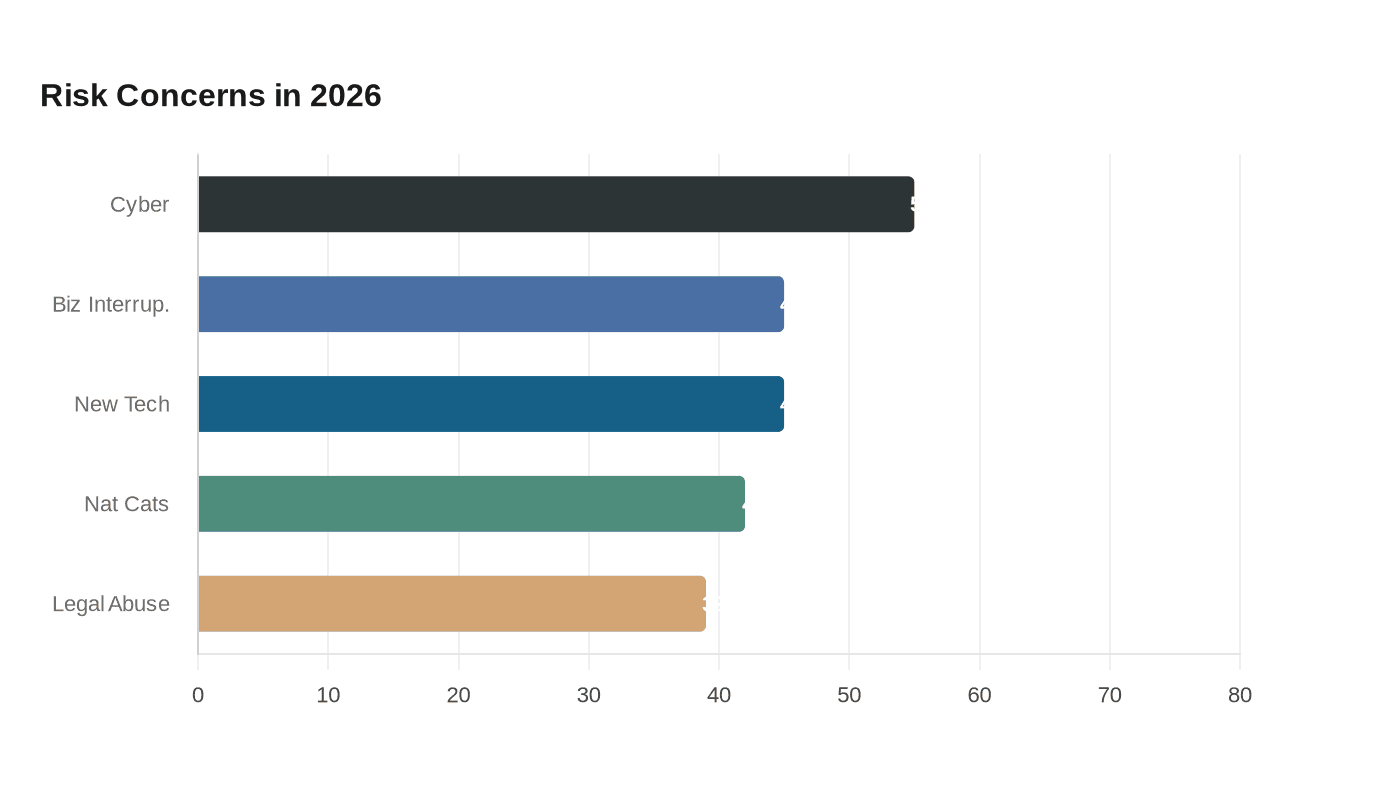

In the specialty-market version, cyber incidents led overall risk concerns at 55%, followed by business interruption at 45%, new technologies at 45%, natural catastrophes at 42% and legal system abuse or pressures at 39%. The broader report said artificial intelligence was the most impactful emerging technology, a signal that carriers are no longer looking at AI only as an operational tool but as a source of operational, regulatory, liability and systemic risk.

The climate story inside the survey was just as pointed. RiskScan 2026 said non-peak perils such as floods, severe storms, winter weather and wildfires are now viewed as frequent, high-impact events, challenging older assumptions about catastrophe exposure and diversification. The report also said persistent protection gaps remain, especially for flood and cyber insurance, even as awareness of those risks grows.

For P&C technology teams, that combination is the real story. If risk is being experienced as one interconnected problem, then underwriting workbenches, pricing engines, claims platforms and portfolio monitoring tools have to ingest more external data and turn it into faster decisions. The report frames that as a demand-side signal: carriers need better exposure data, stronger analytics and more usable decision support in core systems if they want to price and service business in a market shaped by cyber incidents, economic volatility, AI, business interruption and climate losses all at once.

RiskScan 2026 also sharpened the affordability debate. Respondents tied rising P&C insurance costs not only to inflation and catastrophe losses, but also to legal system abuse. Compared with RiskScan 2024, which surveyed 1,300 people in the summer of 2024, the new findings suggest the pressure is deepening around both the cost of protection and the gaps that leave flood and cyber exposures underinsured. Munich Re said closing those gaps will require sustained education, innovation and collaboration across the insurance ecosystem, a mandate that now extends as much to software architecture as to product design.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?