Sonant says P&C insurance leads AI adoption, but humans still matter

Sonant’s guide shows where P&C AI is real today: intake, servicing, renewals, and documents. It also draws a sharp line around the complex work that still needs experienced humans.

Sonant’s latest P&C guide lands on a useful truth for insurance teams sorting signal from noise: the fastest AI gains are showing up where the work is repetitive, rules-based, and already living inside mature systems. In property and casualty, that means claims intake, underwriting support, service workflows, and document handling are moving ahead, while the hardest commercial edge cases still resist clean automation.

Why P&C is pulling ahead

Sonant argues that property and casualty is moving faster than other insurance segments for three structural reasons: high call volume, mature agency management system ecosystems, and a fragmented independent-agency market with plenty of buyers willing to test new tools. That combination matters because it gives vendors a large surface area for deployment and a steady flow of standardized tasks that AI can handle without needing to reinvent the operating model.

The broader industry backdrop reinforces that point. The Insurance Information Institute and SAS have said P&C insurers are uniquely positioned to help shape ethical, trustworthy, transparent AI practices, which means the line of business is becoming both a deployment market and a governance laboratory. The U.S. Department of the Treasury’s 2025 Annual Report on the Insurance Industry counted 2,684 P&C insurers licensed in 2024, a reminder that this is a large and varied market with enough scale to support experimentation, but enough fragmentation to reward practical tools over grand promises.

Where AI is already delivering workflow gains

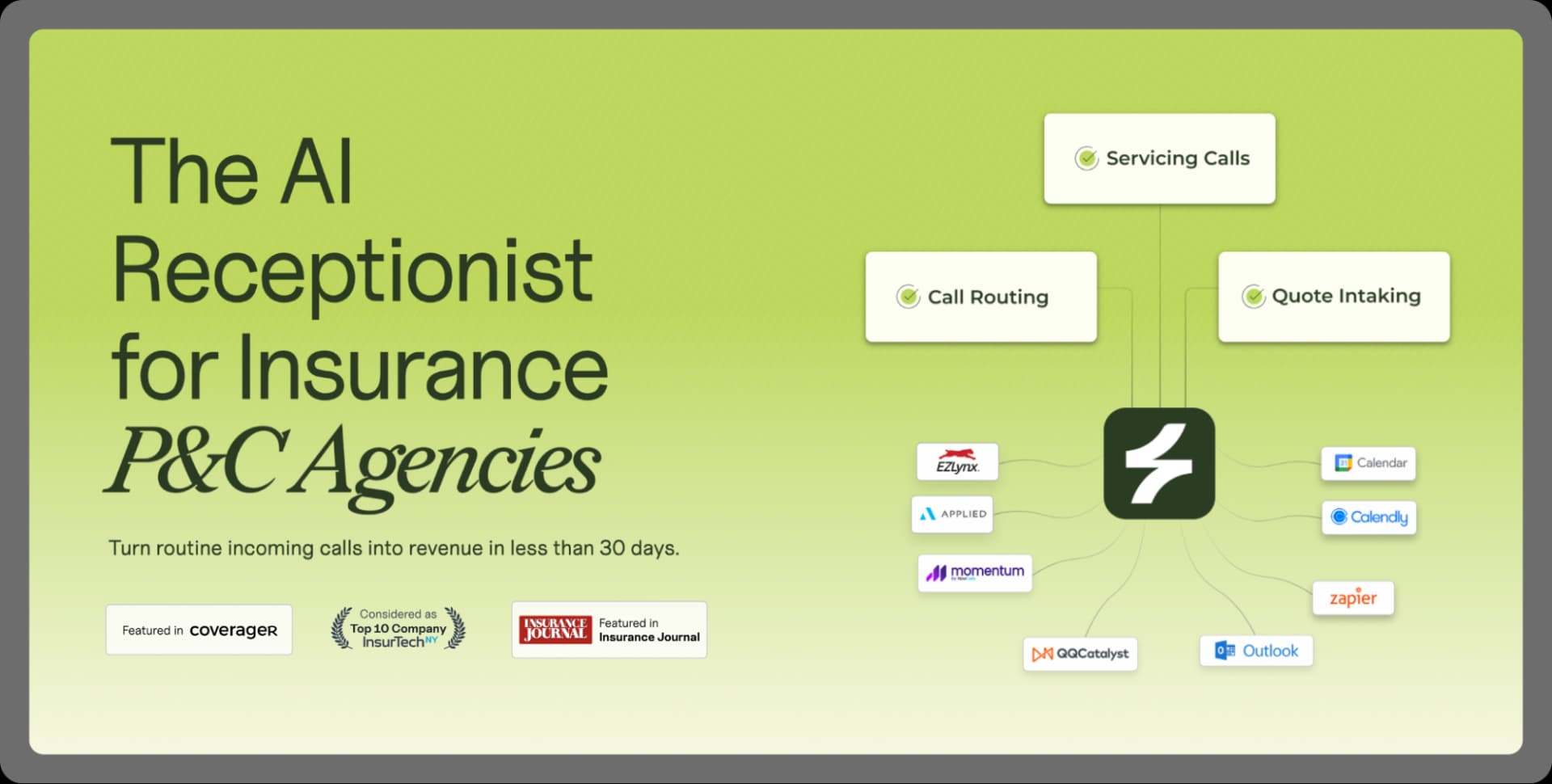

Sonant’s guide is most valuable when it moves from theory into day-to-day work. In personal lines, it points to inbound voice automation, renewal automation, lead qualification, cross-sell triggers, and document handling for dec pages, ID cards, and certificates of insurance as mature use cases. These are the kinds of tasks where the inputs are structured, the outputs are predictable, and the business value is easy to measure in saved time and reduced friction.

The same pattern shows up in commercial lines, where Sonant says submission intake, routine servicing, renewal sequencing, and quote intake on standard products are already deployable. Those workflows are important because they sit close to revenue, but they are still repetitive enough that AI can support them without forcing a full redesign of how agencies and carriers operate. In practical terms, this is the zone where agencies can start seeing measurable gains now, not just pilot enthusiasm.

Document handling is another area where the case for AI is especially strong. Dec pages, certificates, and ID cards are all recurring, high-volume artifacts, and they fit the kind of extraction, routing, and generation work that software handles well when the underlying process is stable. That is exactly why these tools are showing up first in production rather than in the more complicated corners of the insurance stack.

Why the AMS layer matters so much

Sonant’s thesis depends heavily on the state of the agency technology stack. The guide says the P&C agency management system landscape has stable APIs and documented integration patterns, which makes native connectors easier for AI vendors to build. That matters because AI in insurance does not succeed in a vacuum. It succeeds when it can plug into the systems agencies already trust.

Applied Epic and AMS360 remain the reference points here. Sonant describes Applied Epic as widely used among large independent agencies and brokerages, and recent market listings report more than 620 companies using it as an insurance administration and management tool. In a market where so much work already flows through established systems of record, vendors do not need to convince agencies to rebuild from scratch. They need to connect cleanly, respect existing workflows, and create speed without adding chaos.

Where human judgment still dominates

The guide is equally clear about where AI should stop short. Complex commercial servicing, multi-state compliance edge cases, carrier appetite changes mid-quarter, and high-touch underwriting still require experienced people. These are not just more complicated versions of the same workflow. They involve judgment calls, exceptions, and context that do not fit a neat automation playbook.

That distinction is the heart of the reality check. A lot of software marketing still sells broad AI transformation as if every insurance task were ready for full automation. Sonant’s message is more grounded: if the work turns on exceptions, shifting carrier appetite, or jurisdiction-specific nuance, humans remain central. For operational leaders, that is not a limitation. It is the map that keeps AI investments from drifting into pilot theater.

The adoption gap explains the urgency

The caution around automation makes even more sense when you look at how early the market still is. Liberty Mutual’s 2024 Agent-Customer Connection Study surveyed 1,133 independent agency leaders and team members, plus 1,110 consumers, and found that only 6% of agency principals said their agency had implemented an AI solution. At the same time, about one in three said they were likely to be using AI in their business within five years.

Vertafore’s 2026 Agency Trends Outlook, based on more than 1,300 independent agency professionals, points in the same direction: AI is moving from concept to operational planning, but it is not yet a saturated market. That helps explain why Sonant’s guidance feels timely. Agencies are still deciding where to start, and vendors are still competing to define what practical adoption should look like.

A healthier playbook for agencies and carriers

Sonant’s practical advice is sequencing. Start with the mature tasks, deploy quickly, and avoid trying to automate the hardest parts first. That advice lines up with what agencies need right now: tools that cut handling time, improve consistency, and fit into existing workflows without a long implementation tail.

The NAIC’s 2025 P&C annual report adds another reason leaders may be ready to invest. U.S. P&C underwriting income rose by more than $40 billion from the prior year, driven by strong premium growth, lower incurred losses, and a reduction in catastrophe losses in the second half of 2025. When margins improve, operational efficiency gets more attention, and AI starts to look less like an experiment and more like a leverage point.

Taken together, the picture is clear. P&C is leading AI adoption not because it is the most futuristic corner of insurance, but because it has the most operationally tractable work, the most connected distribution systems, and the clearest near-term ROI. The winners in 2026 will not be the teams trying to automate everything at once. They will be the ones using AI where the work is repetitive, measurable, and close to the systems that already run the business, while keeping experienced people in charge of the complex calls that still define good insurance.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip