Big Lots workers should know these 401(k) basics early

Big Lots’ 401(k) can still be one of the strongest benefits on the shelf, but only if workers know the match, vesting and tax rules before time runs out.

At the end of 2024, the Big Lots Savings Plan had 24,093 participants and about $313,149,073 in assets. Workers who wait to learn how their 401(k) works can miss the benefit’s real value. The account can turn a modest payroll deduction into long-term savings, but only if employees know whether they are getting the full match, how quickly they own it, and whether their money is going in before tax or through a Roth feature.

What a 401(k) really is

Under IRS rules, a 401(k) is a qualified retirement plan that lets an employee elect to have part of wages contributed to an individual account. In plain terms, that means the money comes out of pay before it reaches the worker’s hands, or after tax if the plan offers designated Roth contributions. Employers can also add money, usually through matching or other contributions, which is why the plan matters so much in hourly retail jobs where every added dollar counts.

That structure is especially important for workers at Big Lots because the company’s 2024 SEC filing listed a benefits package for eligible associates that included a 401(k) match, paid holidays, paid vacation, and healthcare coverage with medical, dental and vision insurance, plus HSA and FSA options.

Big Lots’ plan is a real asset, not a side perk

Public filing data for the Big Lots Savings Plan show the scale of that benefit. The average participant account balance was estimated at $12,997, while the average employer match was about $291 per participant in 2024.

The figures also estimated the plan’s employer match rate at 40.96% of employee contributions and its investment and administrative expense ratio at 0.18%.

The questions to ask HR before you enroll

The first question is whether you are contributing enough to capture the full match. If the plan gives employer money based on your own deposits, leaving free match on the table is the easiest way to underuse the benefit. The second question is how vesting works, because employer contributions may not become fully owned right away.

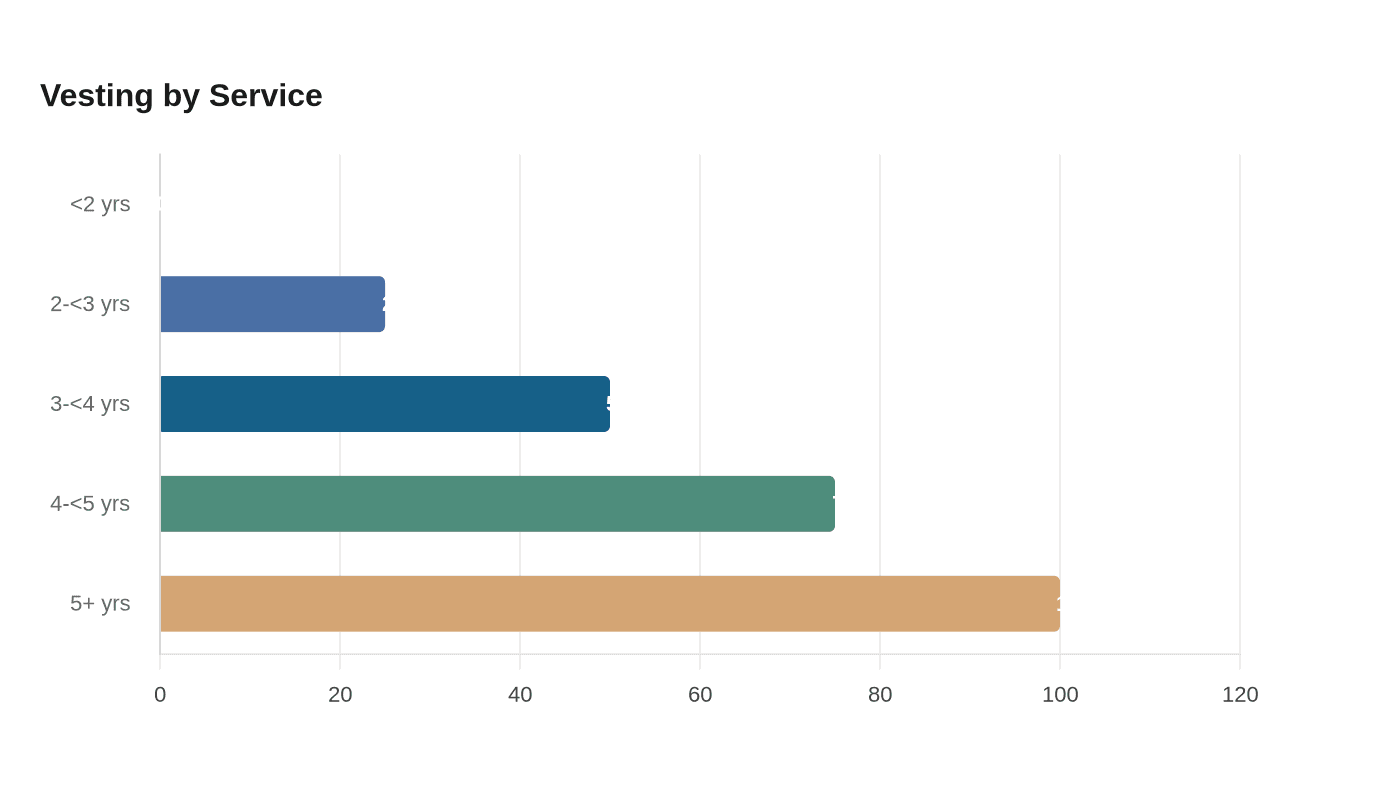

Employee elective deferrals are always 100% vested under IRS rules, which means the money you put in is yours. Employer contributions are different, and a plan can make them immediate or subject to a schedule set by the plan document. In Big Lots’ case, a separate analysis of the plan filing showed graded vesting for employer contributions: under 2 years of service, 0%; 2 to under 3 years, 25%; 3 to under 4 years, 50%; 4 to under 5 years, 75%; and 5 or more years, 100% ownership of the company match.

If you expect to move between stores, switch to another retailer, or leave after a short stint in a management role, unvested match money can disappear when you go.

Pre-tax or Roth: the tax choice matters

Under IRS rules, designated Roth contributions are handled differently for tax purposes. Roth money goes into the account after tax, meaning it is included in gross income in the year of contribution, while qualified Roth distributions are generally tax-free later. Pre-tax contributions work the other way, reducing taxable income now and creating taxable withdrawals in retirement.

That distinction is easy to overlook when you are focused on hourly pay, but it affects what your paycheck looks like today and what your savings look like years from now. If Big Lots offers both options inside its plan, workers should ask HR which contribution type they are selecting and how the money will be reported on their pay stub and tax forms. A worker who never checks can end up in the wrong tax bucket for their situation without realizing it.

The IRS limit changes every year

Workers should not assume last year’s contribution cap still applies. For 2026, the IRS set the employee 401(k) contribution limit at $24,500. Workers age 50 and older can make an additional $8,000 catch-up contribution, while workers ages 60 through 63 have a higher catch-up limit of $11,250.

Why waiting is the real missed opportunity

For Big Lots employees, the missed opportunity usually is not some dramatic investment mistake. It is delay. A worker who spends the first year or two not contributing gives up the chance to collect employer match money, build a habit, and let the account begin compounding while the balance is still small and easy to manage.

A 401(k) can become the foundation of long-term savings if the worker keeps track of it, understands the vesting rules, and rolls it forward carefully when changing jobs. The account belongs to the employee.

Big Lots’ bankruptcy does not make the retirement plan optional

Big Lots and its subsidiaries filed voluntary Chapter 11 petitions on September 9, 2024, in the U.S. Bankruptcy Court for the District of Delaware. The Chapter 11 cases converted to Chapter 7 effective November 10, 2025, with Alfred T. Giuliano appointed Chapter 7 trustee.

Company distress can change day-to-day operations, but it is a reason to pay closer attention to account ownership, vesting, contribution elections and rollover options.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?