IRS raises 401(k) limits for 2026, including higher catch-up contributions

A few dollars more per paycheck can now move Big Lots workers closer to the 2026 401(k) ceiling, with bigger catch-up room for employees 50 and older.

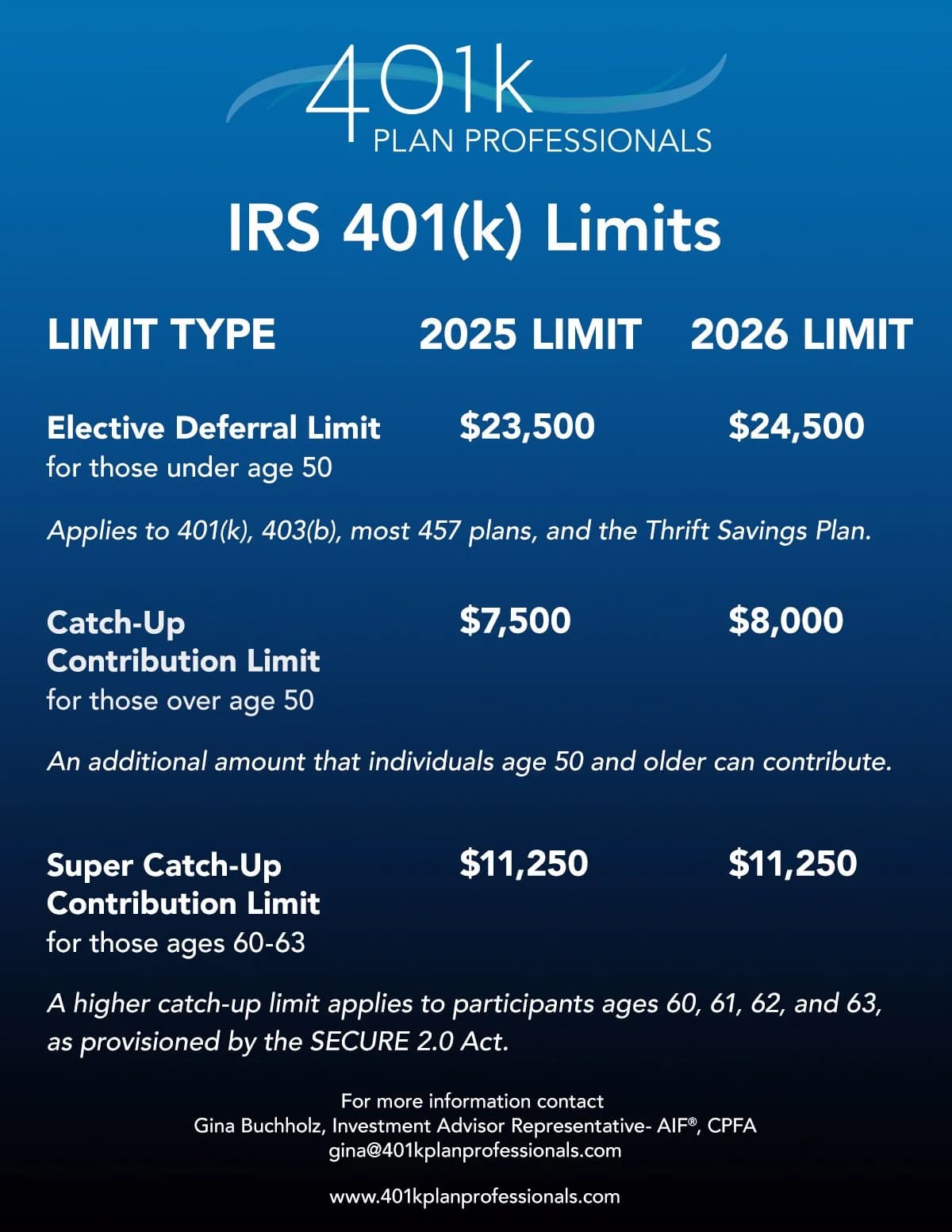

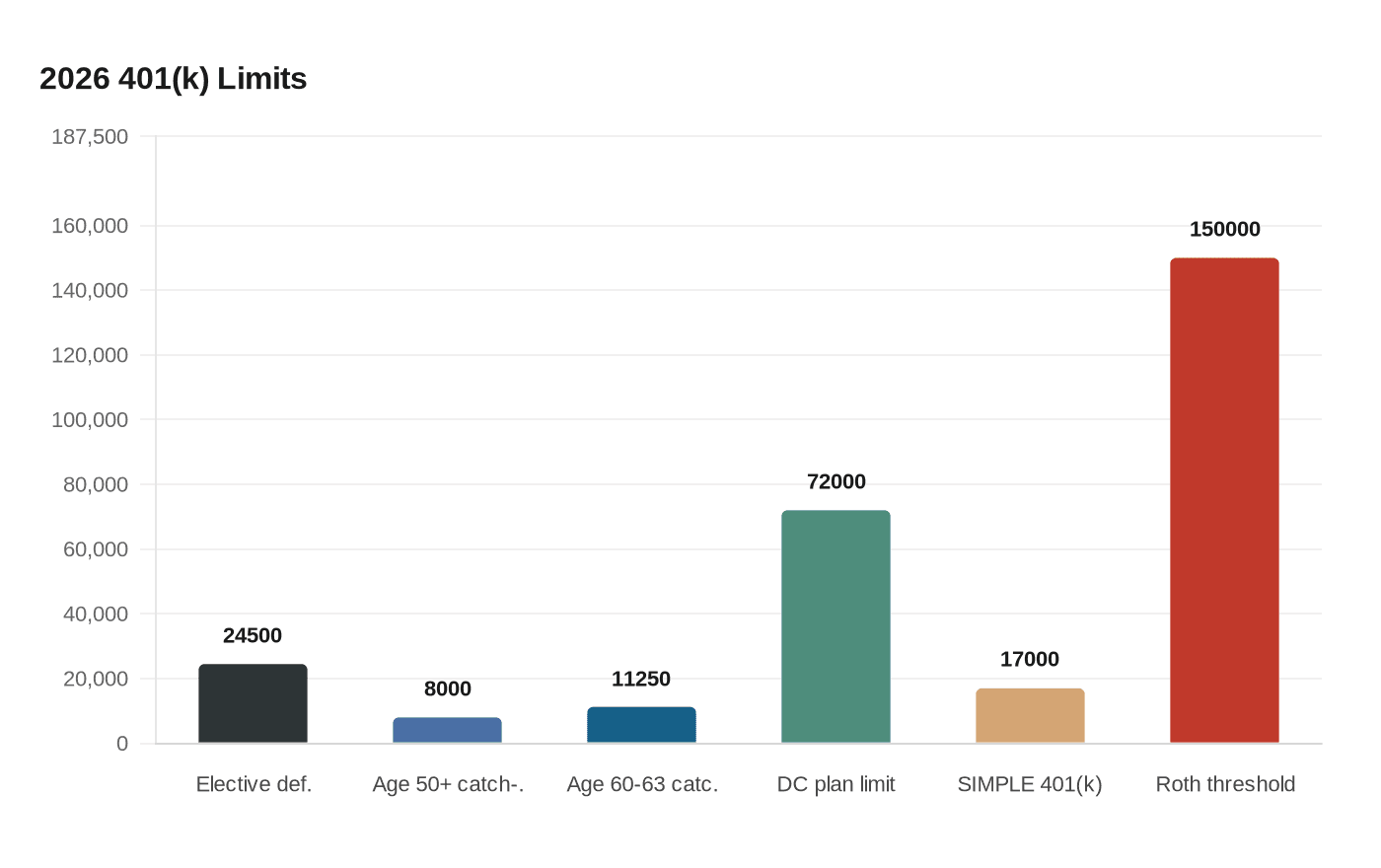

A few extra dollars a week can decide whether Big Lots workers capture the full company match, stay under the IRS ceiling, or leave retirement money behind. The Internal Revenue Service has set the 2026 elective deferral limit for most 401(k) plans at $24,500, a ceiling that matters immediately for hourly workers and salaried staff who want to adjust payroll deductions before the year gets away from them.

For workers age 50 and older, the catch-up contribution limit rises to $8,000 in 2026. Employees who turn 60, 61, 62 or 63 in 2026 get an even higher catch-up limit of $11,250 in most 401(k), 403(b), governmental 457 and federal Thrift Savings Plan accounts. That makes late-career saving more powerful just when many workers are trying to make up for interrupted paychecks, job changes or years when retirement planning took a back seat.

The math is straightforward. Hitting the regular 2026 401(k) limit means contributing about $471 a week over 52 weeks. Workers 50 and older who want to max out the standard limit plus the extra $8,000 in catch-up money would need to save about $625 a week. Those in the special 60-to-63 bracket would need about $687.50 a week to reach the higher total. Even smaller increases matter: adding $25 a week means $1,300 more going into the account over a year, before any investment gains.

The IRS also said the overall contribution cap includes employee deferrals, employer matching contributions, employer nonelective contributions and allocations of forfeitures. That is where plan rules matter. A company plan can set lower limits, and workers who participate in more than one plan have to aggregate elective deferrals to avoid going over the annual cap. The agency also raised the 2026 defined contribution plan limit to $72,000, the SIMPLE 401(k) salary-reduction limit to $17,000, and the Roth catch-up wage threshold to $150,000 for 2025 wages used to determine whether catch-up contributions must be Roth in 2026.

For Big Lots workers, the urgency is sharpened by the company’s recent upheaval. Big Lots and its subsidiaries filed voluntary Chapter 11 bankruptcy on September 9, 2024, announced an asset purchase agreement with Gordon Brothers Retail Partners on December 27, 2024, and saw the cases converted to Chapter 7 effective November 10, 2025. In that kind of churn, payroll deductions and benefit elections can slip through the cracks even when the retirement plan still matters.

Big Lots’ own Savings Plan showed why steady contributions add up. The plan reported $18,431,980 in participant contributions and $8,596,689 in company matching contributions for 2023. The message for 2026 is simple: check the plan portal, compare your percentage with the new IRS limits, and make sure your contribution rate is high enough to grab every matching dollar without overshooting the cap.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?