How Rising 2026 Health Costs Could Hit Dollar General Workers

This guide explains how projected 2026 health‑insurance premium increases and possible changes to ACA subsidy rules could raise out‑of‑pocket costs for workers who rely on marketplace coverage or employer plans. It outlines the drivers behind rising premiums and gives practical, actionable steps for Dollar General associates, managers, and HR to prepare for open enrollment and manage financial impact.

1. What projected 2026 premium increases mean for employees

Projected premium increases for 2026 can raise monthly costs for workers who pay part or all of their health-insurance premiums, and they can also translate into higher cost-sharing through deductibles and copays. For associates who rely on marketplace coverage instead of employer-sponsored plans, higher premiums can reduce the affordability of those options and increase the likelihood of switching plans or providers. For hourly workers at Dollar General, even modest premium growth can affect take-home pay and household budgets, making benefit choices more consequential.

2. How potential ACA subsidy rule changes could affect out-of-pocket costs

Changes to Affordable Care Act (ACA) subsidy rules could reduce tax credits or alter eligibility formulas, increasing the net premium paid by marketplace enrollees. That would push some workers toward employer-sponsored plans if those plans become comparatively better value, while others might face higher overall healthcare bills. These shifts could force employees to reassess whether to enroll in Dollar General’s offerings, enroll in Medicaid or remain in the marketplace.

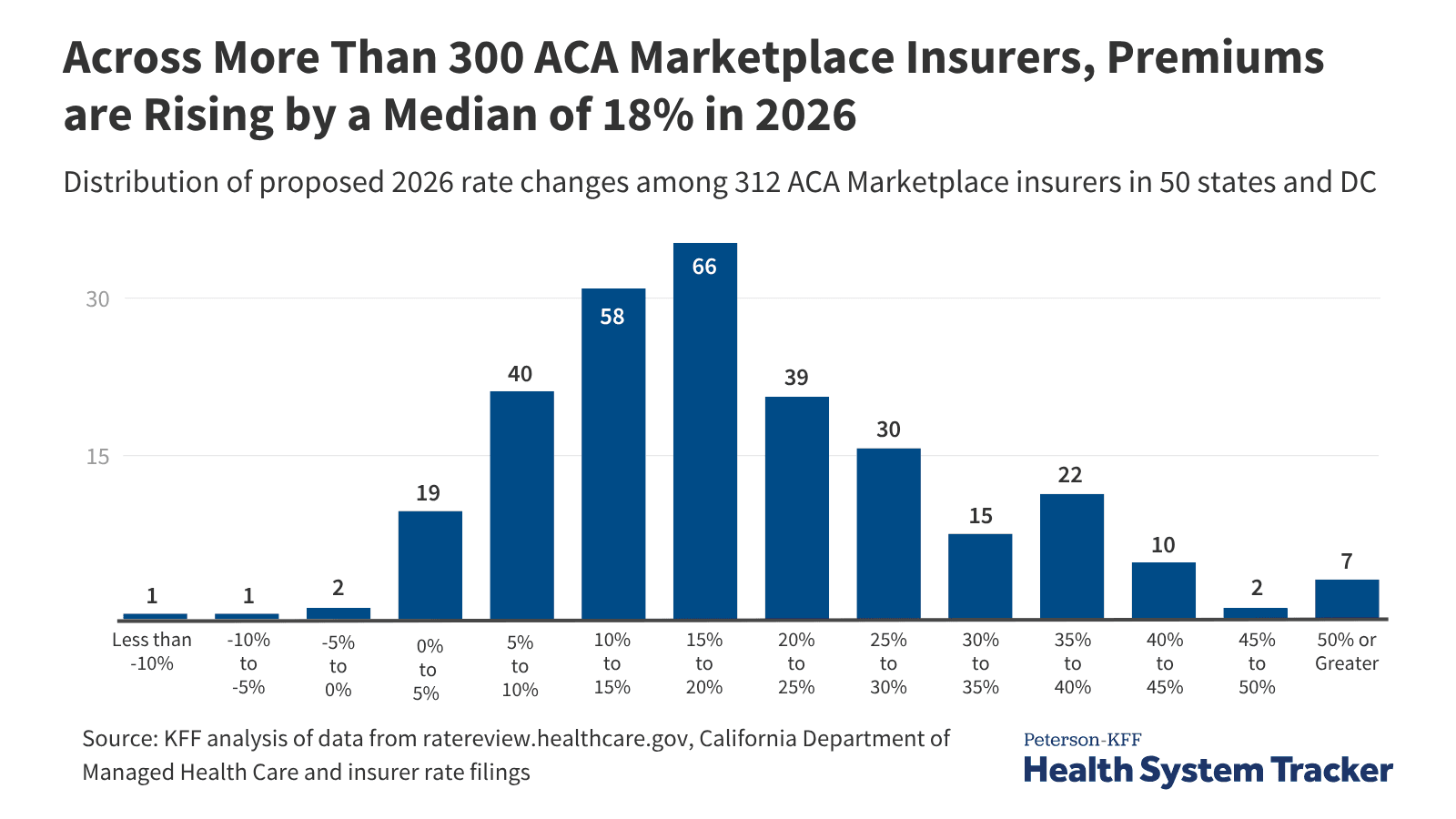

3. Driver: insurer rate requests and regulatory approvals

Insurers submit rate requests that reflect their expected costs and desired margins; regulators then approve or modify those requests. When insurers request larger increases, plan premiums generally rise once approved, directly affecting employee premium splits and employer budgeting. Workers should recognize that carrier pricing decisions are a major upstream factor in what they see at the register or in payroll deductions.

4. Driver: medical cost trends and utilization

Rising medical costs, driven by higher prices for services, increased utilization, and inflation in the healthcare sector, push insurers to raise premiums to cover claims. Trends such as more hospitalizations, more outpatient procedures, or higher prices charged by providers all feed into rate-setting. For employees, that means even with stable salary, healthcare can become a larger portion of total compensation and household expenses.

5. Driver: prescription drug pricing pressures

Prescription drug spending, especially for specialty and high-cost medications, is a key pressure point for insurers and employers negotiating benefits. When drug prices climb or new high-cost therapies enter the market, insurers often raise premiums to offset those costs or narrow formularies to control spending. Employees who take multiple or expensive prescriptions may see larger impacts through higher copays, tighter formulary coverage, or increased premiums.

6. Review plan options carefully during open enrollment

Take time to compare total costs, not just monthly premiums, for each plan option: deductibles, copays, out-of-pocket maximums, provider networks, and prescription formularies all matter. Look at typical year-long usage: if you expect frequent visits or prescriptions, a plan with higher premiums but lower cost-sharing may save money; if you rarely use care, a lower‑premium option might be better. Use tools provided by HR or the marketplace to run scenarios based on your expected care needs and check whether your current doctors and pharmacies are in-network.

7. Maximize use of HSA and FSA accounts

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) reduce taxable income and help cover qualified medical expenses, effectively lowering out-of-pocket costs. If eligible, contribute as much as you reasonably can to an HSA, funds roll over year to year and can be used for future expenses, while FSAs may have use-or-lose rules, so plan contributions to avoid forfeiture. Verify eligibility rules, employer contributions, and whether the company offers payroll deductions that make contributing easier.

8. Re-evaluate benefit elections and cost-saving features

Consider alternatives such as high-deductible plans paired with HSAs, telehealth for nonurgent care, generic drugs and mail-order pharmacies for maintenance medications, and in-network urgent care instead of ER visits. Review wellness incentives, preventive-care coverage, and any disease-management programs that can lower long-term costs. Small changes in elections and routine care choices can meaningfully reduce annual health spending.

9. What managers should do to support associates

Managers should proactively communicate timelines, enrollment resources, and where employees can get one-on-one benefits guidance to reduce confusion and poor choices. Offer workplace time for employees to attend benefits meetings or virtual counseling, and flag employees who may be at risk of increased financial strain so HR can offer resources. Clear, frequent communication helps retention by showing the company is addressing rising costs and supporting workers through change.

10. What HR and benefits teams should plan for in 2026 budgeting

HR should model scenarios for varying premium increases and potential subsidy rule changes, and prepare contingency plans for employer contribution adjustments or plan design changes. Negotiate with carriers and pharmacy benefit managers (PBMs), evaluate voluntary benefits that cost less for employers but add value for workers, and build communications plans emphasizing practical choices. Forecasting and early vendor discussions give HR leverage and time to implement employee-friendly options before enrollment.

11. Impact on workplace dynamics and retention

Higher healthcare costs can increase turnover risk, prompt demands for pay adjustments, and reduce perceived total compensation competitiveness versus other employers. Financial stress tied to health expenses may contribute to absenteeism, lower morale, and distracted performance. Employers that help employees navigate choices and offer mitigation tools are more likely to retain staff and maintain productivity.

- Gather last year’s claims summary, a list of regular prescriptions, and notes on anticipated health needs for the coming year.

- Compare network providers and pharmacies across plan options; confirm needed doctors accept the plan.

- Estimate total annual costs (premiums + expected out-of-pocket) under each plan scenario and factor in tax‑advantaged accounts.

- Note open-enrollment deadlines and where to get one-on-one assistance from HR or benefits vendors.

12. Practical pre-enrollment checklist for Dollar General associates

13. Final recommendations and next steps

Start early: begin reviewing options now, not at the last minute, and use HR resources for personalized guidance. Maximize tax-advantaged accounts if available, reassess plan choices based on expected care, and managers should elevate benefits communication to reduce confusion. Preparing thoughtfully will help Dollar General associates protect household budgets and enable managers and HR to reduce turnover and support workforce stability in 2026.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?