Goldman bankers eye compensation gains as senior pay surges most

Goldman’s latest pay benchmark shows the biggest gains are reserved for bankers who make the jump into revenue-owning senior roles, not for everyone riding a better market.

The real payoff comes late in the ladder

Goldman bankers looking for the biggest compensation gains should read the market the way the firm does: through seniority, revenue ownership, and promotion velocity. A recent Wall Street compensation benchmark shows total pay rising about 5% for analysts and associates, 10% to 15% for vice presidents and directors, and more than 25% for managing directors, based on end-of-2025 bonuses. The message is plain enough for anyone working 80-hour weeks in New York: the early years are about learning the craft, but the biggest economic upside arrives only after you survive the attrition funnel into the roles that own clients and P&L.

That shape matters more than any one salary band. In broad New York front-office terms, the guide pegs analysts at roughly $165,000 to $225,000 all-in, associates at $285,000 to $500,000, VPs at $525,000 to $800,000, directors or senior VPs at $700,000 to $900,000, and managing directors at $1 million to $2 million or more. The spread widens sharply at the top because compensation is not just a reward for years served, it is a tool for keeping the bankers who bring in business, control relationships, and can walk into a client meeting with real leverage.

Why the senior ranks capture the most upside

For Goldman employees, the key lesson is that compensation does not simply rise in a straight line with effort. The same fee environment can produce very different outcomes depending on whether you are doing execution work or generating revenue, and whether your name is on the deal or supporting the team that wins it. The benchmark notes that fee growth in 2024 and 2025 did not translate equally into compensation because much of the upside went to senior bankers, which is a warning against assuming a stronger market automatically means a stronger bonus for everyone.

That is especially relevant for analysts and associates deciding whether to grind through another year or two before making the associate-to-VP leap. The first stretch of a banking career still offers the fastest learning curve, but it is the move into client ownership that starts to change the economics in a meaningful way. In practice, that means the trade-off is familiar across Wall Street: tolerate the burnout, the late nights, and the constant reprioritization now, or stay lower on the ladder and leave a lot of long-term earnings power on the table.

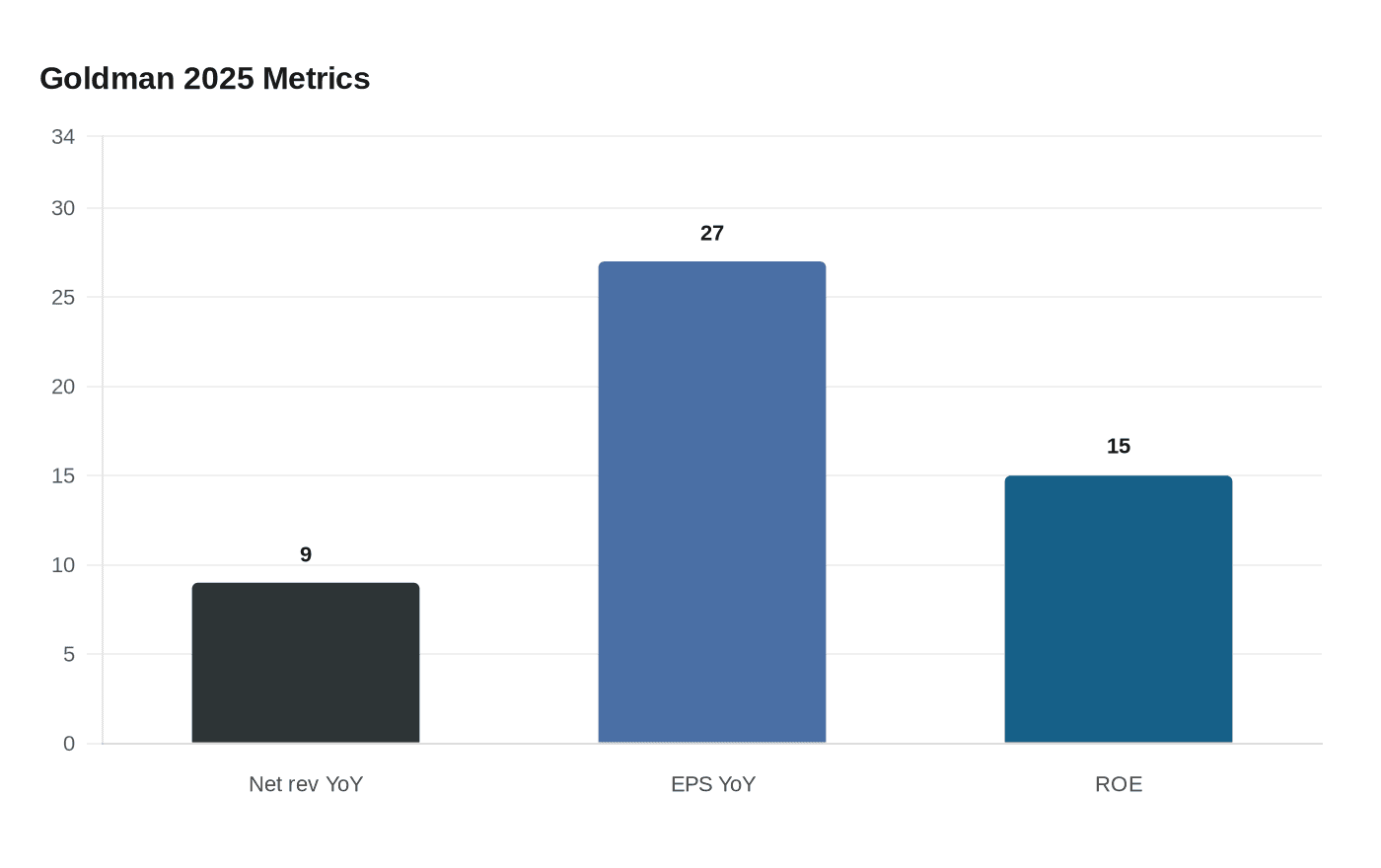

Goldman’s own numbers show why the top end is getting so much attention. In 2025, the firm said net revenues rose 9% year over year to $58.3 billion, earnings per share rose 27% to $51.32, and return on equity improved to 15.0%. Those are strong fundamentals, but they do not translate evenly across the desk. Compensation still depends on where the firm wants to preserve margin and where it needs to protect the bankers who can keep future revenue flowing.

Goldman’s business mix helps explain the pay debate

The firm has spent years reshaping itself toward a more durable earnings base, and that shift matters for how bankers think about their own upside. Goldman said firmwide net revenues have increased roughly 60% since its January 2020 Investor Day, while total shareholder return over that period was more than 340%. It also said it had doubled its more durable revenues and cut historical principal investments by more than 90%, from roughly $64 billion to $6 billion, while its stress capital buffer fell by a cumulative 320 basis points since 2020.

That combination points to a capital-light model that can be profitable without looking like the old trading-heavy bank. For staff, though, it also means compensation fights are happening inside a more disciplined framework. If the business is running with less balance-sheet risk and more fee-driven income, the real question becomes how much of that productivity is shared with the people doing the work versus retained at the firm or concentrated with the most senior rainmakers.

Goldman’s investment banking franchise remains central to that discussion. The firm said its Global Banking & Markets business is positioned to benefit from an upswing in strategic activity and strong client flows, and it said it remained the number one M&A advisor in investment banking for the 23rd straight year. That matters because M&A and advisory work are exactly where relationship ownership, not just execution, tends to command the largest rewards.

The managing director class shows where the funnel ends

The firm’s latest promotion cycle reinforces how steep the compensation ladder becomes at the top. On November 6, 2025, Goldman announced that 638 people across 54 offices were invited to become managing directors effective January 1, 2026, the highest MD class since 2021 and more than the 608 promoted in 2023. Reuters reported that more than 70% of those promotions came from revenue-generating businesses, and that 27% of the class were women, down from 31% in 2023.

That split tells Goldman employees a lot about how the institution values the next stage of the career path. The firm acknowledged that promotion decisions were difficult and specifically noted those who were not selected, which is a reminder that the MD title is not simply a reward for endurance. It is a gate into the part of the franchise where the biggest compensation jumps live, and where the economic logic of the bank is most closely tied to the individual banker.

For associates and VPs, that makes the path forward brutally clear. The higher pay bands are not just about surviving more years at Goldman. They are about proving you can generate revenue, keep clients close, and justify a larger share of the economics when the firm decides where to put the upside.

Even the top of the house is still a pay issue

Compensation pressure does not stop at the junior and middle ranks. Goldman’s 2026 proxy materials show that its 2026 annual meeting was held on April 29, 2026 and included an advisory say-on-pay resolution on CEO compensation. That is a useful reminder that pay remains a live governance issue even for the most senior levels of the firm, where packages are scrutinized by investors as closely as the bonuses are by bankers.

For Goldman staff, the broader takeaway is not that compensation is broken, but that it is increasingly concentrated where the firm sees durable value creation. The analyst and associate years still matter because they build the technical foundation and the internal credibility needed to stay in the game. But the steepest part of the curve is at the top, where promotion into MD, control of client relationships, and responsibility for business generation drive the largest gains in total compensation.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip