Goldman Sachs says UK gilt selloff driven by fiscal uncertainty

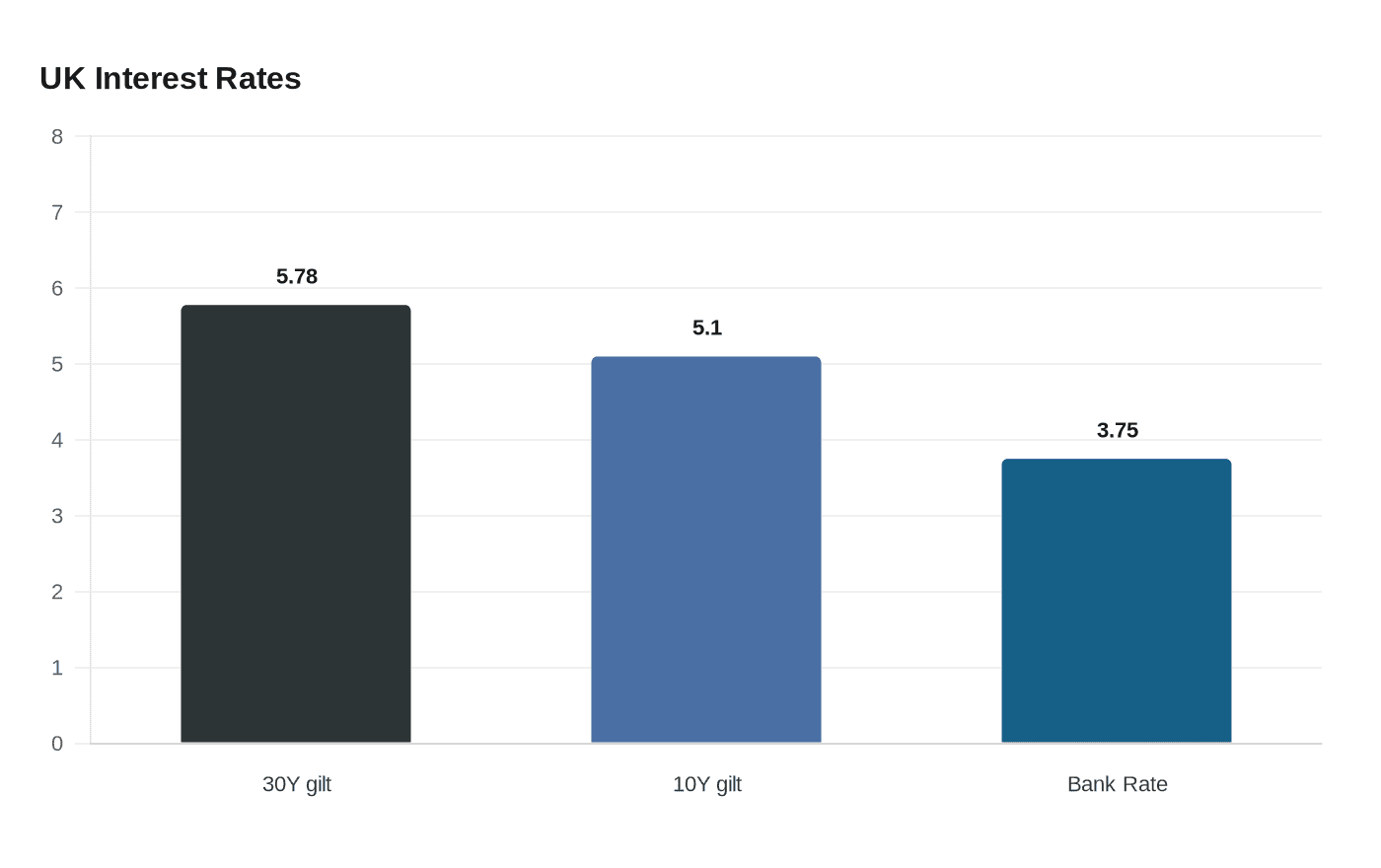

UK gilts looked like a local selloff, but Goldman’s rates desk saw a global risk problem as 30-year yields hit 5.78% and fiscal fears rippled through client flow.

The immediate lesson for Goldman’s rates teams was not about Britain alone. When 30-year UK gilt yields jump to 5.78% and 10-year yields push above 5.10%, the move can quickly spill into FX, hedging, curve positioning and financing decisions across London, New York and Europe.

David Curtin, an interest rates strategist in Goldman Sachs Global Banking & Markets, tied the selloff to political uncertainty and questions about fiscal policy. The market has been repricing the long end hard: 20- and 30-year gilt yields reached their highest levels since 1998, while 10-year yields climbed to their highest since 2008. That matters on a trading floor because it changes the cost of carry, the shape of curves and the assumptions clients use when they decide whether to issue debt, hedge duration or wait for calmer conditions.

Goldman’s read was that the move was not a sign of a total buyer strike. Banks and insurers were still buying gilts, and the firm said there were pockets of demand even as inflation risk and term premium were being repriced. That distinction is important for desks managing risk across sovereign books: a disorderly unwind looks different from a market where real money is still stepping in, even if only selectively.

The political backdrop has been doing as much damage as the macro data. Concerns about who will lead Britain’s government, the future direction of fiscal policy and Labour’s local-election losses have all fed into the selloff, alongside lingering memories of the 2022 gilt market meltdown. Allianz has kept a bullish stance on UK bonds and Royal London has been buying more, a sign that some institutional investors still see value even after the sharp move.

The demand picture is also fragmenting by maturity. The Institute for Fiscal Studies said domestic financial institutions, especially banks, have been buying more gilts, but mainly in sub-15-year paper. Longer-dated demand has been weaker, and Bank of England policymaker Catherine Mann has warned that the growing role of price-sensitive international investors could make borrowing costs more volatile if another shock hits.

For Goldman bankers and traders, the implication is broader than one sovereign market. Higher long-end yields can reset valuation models, shift client appetite for equity versus fixed income and alter the timing of cross-border funding. Goldman also said the Bank of England may have room to raise rates this summer if it wants to dampen inflation from soaring energy prices, even as a mid-May Reuters poll found economists still expected Bank Rate to stay at 3.75% in 2026, with more than a third expecting at least one hike. Against that backdrop, the UK Debt Management Office’s 2026-27 plan for £252.1 billion of gilt issuance and £5 billion of net Treasury bill issuance is unlikely to settle the debate. Shorter bills may ease one pressure point, but they do not remove the long-end risk that is now running through global rates books.

Know something we missed? Have a correction or additional information?

Submit a Tip