Goldman Sachs sees Fed cuts delayed to 2027 as inflation stays sticky

Goldman pushed its next Fed cuts to December 2026 and March 2027, keeping financing costs higher for longer across trading and deal desks.

Goldman Sachs’ delayed Fed-cut call has an immediate desk-level consequence: money stays expensive, and the bankers and traders who live off cheaper funding have to wait longer for relief. Goldman now sees the Federal Reserve’s next two rate cuts landing in December 2026 and March 2027, one quarter later than it expected before, after concluding that inflation has stayed stickier than anticipated.

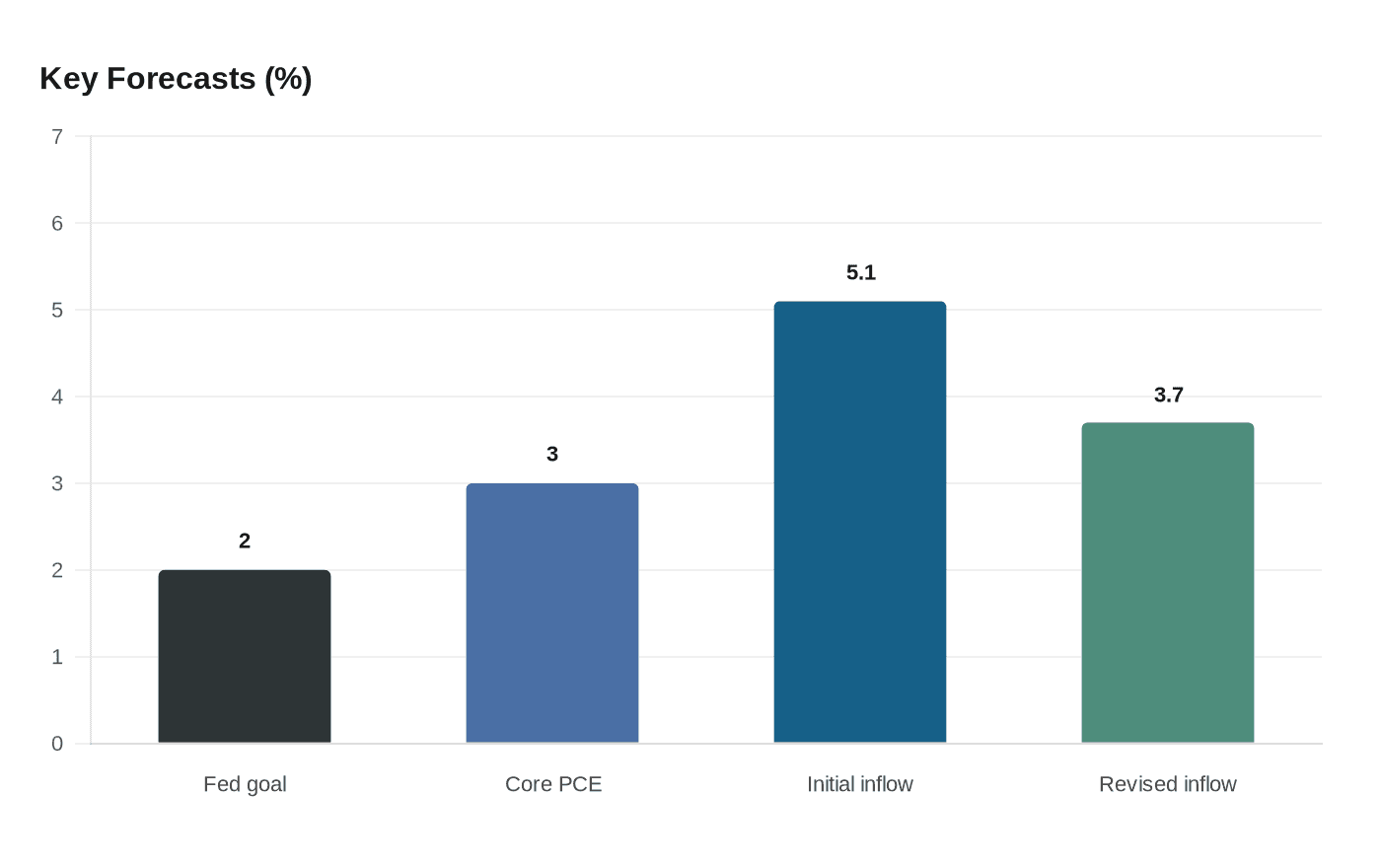

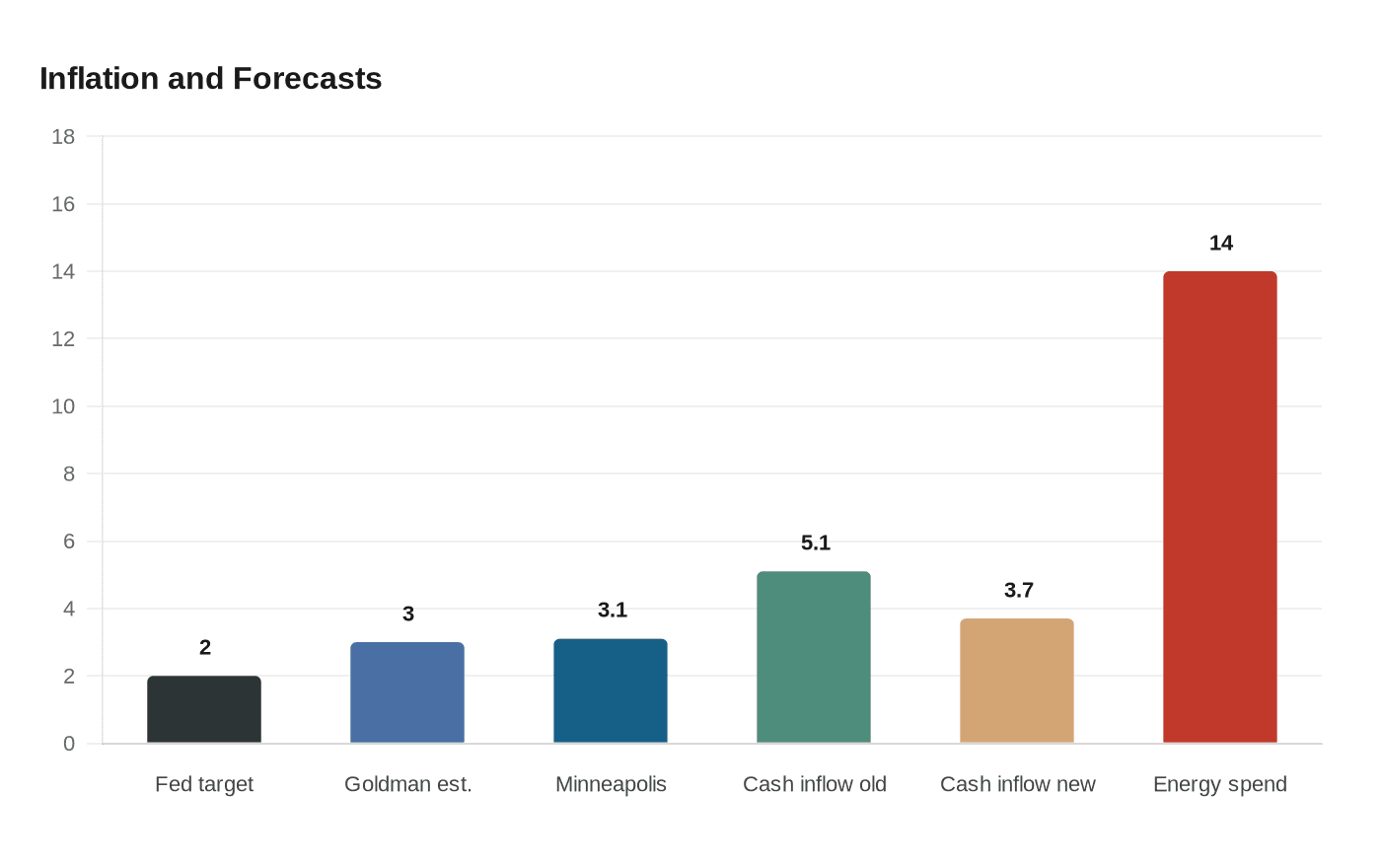

The firm’s U.S. economists said energy cost pass-through is likely to keep core PCE closer to 3% than the Fed’s 2% goal through 2026. That matters because the Fed measures its inflation target using the personal consumption expenditures price index, and policy does not ease quickly when that gauge is still running hot. In March, the Federal Reserve’s own projections covered inflation, growth, unemployment and the expected policy path through 2028, signaling that rate timing remains central to the outlook.

For Goldman employees in rates, macro, mortgage and leveraged finance, the shift changes how deals get priced and when clients move. Higher-for-longer policy tends to narrow issuance windows, raise the hurdle for borrowers and push M&A financing decisions farther out. ECM and DCM teams can expect more selective supply, while coverage bankers may spend more time explaining why waiting for a lower discount rate could backfire if spreads widen or market conditions turn choppier.

The broader Fed backdrop supports that caution. On March 26, Philip N. Jefferson said inflation remained above the Fed’s 2% target and that higher energy prices, along with tariff uncertainty, complicated the outlook. On April 1, Alberto G. Musalem said policy was well positioned and that the current rate range looked appropriate for some time. A Federal Reserve Bank of Minneapolis analysis later put core PCE inflation at 3.1% year over year through January 2026 and estimated tariffs could be adding about 0.5 to 1 percentage point to inflation.

Goldman’s own consumer work points to the same pressure on the real economy. On May 8, Goldman Sachs Research said disruptions to oil flows from the Middle East were filtering through to U.S. consumers and that it had twice cut its 2026 discretionary cash inflow growth forecast, to 3.7% from an initial 5.1%. The firm also said energy spending could rise about 14% this year, with low-income households hit hardest.

For Goldman’s junior bankers and analysts, the message is practical: the rate path is not an abstract macro call. It shapes pricing, client urgency, carry costs and the pace of work across desks, and it can keep bonus-sensitive deal flow under pressure until the Fed finally turns.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?