Goldman Sachs sees South Korea powering humanoid robot growth

Goldman sees South Korea supporting 74,000 humanoid units by 2030 and about 30% of global production by 2035. For Goldman teams, AI now means parts, plants, and clients.

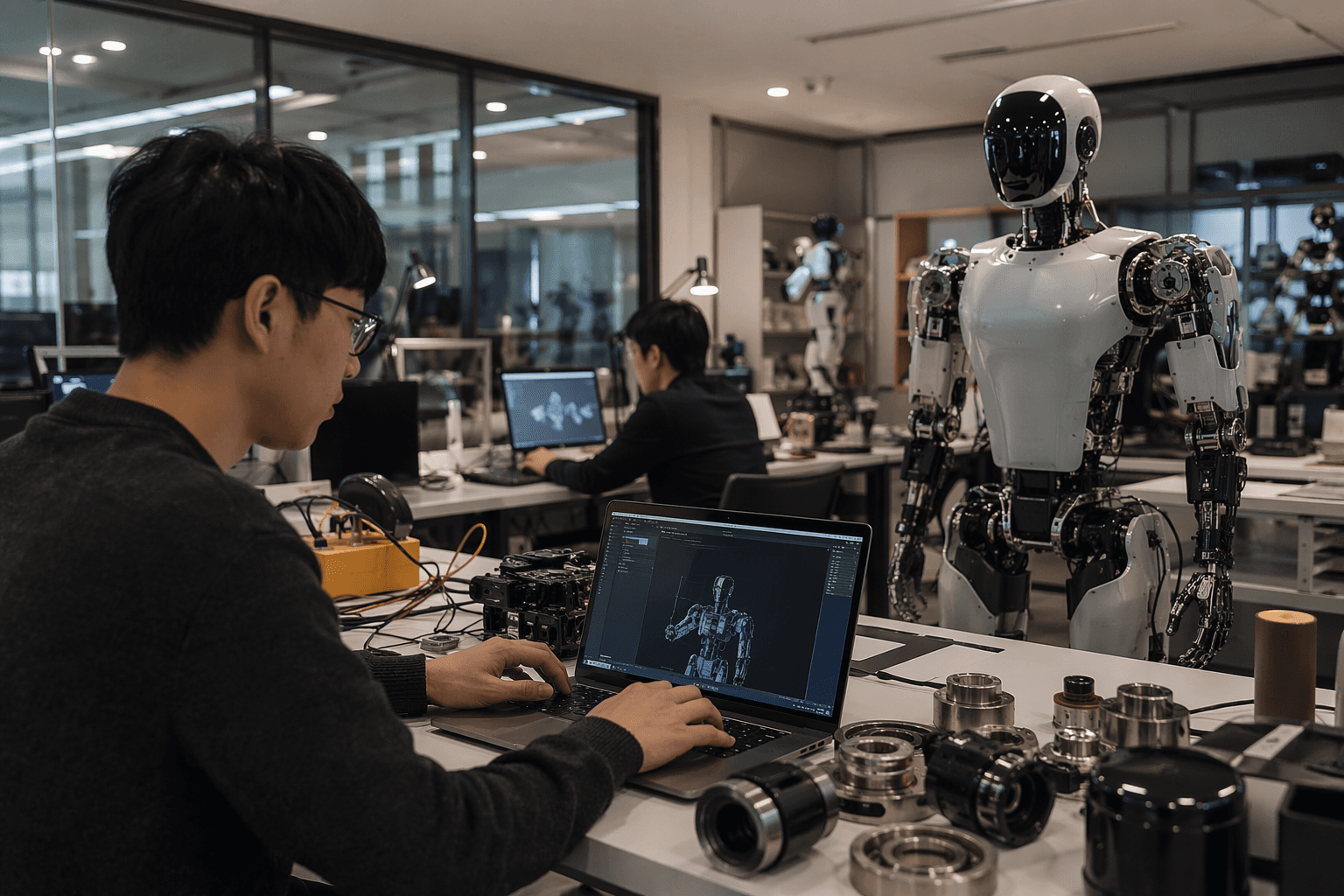

Korean companies could account for about 30% of global humanoid production by 2035, while Korean supply chains may support roughly 74,000 humanoid units by 2030. Goldman Sachs is pushing the AI story out of chatbots and into actuators, sensors, and factory floors, with South Korea emerging as a key test case. Inside the firm, that changes what counts as relevant AI coverage: not just software adoption, but the industrial supply chains, component makers, and manufacturing clients that will build the next wave of humanoid robots.

South Korea is becoming the hardware side of the AI trade

Goldman Sachs Research’s June 25 note argues that South Korea is unusually well positioned for humanoid robot development because its auto-industry base maps onto the parts humanoids need most, including actuators, sensors, and electric motors.

That is a different AI trade from the one that dominated the last two years. The center of gravity moves from model training and cloud infrastructure to precision manufacturing, robotics assembly, and the firms that already know how to build durable parts at scale. For Goldman, that broadens the conversation from software multiples to industrial ecosystems, vendor qualification, and the economics of component bottlenecks.

A country built for automation gives the thesis real traction

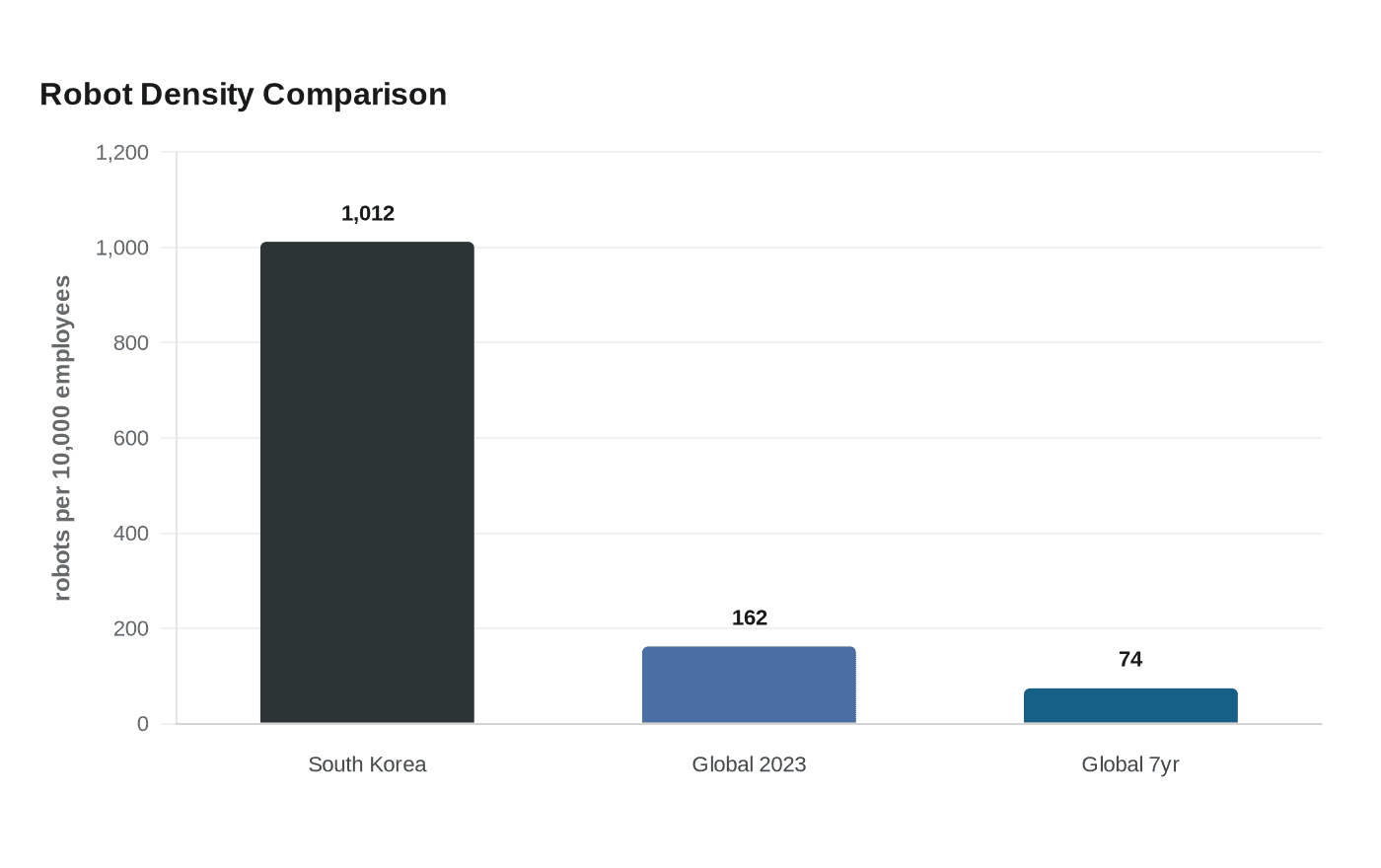

South Korea already has one of the most automated factory bases in the world, which gives humanoids a live production environment instead of a lab-only future. The International Federation of Robotics put South Korea at 1,012 industrial robots per 10,000 employees in 2023, the highest robot density in the world. The federation also put the country’s robot density growth at an average of 5% annually since 2018.

Humanoids are most likely to scale where factories already understand robots, controls, uptime, and maintenance. South Korea is not just a promising market for sales, it is a proving ground for deployment. The same IFR data showed how quickly automation is spreading beyond Korea: the global average robot density reached 162 units per 10,000 employees in 2023, more than double the 74 units recorded seven years earlier.

Goldman’s earlier humanoid call now looks like a commercialization roadmap

The South Korea note builds directly on Goldman’s February 26, 2024 humanoid-robot report, which took a broader view of the market. That earlier work estimated the global humanoid market could reach at least US$6 billion in 10 to 15 years, with humanoids filling 4% of the U.S. manufacturing labor shortage gap by 2030 and addressing 2% of global elderly-care demand by 2035.

Taken together, the two pieces show a clear progression in the bank’s thinking. The 2024 report framed humanoids as an AI accelerant with large end markets; the June 2026 South Korea note narrows the lens to the supply chain that can actually make the machines. For Goldman employees, that means the question is no longer only who buys humanoids, but who supplies the motors, chips, battery systems, and mechanical subassemblies that make commercialization possible.

Policy is turning the sector into an industrial project, not a science project

South Korea’s government is backing that shift with industrial policy. On April 10, 2025, the Ministry of Trade, Industry and Energy announced the K-Humanoid Alliance, a consortium of more than 40 domestic robotics manufacturers, component suppliers, researchers, universities, and government bodies.

The alliance’s goals are concrete: jointly developing AI robot models, humanoid core technology, AI semiconductors, and mobility batteries, while also nurturing companies and specialists and strengthening collaboration between suppliers and clients. The ministry will support the alliance with financial assistance for related R&D.

Who inside Goldman should care, and why

This is not just a robotics story for technology analysts. Inside Goldman, it gives industrials, autos, semis, and tech coverage teams a common framework for where AI capex may surface next. A Korean auto-parts supplier, a battery maker, a sensor business, or a semiconductor input vendor may now matter as much to the AI narrative as a cloud platform or software company.

For bankers, the useful angle is cross-sector coverage. Humanoid-related work can touch equity capital markets, M&A, structured financing, and cross-border advisory in one transaction stream, especially when Korean industrial companies try to move into robotics components or partner with global clients. That kind of work tends to reward bankers who can connect manufacturing economics with AI demand, which is exactly the sort of broad franchise thinking that influences staffing, visibility, and eventually total compensation.

For research, the opportunity is sharper still. Analysts have to separate headline-grabbing robotics optimism from the slower, less glamorous reality of tooling, quality control, supply agreements, and capex timing. They also have to explain whether a component is substitutable, where production can scale, and how much margin pressure comes from localization.

The names to watch are already on the supply side

A Seoul-based robotics ecosystem is already taking shape in companies such as ROBOTIS, a robotics actuator company that promotes humanoid and Physical AI platforms. Its lineup includes semi-humanoid systems and manipulator platforms, which is the kind of product set that shows how the market is shifting from concept to commercialization.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?