Goldman Sachs upgrades AMD to Buy after strong earnings, raises target to $450

Goldman’s bigger bet is not just on AMD’s quarter, but on AI reshaping semis work, client demand, and where research firepower gets focused.

Goldman Sachs’ upgrade of Advanced Micro Devices to Buy, with a price target lifted to $450 from $240, shows how quickly AI demand has turned semiconductors into a hotter internal battleground for research, trading conversations, and client coverage. The new target implied roughly 27% upside from AMD’s prior close, and the stock jumped sharply in premarket trading after the call.

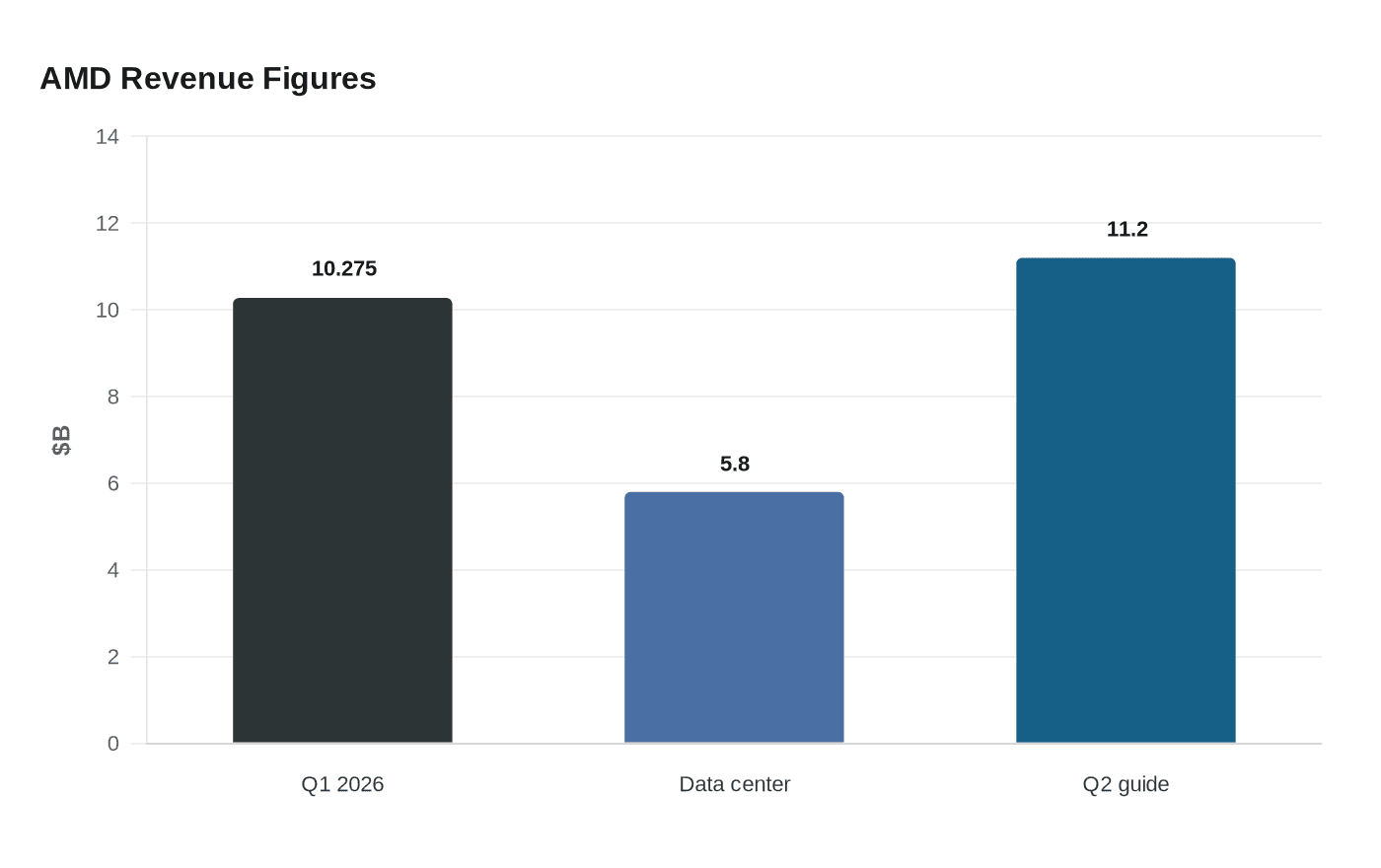

The move followed AMD’s first-quarter 2026 results on May 5, when the Santa Clara, California chipmaker said revenue came in around $10.25 billion to $10.3 billion, ahead of Wall Street expectations. AMD reported non-GAAP earnings per share of $1.37 and said data center revenue rose 57% from a year earlier to about $5.8 billion. It also guided second-quarter revenue to about $11.2 billion, another sign that demand is not easing.

For Goldman, the more important signal is where the demand is coming from. The bank said AMD could benefit from agentic AI-driven demand and from stronger server CPU growth, while also seeing upside in datacenter GPUs in 2027 and beyond. On the earnings call, CEO Lisa Su said AMD was seeing significantly more CPU demand from major cloud providers and enterprise customers, a mix that matters to Goldman analysts because it points to spending that can travel across cloud infrastructure, enterprise IT budgets, and AI buildouts instead of relying on a single product cycle.

AMD also sharpened one of the biggest arguments in its favor: the server CPU total addressable market. The company said it now expects that market to grow at more than 35% annually to over $120 billion by 2030, compared with a previous 18% compound annual growth outlook. That kind of revision tends to reverberate inside banks like Goldman, where semiconductor coverage has become less about cyclical PC demand and more about whether analysts can track cloud capex, accelerator adoption, and the knock-on effects of AI infrastructure spending.

Goldman was not alone in getting more bullish. Bernstein upgraded AMD to Outperform from Market-Perform and raised its target to $525, underscoring how fast the Street is re-rating the name after the earnings report. The broader message for Goldman’s coverage teams is that semis are no longer a side pocket of tech research. With AI winners attracting more attention, more client calls, and more trading interest, the analysts who can connect server CPUs, GPUs, cloud demand, and enterprise adoption are becoming more valuable to the franchise.

Know something we missed? Have a correction or additional information?

Submit a Tip