Goldman Sachs Upgrades Netflix to Buy, Sets $120 Price Target

Eric Sheridan's Netflix upgrade cites an 18% share-price drop as the entry point, with Goldman's new $120 target implying 26% upside ahead of April 16 earnings.

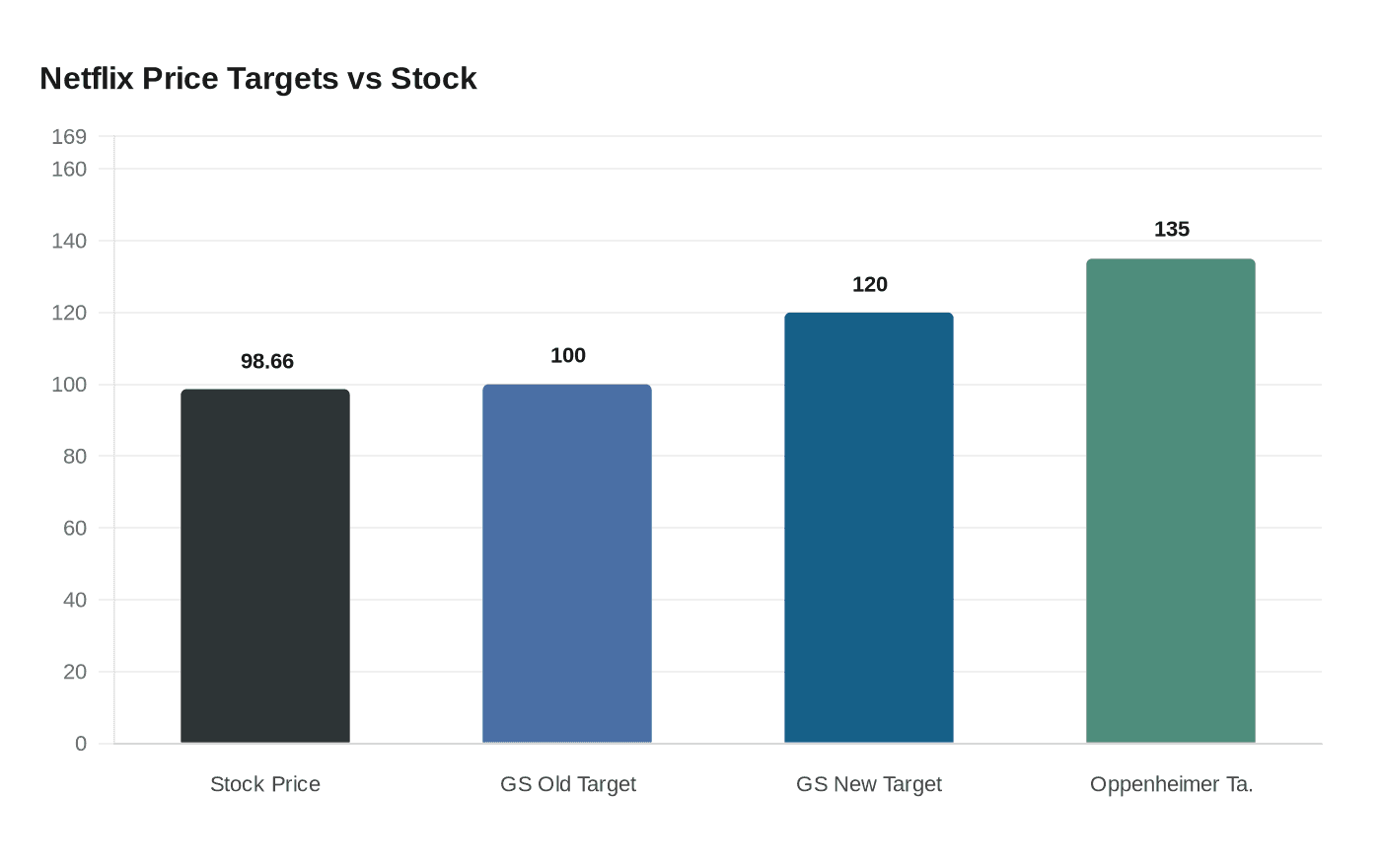

Goldman Sachs analyst Eric Sheridan upgraded Netflix to Buy from Neutral on April 6, lifting his 12-month price target to $120 from $100 after the stock shed roughly 18% over the prior six months. At Netflix's price of around $98.66 at the time of the call, the new target implies approximately 26% upside, just below the 30% average implied upside across Goldman's broader coverage universe. Sheridan's framing was blunt: the pullback created a "more positive risk/reward" dynamic for long-term investors.

The upgrade lands eight trading days before Netflix reports Q1 2026 results, scheduled for April 16 after market close. Wall Street consensus puts Q1 revenue at approximately $12.157 billion, up 15.3% year-over-year, with earnings per share of $0.76, a 15.2% increase from the $0.66 reported in Q1 2025. That follows a strong fourth quarter in which Netflix posted $12.05 billion in revenue, up 18% year-over-year, with 325 million global subscribers on the books.

Sheridan's bull case rests on four strategic pillars: original content driving user growth, expansion into live programming and events, gaming, and advertising. On advertising, the numbers are difficult to argue with. Netflix's ad-supported tier reached 190 million monthly active viewers globally as of November 2025, more than doubling from 94 million in May 2024. Ad revenue approximately doubled in 2025 to around $1.5 billion, and the company has guided for another doubling to roughly $3 billion in 2026. Goldman cited positive channel checks from advertisers at the New York NewFronts events, where media companies pitch their programming to ad buyers annually, as a specific confidence catalyst. Netflix is also testing generative AI-powered interactive mid-roll and pause ads, with a global rollout planned for 2026 across all ad-tier markets.

March 2026 price increases added a separate revenue layer. Netflix raised its Standard ad-free plan by $2 to $19.99 per month, its Premium 4K tier by $2 to $26.99, and its ad-supported plan by $1 to $8.99. It was the second major price adjustment in just 15 months, and Goldman estimates the combined increases could generate approximately $3 billion in additional annual revenue on top of the ad trajectory.

Gaming is a quieter piece of the thesis but moving in the right direction. Netflix expanded its gaming offering to television sets in 2025 with multiplayer party games using smartphones as controllers, and game downloads rose 17% to 74.8 million between January and October 2025. Against all of this, Netflix has committed to spending approximately $20 billion on content in 2026, anchoring the subscriber retention argument.

Goldman also projects that Netflix will repurchase 20% to 25% of its shares over the next five years, adding a capital return dimension to a stock that already trades at roughly 38 times earnings on a market cap of approximately $392.5 billion. The company's full-year 2026 revenue guidance of $50.7 billion to $51.7 billion gives Sheridan's price target a concrete foundation.

Goldman was not alone in its conviction. Erste Group also upgraded Netflix to Buy around the same period, while Oppenheimer maintained an Outperform rating with a $135 price target, $15 above Goldman's fresh call, suggesting the Street's optimism on Netflix's advertising and pricing execution runs well beyond a single house view.

Know something we missed? Have a correction or additional information?

Submit a Tip