Lloyd Blankfein reflects on Goldman Sachs culture, crises and AI

Lloyd Blankfein’s Goldman legacy points to the same rule under AI: speed up the work, but keep judgment, risk control and client trust tightly held.

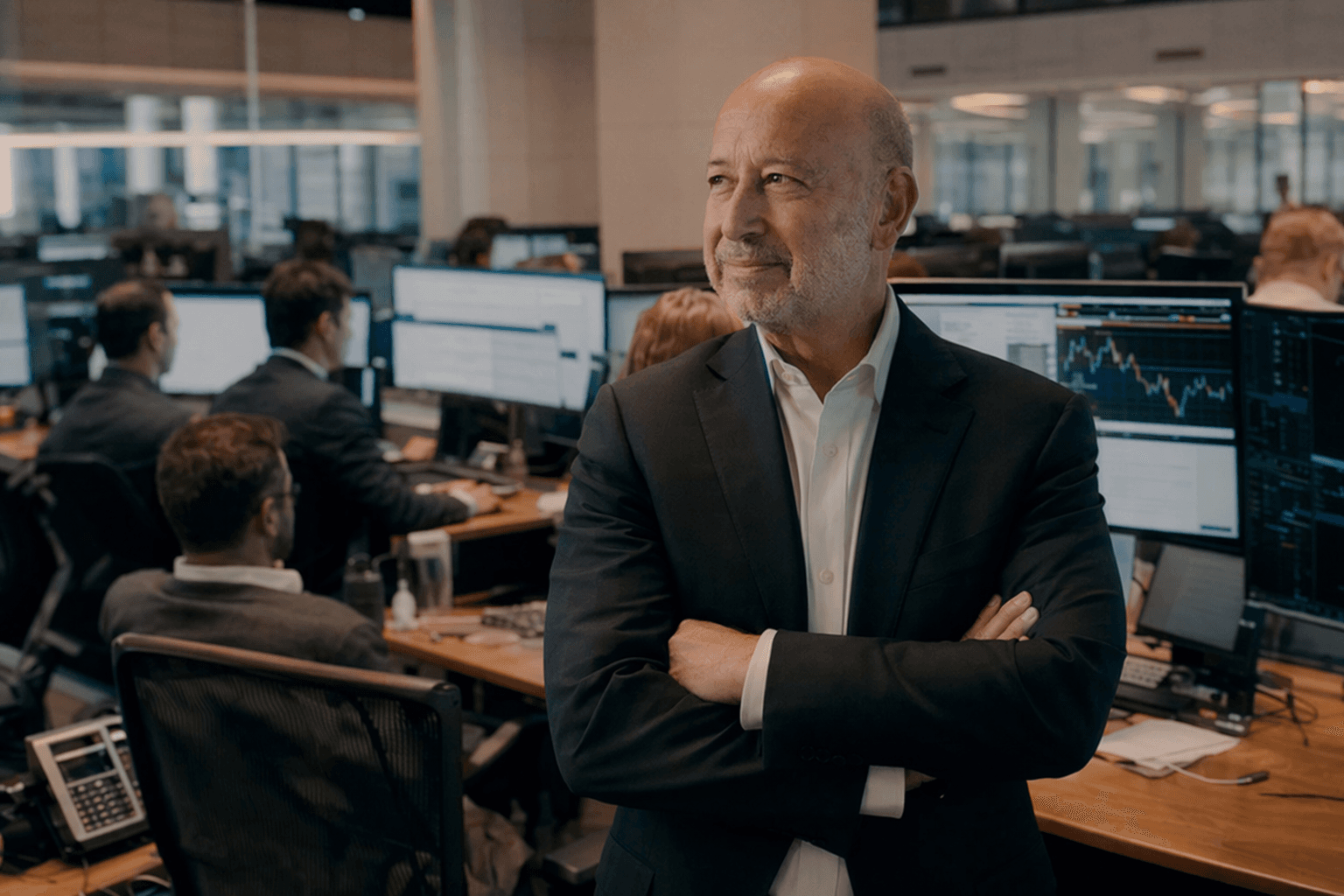

Blankfein is the cleanest window into Goldman’s next operating model

Lloyd Blankfein’s career says a lot about how Goldman Sachs thinks it should evolve under AI: keep the firm elite, make the work faster, but never relax the demand for judgment. He came up the hard way, from the Bronx and Brooklyn to Harvard College and Harvard Law School, then from corporate tax law into J. Aron & Co. and eventually into the foreign exchange business that helped define Goldman’s trading culture. That path matters because it shows the firm’s old guard still values people who can move between technical detail, client pressure and risk.

Why Blankfein still resonates inside Goldman

Blankfein became chairman and CEO in 2006 after Hank Paulson left for the U.S. Treasury, then stepped down as CEO on September 30, 2018 and retired as chairman at the end of that year. His rise coincided with one of the most severe tests in modern banking, the 2008 financial crisis, when Goldman transitioned into a bank holding company and had to operate under far heavier scrutiny. That era still defines how many Goldman veterans think about the business: growth is welcome, but only if the firm can still manage its exposures when markets break.

His background also reflects the internal mythology Goldman likes to tell about itself. Born in 1954, raised in New York City, educated at Harvard, and trained as a lawyer before moving into markets, Blankfein is the kind of leader who understood the firm not as a club but as a machine for decision-making under pressure. In Goldman terms, that means mentorship matters, entrepreneurial initiative matters, and so does the ability to make a call before the rest of the market has settled on one.

What Goldman says it has always been, and what that means now

Goldman traces its origins to 1869 and describes its culture as built around teamwork, client service and giving back. That sounds broad, but inside the firm those values usually translate into something more concrete: who gets staffed on the hard deals, who earns trust with clients, and who can represent the franchise without improvising the wrong answer. Blankfein’s generation did not just inherit that culture, it hardened it through the crisis years, when the downside of a bad decision was no longer theoretical.

That helps explain why Goldman continues to frame innovation as part of its identity rather than a break from it. The firm points to milestones such as creating the first price-to-earnings ratio and helping reinvent the modern IPO. Under Blankfein, that instinct expanded beyond classic investment banking into adjacent businesses and platforms, from principal investing to digital tools. The message to employees is simple: Goldman does not want technology to flatten its identity, it wants technology to extend it.

The crisis-era instinct that still shapes risk decisions

The most important through-line from Blankfein’s era is risk discipline. During the financial crisis, Goldman’s move into a bank holding company forced the firm to live with more regulation, more capital pressure and less room for casual bets. That legacy still matters for analysts and associates who live inside deal pipelines and market calls, because it suggests that even as the firm adopts new tools, the approval culture around risk is unlikely to loosen.

Goldman’s Merchant Banking Division is a good example of how that balance has worked in practice. Announced on September 9, 1998, it later grew to approximately $100 billion in assets under management after the financial crisis. That kind of expansion shows the firm’s willingness to push into capital-intensive businesses, but only in a framework that still treats risk as something to monitor continuously, not something to outsource to optimism. For people building careers there, the lesson is that initiative is rewarded, but only when paired with discipline and a clear line of sight on downside.

What leadership has already changed under Blankfein’s watch

Blankfein’s tenure also included a series of initiatives that broadened Goldman’s footprint beyond deal-making alone. The firm launched 10,000 Women in 2008 and 10,000 Small Businesses in 2010, both of which signaled a more explicit interest in economic participation outside the firm’s walls. Goldman also launched the Business Standards Committee in 2010, Marquee in 2014 and Marcus in 2016, each reflecting a different response to the post-crisis environment, from reputational repair to digital distribution and consumer-facing finance.

Taken together, those moves show that Goldman has already spent years trying to reconcile two identities: a high-touch advisory bank and a more technology-enabled financial platform. For employees, that means the firm has been asking for a while whether work that once depended on manual effort, distribution muscle or relationship cover can be codified, scaled or productized. AI is not introducing that question, it is accelerating it.

What AI changes, and what it probably does not

David Solomon said in 2025 that AI could draft about 95% of an IPO prospectus in minutes, compared with the weeks-long effort of a six-person team. That is the kind of statistic that should get attention inside Goldman because it does not just point to efficiency gains, it points to a very different division of labor. If a model can draft the bulk of a first pass, then junior bankers may spend less time assembling materials from scratch and more time validating inputs, shaping judgment calls and preparing for the parts of the process that still require a human signature.

Goldman has said its AI use cases include compliance, coding productivity and client-facing tools. Those are not decorative examples. Compliance suggests review work, coding productivity suggests faster internal build cycles, and client-facing tools suggest that the interface between Goldman and the outside world may become more automated even if the relationship itself remains human. For analysts and associates, that likely means fewer hours spent on repetitive drafting and more pressure to understand what the machine produced, where it is wrong and how to use it in a way that still clears the firm’s standards.

The real tension for Goldman people

This is where Blankfein’s comments matter most. Goldman’s old guard does not appear to be arguing that AI should replace the franchise’s core judgment. It is arguing that the firm should use AI to remove drag from the work while keeping the same bar for risk, client service and internal accountability. That is a very Goldman answer: change the workflow, preserve the hierarchy of responsibility.

For people inside the firm, the practical consequence is likely a familiar one in a new form. The work will get faster, the outputs will get more standardized, and the margin for weak judgment may get smaller. But the things Goldman still treats as non-negotiable, judgment under pressure, risk awareness, client trust and the ability to operate in a high-stakes culture, are exactly the things Blankfein’s career was built to protect. That is the playbook the old guard is handing down as AI becomes part of the daily operating model.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?