U.S. private credit lenders post worst unrealized losses since 2022

Paper losses in private credit hit their worst level since 2022, sharpening scrutiny on Goldman Sachs’ alternatives push and the risk discipline behind it.

The latest private credit markdowns are landing squarely on Goldman Sachs’ biggest growth story. As unrealized losses widened across U.S. lenders, the question inside the firm is not whether alternatives still matter, but how much harder it will be to prove that the money can be raised, priced and managed without loosening standards.

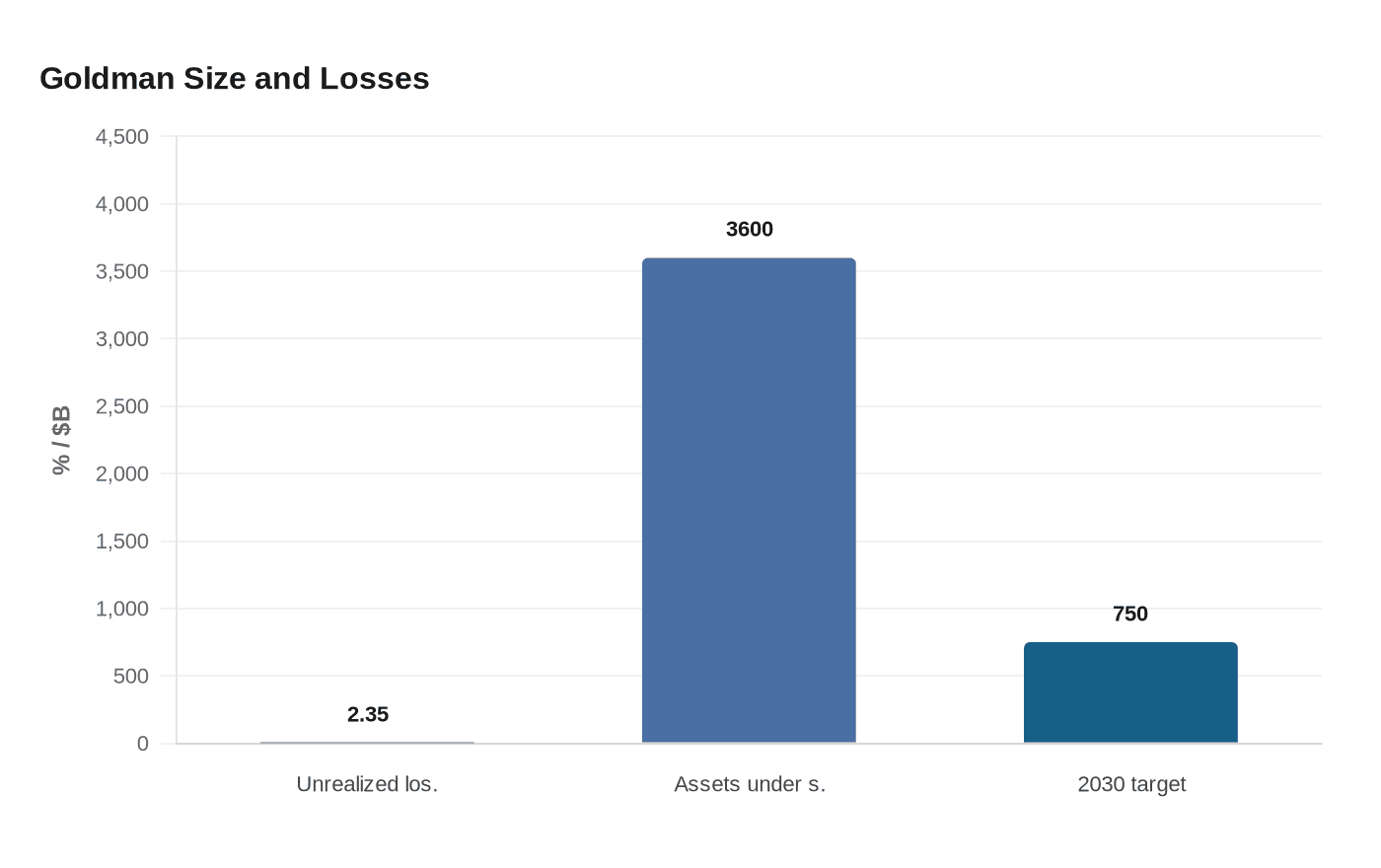

Reuters’ review of 51 U.S. business development companies showed aggregate unrealized losses at 2.35% of net asset value in the first quarter of 2026, the steepest quarterly hit since the second quarter of 2022. Payment-in-kind income also stayed elevated, even after easing from recent highs. Together, those signals point to more pressure on profitability and asset quality, and to a market where refinancing conditions, borrower health and mark-to-market assumptions are getting tougher to defend.

That matters directly for Goldman Sachs because private credit sits inside a broader alternatives strategy the firm has been building aggressively. In its 2025 annual report, Goldman said it had $3.6 trillion in assets under supervision and described wealth, alternatives and solutions as growth opportunities. The firm has also said it wants its private markets and alternative investment business to reach $750 billion in assets by 2030. For teams in Goldman Sachs Asset Management, Goldman Sachs Alternatives and financing, that target depends on convincing clients that risk is being priced better than in public markets, even as paper losses rise.

Goldman has tried to keep that message measured. In a recent commentary, Goldman Sachs Asset Management said private credit is unlikely to pose significant financial system risk because investments are not concentrated, leverage is limited and assets and liabilities are well matched. But the Reuters findings sharpen the pressure points Goldman staff will watch next: underwriting standards, valuation discipline, exposure to payment-in-kind-heavy portfolios and how much of the book is tied to borrowers in software and other sectors facing AI disruption.

The firm is still expanding. On May 12, 2026, Goldman Sachs Alternatives acquired FGI Worldwide LLC, a provider of working capital financing and trade credit insurance solutions, adding another specialty finance piece to the platform. For bankers, investment professionals and risk managers, that is the tension now: every new step into private credit adjacent businesses has to clear a harsher test on drawdowns, non-accruals and sector concentration, or the growth story starts to look more fragile than strategic.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip