IRS proposes raising estate tax closing letter fee to $76

The IRS wants to lift the estate tax closing letter fee to $76, a small hike that can still ripple through estate-administration timelines and client conversations.

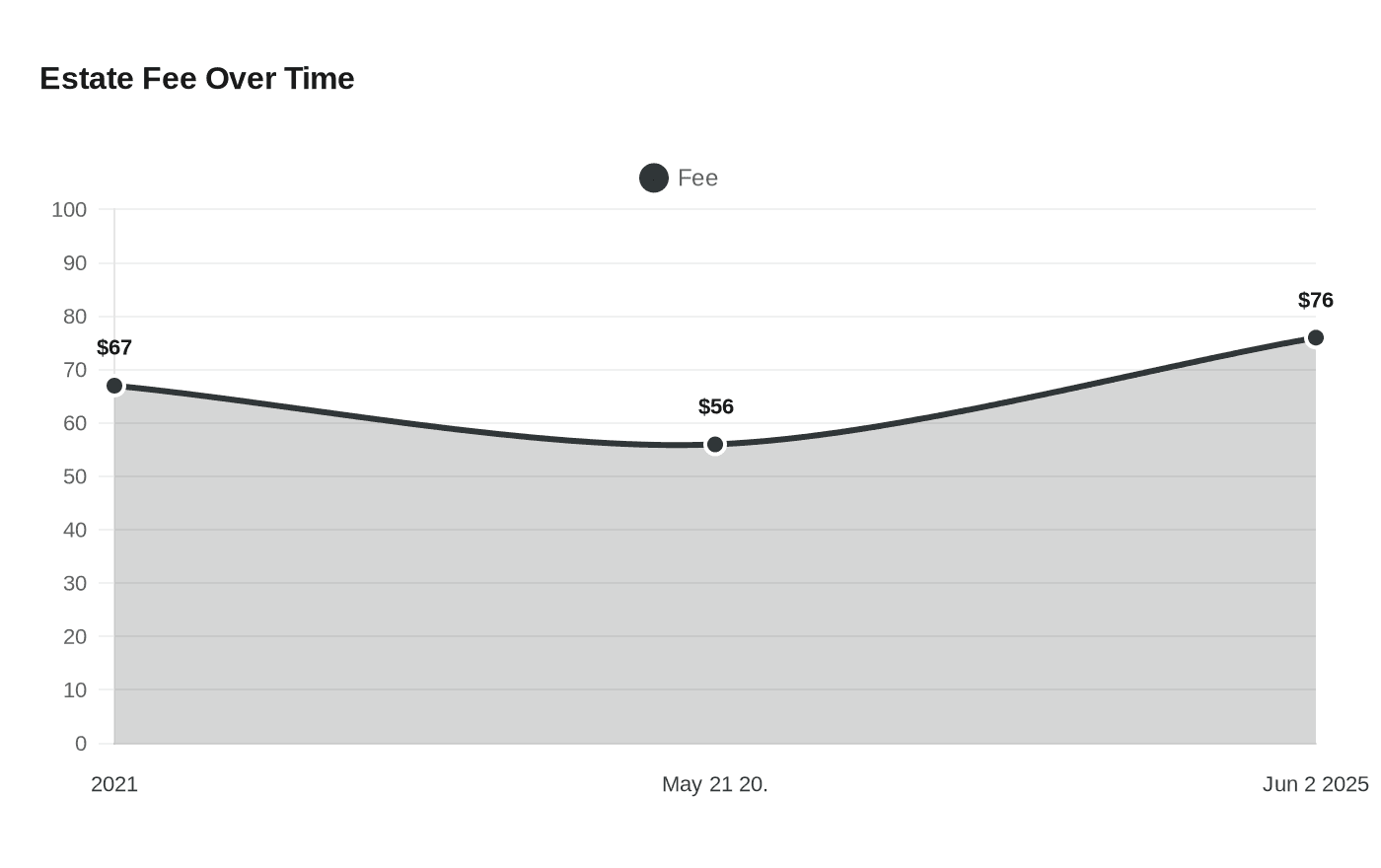

The Internal Revenue Service proposed increasing the estate tax closing letter fee, known as Letter 627, from $56 to $76, a change that looks modest on paper but can still shape how KPMG tax teams handle estate and trust matters. For advisers working with high-net-worth families, the fee is another line item to explain when an executor wants certainty that a Form 706 has been accepted and the file can be closed cleanly.

The proposal appeared in REG-103193-26 on June 2. The IRS said its 2025 biennial review put the full annual cost of the closing letter program at $615,593, based on an estimated 8,053 annual requests, which comes out to $76 per request. The agency also said the service confers special benefits beyond those available to the general public, and it cited the Independent Offices Appropriations Act of 1952, which allows agencies to charge user fees and says services should be self-sustaining to the extent possible.

For practitioners, the arithmetic matters less than the workflow. A closing letter is often part of the last documentation package in an estate administration, and even a $20 increase can ripple through engagement letters, billing discussions, and the timing of final sign-off. When clients are already sensitive to both cost and delay, tax professionals end up spending time justifying why the request is worth making at all, especially when the letter is no longer automatic.

That change in behavior is built into the process. The IRS has said that for estate tax returns filed on or after June 1, 2015, closing letters are issued only upon request. In many cases, IRS account transcripts can substitute for the closing letter, including to show acceptance of Form 706 and completion of an examination. Even so, many attorneys, executors and tax advisers still treat the letter as the cleanest endpoint, which is why a fee increase can affect not just dollars but the cadence of closing an estate.

The timing also matters. The proposed regulations would apply to requests received by the IRS on or after the date that is 30 days after final regulations are published in the Federal Register. The IRS said it will consider timely comments before finalizing the rules and will schedule a hearing if one is requested in writing. The fee had only recently moved down to $56 on May 21, 2025, after being set at $67 in 2021, so this new proposal would add another procedural adjustment for tax professionals who already track a steady stream of small but consequential IRS changes.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)