IRS releases look-back interest calculator for long-term contracts

The IRS has launched an Excel look-back interest workbook that could cut rework for long-term contracts, but KPMG teams will still need judgment on the facts.

The IRS has put a new Excel workbook in the hands of tax teams that live with long-term contract complexity: the Percentage-of-Completion Method Look-Back Interest Calculator XLSX, released May 29. For KPMG auditors, tax advisers, and client finance teams, the practical appeal is not that the math got easier in a vacuum, but that one of the most tedious parts of Form 8697 now has a standard starting point.

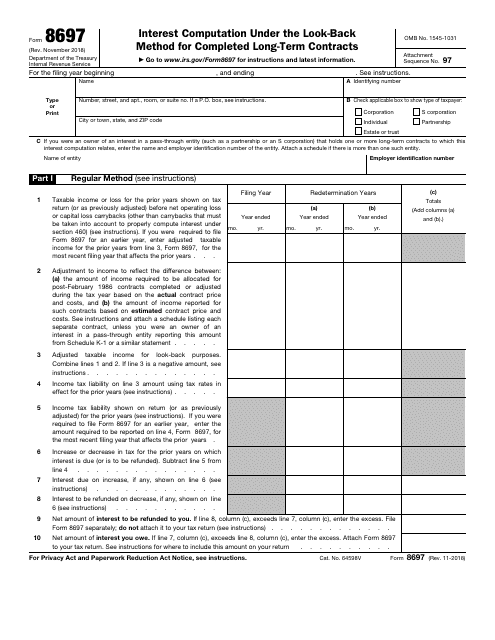

The calculator supports the interest computation required for Form 8697, the return used to figure interest due or refundable under the look-back method for completed long-term contracts. The IRS says the process still follows three steps: reallocate income using actual revenues and costs, compute the hypothetical overpayment or underpayment of tax, then calculate interest on that amount. That sequence matters for construction clients, industrial manufacturers, and other project-based businesses where percentage-of-completion estimates made years earlier may not line up with the final contract outcome.

That mismatch is where the new workbook could save time. A small change in estimated margin, cost allocation, or contract price can cascade into a different look-back result and trigger fresh reconciliation work between project accounting and tax accounting. For KPMG teams reviewing prior-year positions, the workbook can reduce manual spreadsheet rebuilding, narrow the source of disputes, and make it easier to explain why a later completion-year adjustment or a dispute settlement changes the interest outcome. It can also create a more consistent paper trail for review, which matters when multiple service lines touch the same engagement.

The IRS was equally clear about the limits. The calculator does not cover every fact pattern, does not replace authoritative guidance, and does not guarantee compliance. Taxpayers still need their calculations to agree with I.R.C. Section 460 and Treasury Regulations Section 1.460-6, especially where estimates, post-completion adjustments, or contract-specific complications drive the result. The look-back rules themselves are not new: Section 460 was enacted by the Tax Reform Act of 1986, the Taxpayer Relief Act of 1997 added a de minimis election in some cases, and final regulations became effective Jan. 11, 2001.

For KPMG, the release is less about automation than workflow discipline. It pushes routine arithmetic toward a shared IRS tool and raises the value of review, documentation, and exception handling. The IRS also said taxpayers can send feedback to Stakeholder Liaison with the subject line “Look-Back Interest Workbook Feedback,” a sign that the agency expects practitioners to keep testing where the workbook fits and where human judgment still has to lead.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)