IRS sets 2027 HSA and HDHP limits for KPMG client planning

Workers can put $100 more into self-only HSAs and $250 more into family accounts in 2027, but the bigger lift is updating payroll, enrollment, and plan design.

A worker with self-only HSA coverage can save $100 more in 2027, and a family can save $250 more, but the real work for KPMG client teams is turning those higher limits into clean payroll deductions, enrollment materials, and plan designs before open enrollment starts.

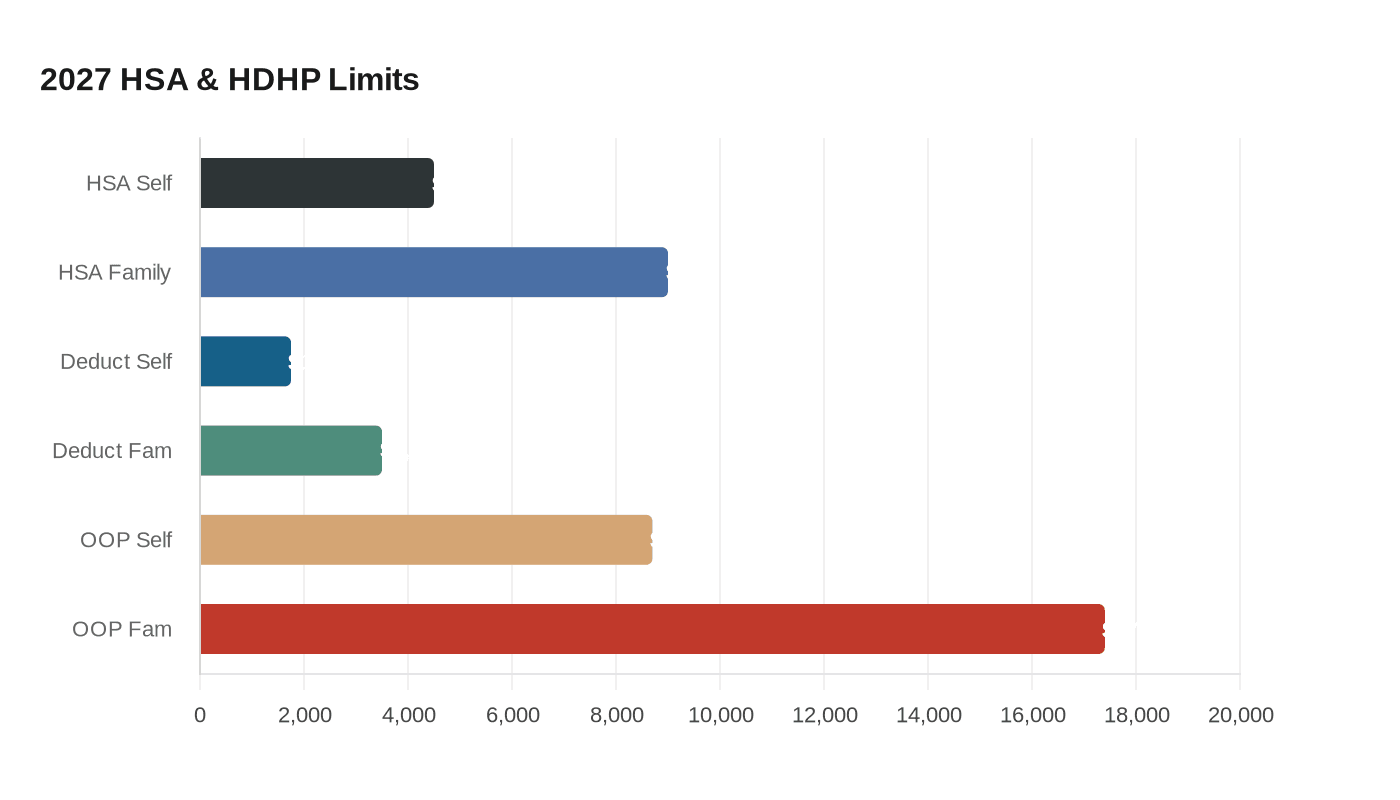

The Internal Revenue Service issued Rev. Proc. 2026-24 on May 29, 2026, setting the 2027 inflation-adjusted limits for health savings accounts and high-deductible health plans. KPMG’s TaxNewsFlash flagged the update the same day, with the self-only HSA contribution cap rising to $4,500 and the family cap to $9,000. The annual limits apply for calendar year 2027, even when an HDHP runs on a non-calendar-year plan year.

That distinction matters for payroll and benefits teams. A July 1 plan year, for example, would not change the HSA contribution cap midstream, but it would pick up the 2027 HDHP minimum deductible and out-of-pocket rules on July 1, 2027, and carry them through June 30, 2028. Those thresholds move to $1,750 for self-only coverage and $3,500 for family coverage on the deductible side, with out-of-pocket maximums of $8,700 and $17,400. If a client updates contribution limits but misses the plan-design tests, the paperwork may look current while the plan itself is out of step.

For KPMG advisers, the new limits are more than an annual inflation notice. They affect how HR frames HSA compatibility, how payroll systems handle deductions, and how compensation teams explain the value of benefits to employees who weigh richer medical coverage against tax-advantaged savings. Higher limits can be especially relevant for more senior staff and higher-utilization households, where the ability to shelter more pretax dollars can change the enrollment decision.

Rev. Proc. 2026-24 also revised the maximum amount that may be newly available for excepted-benefit HRAs and the aggregate monthly fee allowance for direct primary care service arrangements, widening the impact beyond standard HSA administration. For KPMG’s tax, payroll, and benefits professionals, the message is straightforward: the numbers changed on May 29, and the work now is making sure clients can explain those changes clearly enough to avoid confusion when employees make coverage decisions for 2027.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip