IRS updates energy community bonus credit rules, affecting tax deals

New IRS energy-community maps could swing bonus credits by 10% or 10 points, forcing KPMG deal teams to recheck site assumptions, models and closing checklists.

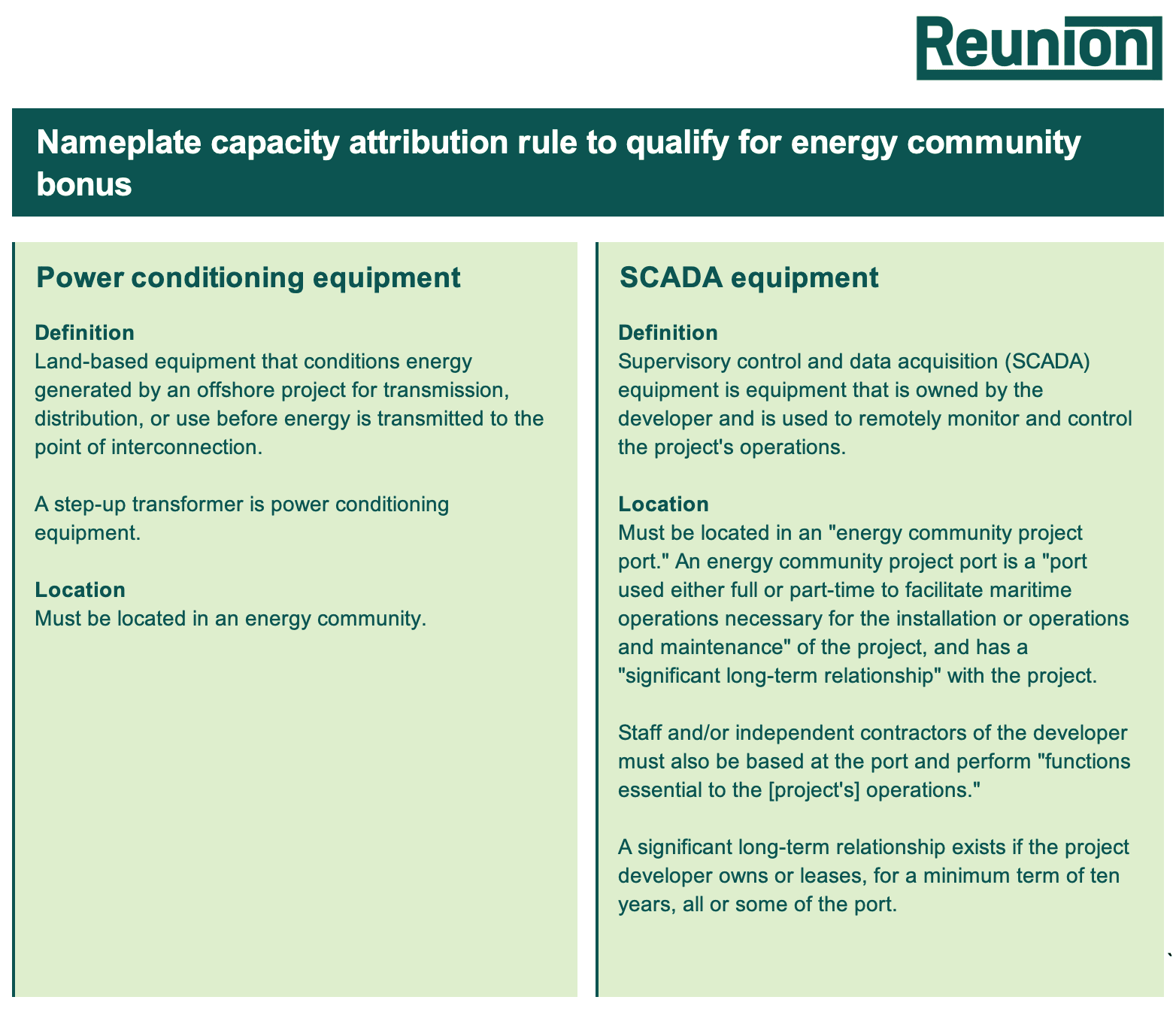

A small IRS guidance update is carrying outsized consequences for project finance. Notice 2026-39 changes the annual materials taxpayers use to test whether a project qualifies for the energy community bonus under sections 45, 45Y, 48 and 48E, which can lift certain production credits by up to 10% and certain investment credits by 10 percentage points.

The notice, issued June 10, updated Appendix 1 for the Statistical Area Category and Appendices 2 and 3 for the Coal Closure Category. For developers, investors and lenders, that means the location screen is not a one-time exercise. Sites that now fall inside an eligible energy community may pick up a higher credit rate, while projects built around older tract assumptions may need to be rechecked before closing or placed-in-service dates lock in the economics.

That is the kind of change that lands quickly in KPMG tax, infrastructure, renewables, project finance and M&A workflows. Deal teams may need to rerun map-based diligence, refresh census tract assumptions and confirm that the right appendix is being used in model outputs. Compliance and controversy teams will also want cleaner files, because bonus-credit support can become expensive to defend if the location analysis is off by even a small factual detail.

The update matters because energy community eligibility can change site selection, transaction pricing and financing structures. If a project only works with the bonus credit, then a shift in status can alter the return profile for the sponsor and the tax equity investor at the same time. That makes the notice more than a technical refresh: it is a cue to revisit assumptions already built into term sheets, closing checklists and diligence memos.

The IRS also drew some clear lines around what this notice does not cover. It does not address the Brownfield Category described in Notice 2023-29, and the appendices are not for purposes of the section 48C advanced energy project credit. The agency has been updating this framework in stages through prior notices, including Notice 2024-30, Notice 2024-48 and Notice 2025-31, as the Inflation Reduction Act credit regime continues to settle into practice.

KPMG flagged Notice 2026-39 the same day it was issued, a sign that tax teams are treating it as an immediate action item rather than routine administrative cleanup. The notice is expected to appear in the Internal Revenue Bulletin on June 29, and by then many deal teams will already be revisiting the assumptions behind their credit models.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)