KPMG flags IRS updates on carbon credits, energy tax rates

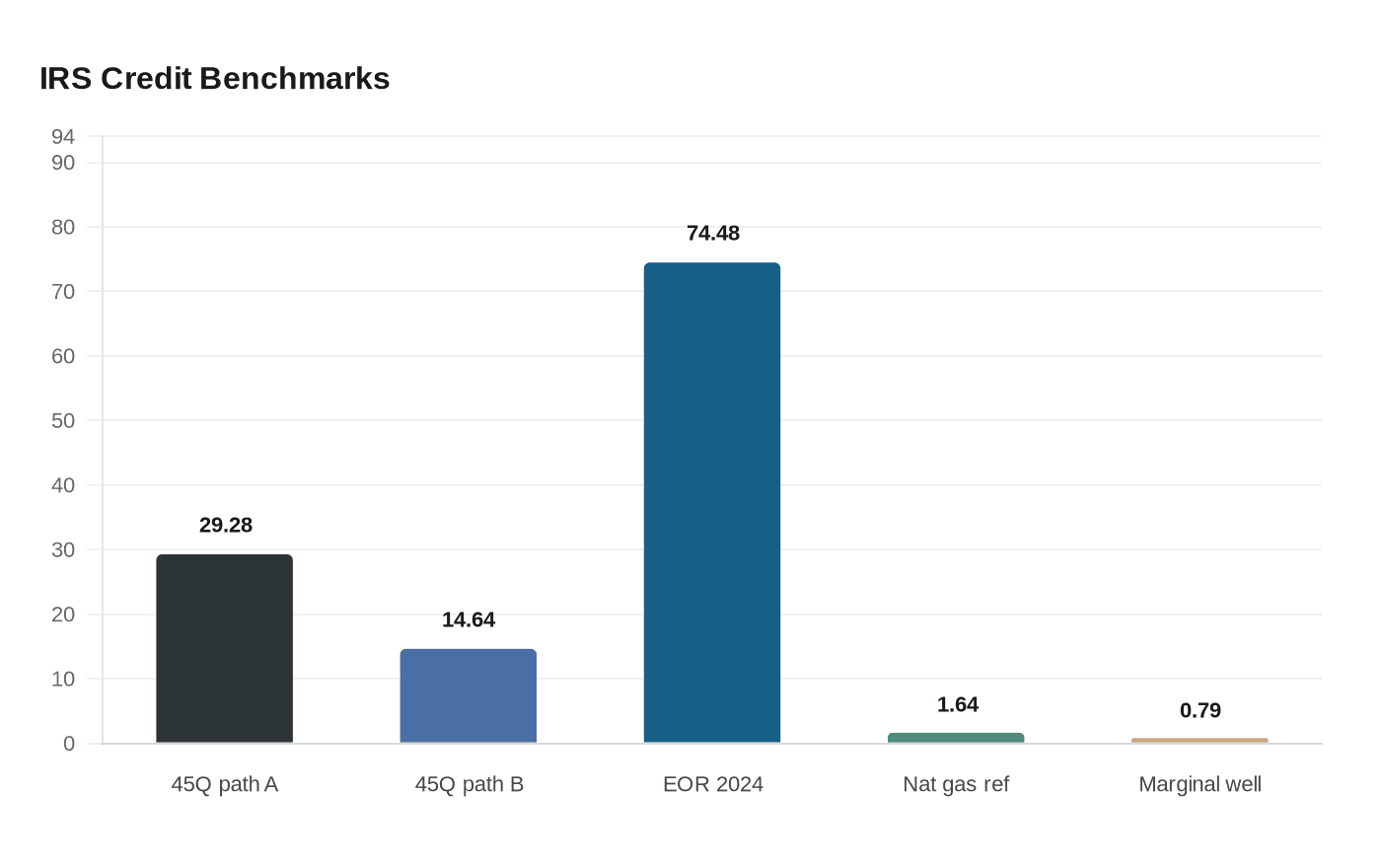

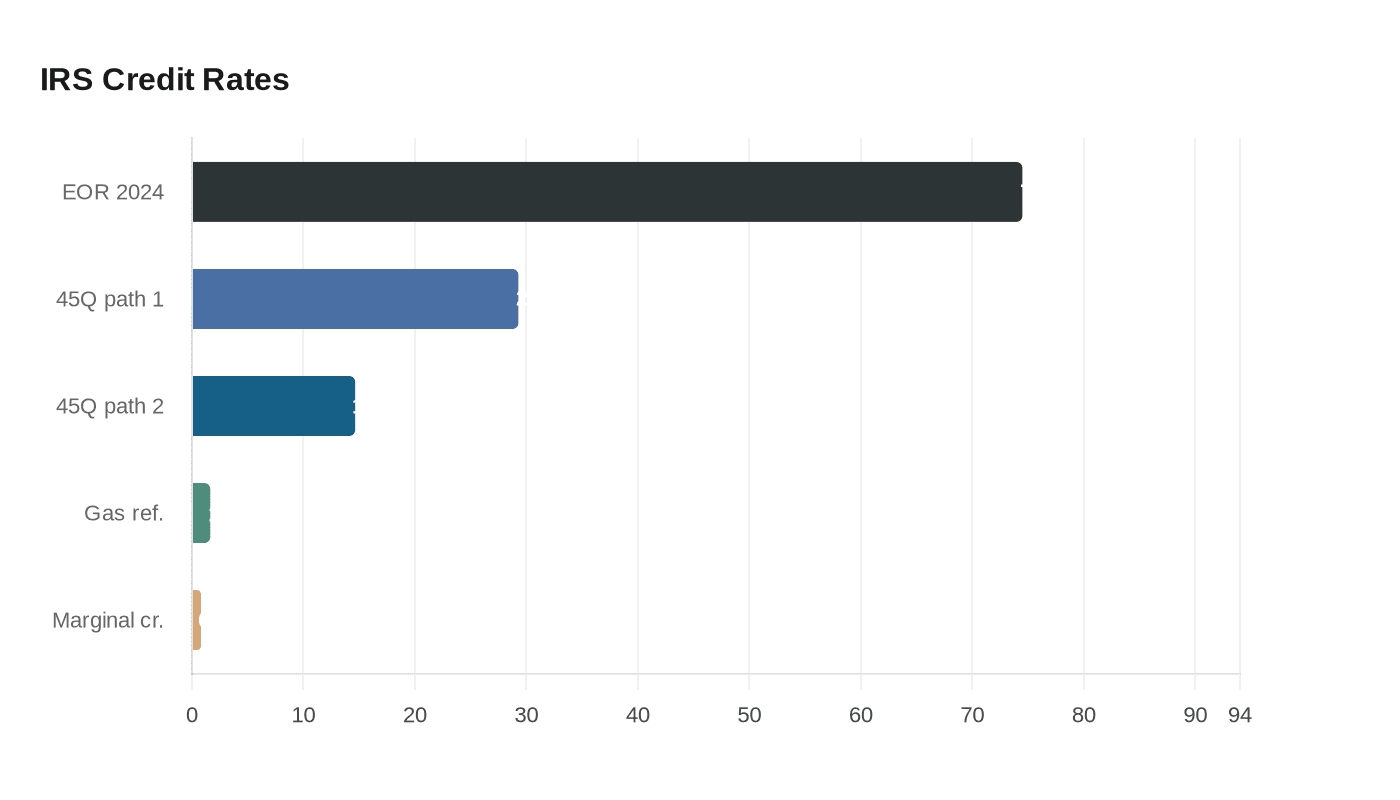

The IRS set the 2026 45Q inflation factor at 1.4639, changing carbon credit values to $29.28 or $14.64 a ton and resetting model assumptions for energy clients.

KPMG is telling energy, ESG and tax teams to recalculate their assumptions after the Internal Revenue Service issued fresh reference points for carbon credits and energy-related tax rates. The key number for carbon capture work is the 2026 inflation adjustment factor under section 45Q: 1.4639. That factor translates into credit values of $29.28 per metric ton under one election path and $14.64 per metric ton under another, giving deal teams a new benchmark for live project models.

The notices matter because they do more than update a worksheet. Notice 2026-29, published in Internal Revenue Bulletin 2026-22 on page 1537, sets the inflation adjustment factor for the carbon oxide sequestration credit for calendar year 2026. Notice 2026-30, on page 1539 of the same bulletin, publishes the 2025 reference price under section 45K(d)(2)(C). That reference price feeds calculations for enhanced oil recovery credits, marginal well production credits and the applicable percentage used in percentage depletion for marginal properties.

For KPMG professionals, the practical effect lands across functions at once. Tax teams need the new figures when they model project economics, estimate credit value and update forecasts for clients weighing carbon capture, utilization and storage investments. ESG advisers need the same numbers because carbon credits and energy-transition incentives sit at the intersection of sustainability strategy, tax planning and financial reporting. Audit teams may also feel the impact in tax provisions, valuation assumptions and disclosures tied to environmental projects or regulated programs.

The update is especially relevant for carbon capture projects in the United States and U.S. possessions, since section 45Q applies only to qualified carbon oxide captured, disposed of, injected or utilized there. That makes the notice a fresh reference point for domestic CCS decisions, where a small change in the inflation factor can move payback periods, influence capital allocation and decide whether a project clears an internal hurdle rate.

The 2025 reference price notice carries its own weight. In 2025, the IRS said the 2024 reference price for the enhanced oil recovery credit was $74.48, which fully phased out that credit for qualified costs paid or incurred in 2025. Last year, the marginal well production credit was based on a $1.64 per thousand cubic feet natural gas reference price and a 1.5821 inflation adjustment factor, producing a $0.79 credit per eligible mcf. Those kinds of annual benchmarks can swing economics quickly, which is why KPMG flagged the notices as more than technical housekeeping. For firms serving energy clients, they now shape the assumptions behind tax forecasts, sustainability claims and the coordination that has to happen between tax, ESG and reporting teams.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)