KPMG says Tax Court ruling raises research credit documentation stakes

A Tax Court denial in part turned on who owned the research rights, not just whether the work was technical, putting contracts and file support at the center of credit defense.

The Tax Court cut into a research credit claim because two of six sample projects did not satisfy the substantial-rights test, a result that put contract language and project files ahead of broad claims about technical work. For architecture, engineering and other project-based businesses, the message is blunt: a credit can fail even when the underlying design work is sophisticated if the arrangement looks funded and the taxpayer cannot show enough legal and economic control over the research.

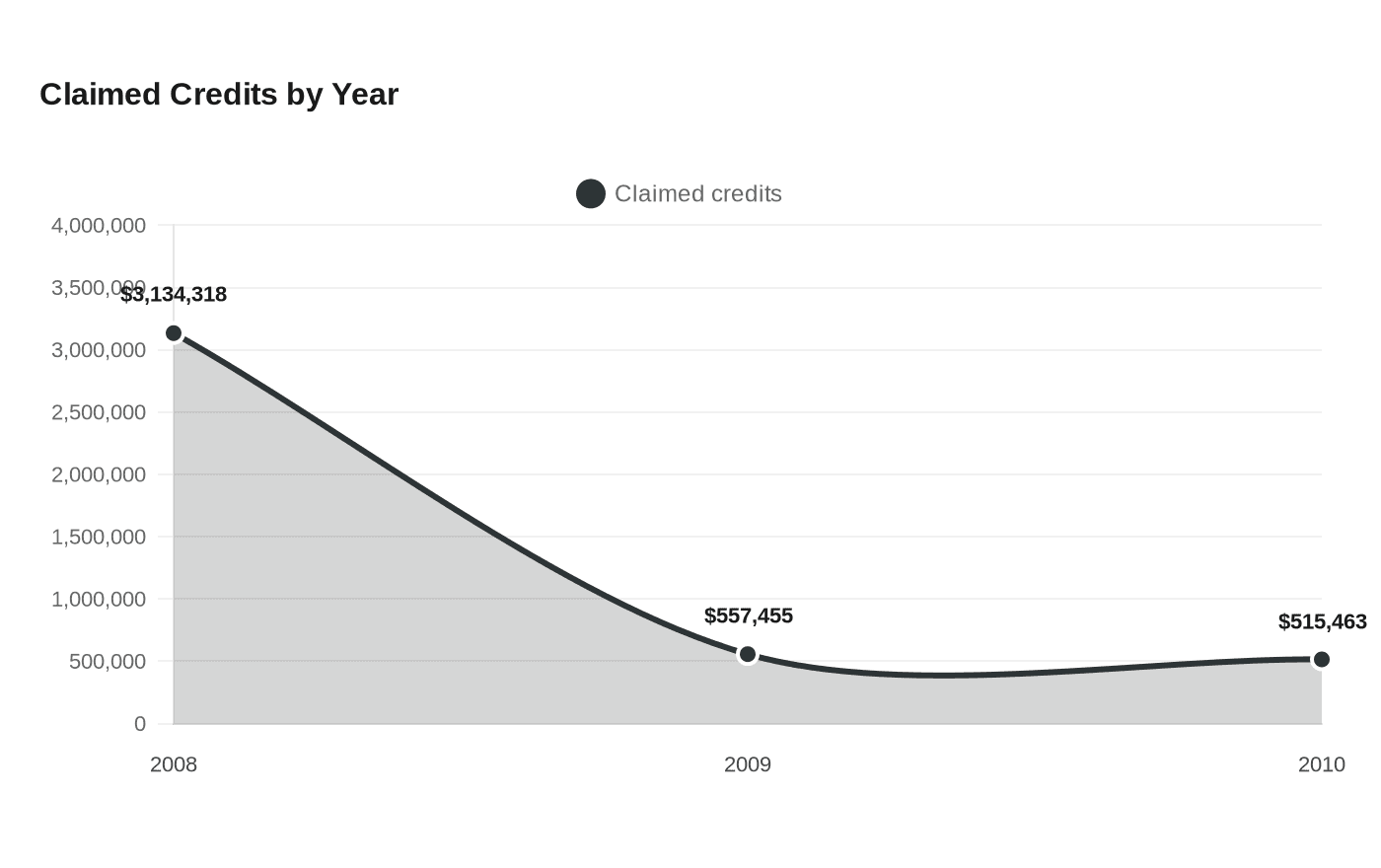

In T.C. Memo. 2026-50, filed June 16, 2026, the court addressed consolidated docket Nos. 13382-17, 13385-17 and 13387-17 involving Adrian D. Smith and Nancy W. Smith, Carlisle G. Gill and Wendy S. Gill, and Robert J. Forest and Susan N. Gaspari-Forest. The credits flowed through from Adrian Smith + Gordon Gill Architecture, LLP, to the partners’ joint returns and were carried forward and later carried back through amended returns. The IRS had disallowed credits tied to Atrium City Tower, Kingdom Tower, Masdar HQ, Atrium City Masterplan, Plot 14 and Plot R2, with reported claimed credits of $3,134,318 for 2008, $557,455 for 2009 and $515,463 for 2010.

The court’s remaining questions were narrow but consequential: whether the research was funded under section 41(d)(4)(H) and whether the 2008 compensation paid to Smith, Gill and Forest was reasonable under section 174(e). Before trial, the IRS filed a motion for summary judgment on October 1, 2024, and the case was set for a special trial session beginning March 10, 2025, in Chicago. The IRS ultimately conceded that AS+GG’s claimed business components met the four-part test for qualified research, so the real fight became who bore the risk and who owned the research rights.

That is where the operational lesson lands for KPMG tax controversy, credits and incentives, and industry teams serving architecture, engineering, software and product-design clients. Commentary on the case points to supertall towers, zero-carbon and low-energy concepts, wind studies, solar orientation analysis, and structural and environmental performance issues, but the court still focused on whether the contracts and reimbursement structure supported the claim. The agreements also included choice-of-law provisions tied to Dubai, Saudi Arabia and the United Kingdom, making this one of the first Tax Court cases to test how local or foreign governing law affects the funding analysis.

KPMG linked the ruling to Meyer, Borgman & Johnson, Inc. v. Commissioner, the 2024 Eighth Circuit decision that strengthened the government’s position on the funding exclusion in professional-services settings. For clients and the teams advising them, the practical response is clear: tighten research-rights language, document reimbursement and ownership terms project by project, and build contemporaneous substantiation that can survive audit when only part of a portfolio qualifies.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)