KPMG sees selective private equity market still funding AI and energy deals

AI data centers and energy networks are still drawing capital, even as global PE deal counts and fundraising hit multi-year lows.

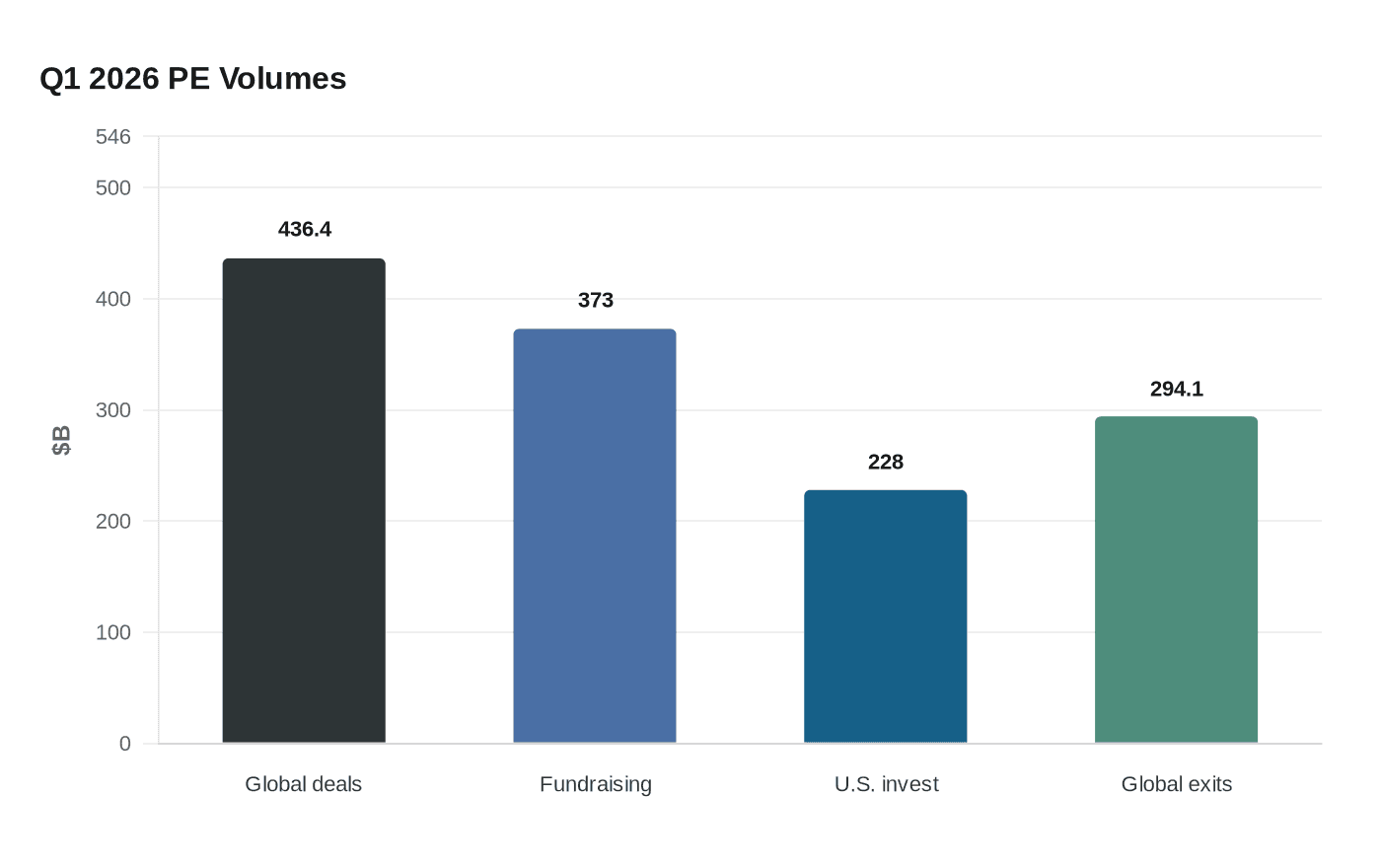

Private equity is still writing big checks, but it is doing it with a much sharper lens. KPMG said global PE deal value reached $436.4 billion across 4,168 deals in the first quarter of 2026, even as the rolling 12-month deal count slipped to 19,682, the lowest since Q1 2021, and fundraising fell to $373 billion, its weakest level since 2017.

That combination matters for KPMG deal teams because it points to a market that is not frozen, only selective. Capital is still moving into large transactions tied to AI infrastructure, the energy transition, transportation and business services, especially where data-center power demand, digitization and logistics complexity create a clear investment case. In practice, that means more demand for diligence, valuation, tax structuring and post-deal integration work in a narrower set of sectors rather than across the whole market.

Tilman Ost, who heads KPMG’s Private Equity practice in EMA and Germany, put the trend plainly: “infrastructure investments related to AI, digitalization, and the energy transition are developing particularly dynamically, driven in part by rising power demand from AI applications and data centers.” Ost has more than 17 years of exclusive private equity experience, and his team’s read of the market reflects where sponsor attention is going now, toward power, resilience and operating scale.

The U.S. picture was similar. KPMG said private equity investment in the United States totaled $228 billion in Q1 2026, while the rolling transaction count fell to 8,536, a five-year low. The quarter’s biggest deals underscored how concentrated the market has become: the $41 billion take-private of AES by Global Infrastructure Partners and EQT, the $9.2 billion secondary buyout of InPost led by Advent International and FedEx, and the $7.5 billion buyout of EGYM led by Affinity Partners. KPMG also said investors were increasingly using add-on acquisitions as a value-creation tool.

The exit side was slower. Aggregate global exit value reached $294.1 billion in Q1 2026, but exit volumes declined further and IPO activity stayed muted. KPMG said investor sentiment entering the quarter was cautiously optimistic, helped by dry powder, better exit conditions and a stabilizing macro backdrop, although geopolitical conflict in the Middle East briefly dampened deal activity.

For KPMG’s own professionals, the clearest signal sits inside the sector mix. A separate KPMG and Oxford Economics M&A Outlook for Germany found that 76% of surveyed M&A leaders already use AI in due diligence and 83% expect AI to improve post-merger integration. Business services, including IT services and audit, tax and legal consulting, also remain attractive to investors. That is where the work is likely to land next: not in broad-market exuberance, but in the teams that can price power, map data-center demand and turn a selective deal market into execution.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)