KPMG survey finds AI reshaping finance, boosting judgment and assurance

KPMG’s latest finance AI survey says the real prize is better judgment, not just automation. Clients are already demanding evidence, assurance, and faster decisions.

AI in finance has crossed a threshold that matters inside every KPMG service line: the question is no longer whether the technology works, but what it should be trusted to do. The clearest message from KPMG’s latest global survey is that finance teams are moving AI out of the back office and into decision support, where the stakes are higher and the need for human sign-off is harder to avoid.

AI is moving from automation to judgment support

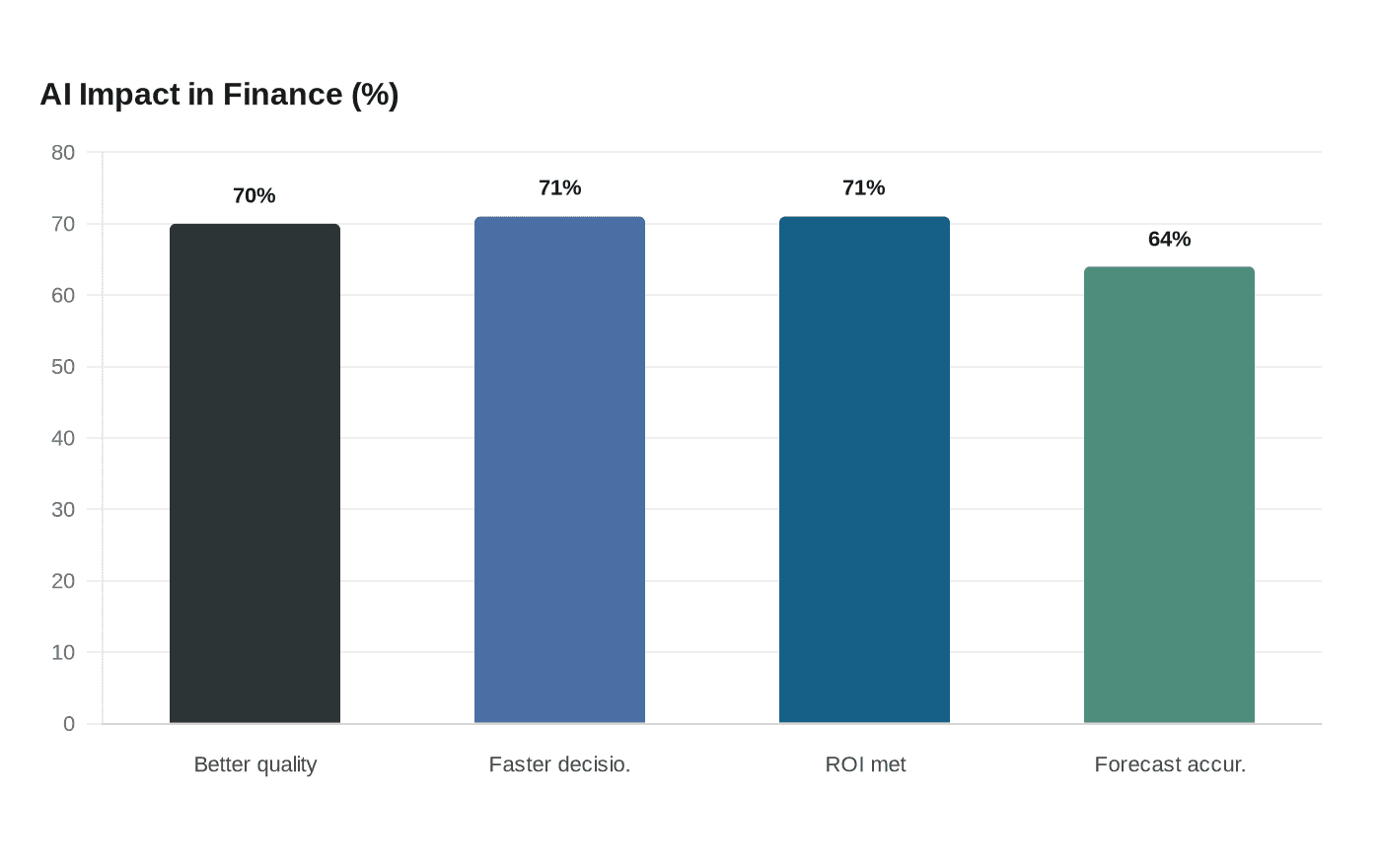

The shift shows up in the numbers. KPMG says active AI use across finance has climbed from 30% in 2024 to 75% in 2026, and 71% of leaders now say AI is meeting or exceeding ROI expectations. In the same survey, 70% of organizations reported better decision-making quality, 71% said decision-making got faster, and 64% saw improved forecast accuracy. That is a big change from the early AI pitch, which was mostly about shaving minutes off repetitive tasks.

For KPMG consultants, auditors, and advisors, the practical implication is straightforward: the client conversation is moving upstream. Finance leaders are not just asking whether AI can close a reconciliation or draft a variance explanation. They are asking whether it can improve the quality of the decision that follows, and whether the result can survive review, challenge, and audit.

The survey signals where clients are already spending

The underlying 2026 Global AI in Finance report was fielded in March 2026 and surveyed 1,013 senior finance leaders across 20 countries and 13 sectors. It covered organizations with annual revenues of at least US$250 million, and US$500 million in the United States. That makes the findings more than a technology snapshot. They reflect how large finance functions, including many KPMG clients, are redesigning work in real time.

KPMG says the next 18 months will bring even more change in the United States, where 93% of companies are expected to be deploying or scaling AI in finance. Half of U.S. companies in the survey are already planning to orchestrate or develop multi-agent AI systems across finance workflows. That matters because multi-agent setups are not just single-use tools. They imply coordinated systems that touch planning, reporting, controls, and decision support at the same time.

Assurance readiness is becoming the differentiator

The most important signal for audit and assurance teams is KPMG’s finding that assurance readiness now separates the winners from the laggards. KPMG defines assurance readiness as the ability to produce AI-related audit evidence efficiently and without disruption. Organizations that are ready on that front report three to six times higher rates of error reduction than those without that readiness.

That changes what good finance AI implementation looks like. The firms getting the most value are not merely deploying models faster. They are building the documentation, evidence trails, and control structures that allow human reviewers to trust the output. In practice, that means audit teams will spend less time arguing about whether AI is allowed and more time evaluating whether the evidence is sufficient, reproducible, and aligned with the business judgment being made.

The report also says data quality is both the most-cited barrier and the biggest opportunity in AI finance adoption. That is consistent with what clients are already discovering: even strong models produce weak answers if the underlying data is fragmented, inconsistent, or incomplete. For KPMG teams, that puts a premium on data governance, control design, and review standards that are tight enough for audit but flexible enough for change.

Agentic AI is starting to matter in finance workflows

KPMG’s data suggests that agentic AI is where the biggest performance gains are starting to show up. Organizations deploying agentic AI showed about a 32-point advantage across key finance metrics, and nearly 40 points on forecast accuracy and ROI. Those are large gaps, and they suggest that the most advanced users are not just automating tasks but rethinking how work flows through finance teams.

The story for KPMG practitioners is not that AI replaces finance judgment. It is that it changes where judgment gets applied. Routine classifications, drafting, and first-pass analysis can move faster, but escalation points still need humans. A CPA can speed up transaction review, anomaly detection, forecasting scenarios, and draft commentary. Human sign-off still matters where there is a material estimate, a control exception, a complex accounting policy question, or a client issue that could affect assurance conclusions.

That distinction should reshape how teams work with clients now. Instead of treating AI as a productivity layer on top of existing processes, KPMG teams will need to redesign review checkpoints, clarify who owns final decisions, and define what evidence is required before a machine-assisted recommendation is accepted.

What this means for KPMG workflow design

The report points to three operational changes that will matter inside KPMG engagements.

- Evidence standards need to be built in from the start. If assurance readiness depends on efficient audit evidence, teams should not wait until close or sign-off to ask for logs, prompts, exception trails, or model outputs.

- Review layers need to be explicit. AI can accelerate preparation, but judgment quality still depends on who checks the output, when escalation happens, and what gets documented.

- Client conversations need to shift from capability to accountability. The more useful question is no longer whether AI can generate an answer. It is whether the answer is reliable enough for a controller, a tax leader, or an engagement partner to stand behind it.

That is where KPMG’s audit, tax, and advisory teams have a chance to work together. Audit brings discipline around controls and evidence. Tax can help build workflow intelligence around recurring judgments and exception handling. Advisory can help leadership teams design operating models that keep AI useful without making governance an afterthought.

Talent and training are still lagging behind the technology

The report also shows that most organizations are upskilling existing teams, but only 28% are rethinking the types of talent they need. That gap matters for KPMG because the workflow change is bigger than training people to use a tool. Teams will need staff who can evaluate model behavior, challenge outputs, and connect technical performance to financial judgment.

For professionals on the partnership track, that raises a familiar Big 4 tension: faster delivery can look like progress until review quality slips. The firms that get this right will be the ones that use AI to raise judgment quality, not just throughput. The firms that miss it will end up with more output and less confidence in what they are signing.

KPMG’s own framing captures the core of the shift: the conversation about AI in finance has changed. The firms that win will be the ones that can pair technology with governance, evidence, and professional judgment, turning AI from a productivity tool into a decision engine that finance leaders can actually trust.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip