KPMG’s Diane Swonk warns Iran-war supply shocks may echo 1970s

Swonk says the Hormuz shutdown disrupted 20M+ barrels a day, and IEA reserves “only cover about 20 days.” Expect sharper client stress tests and choppier staffing.

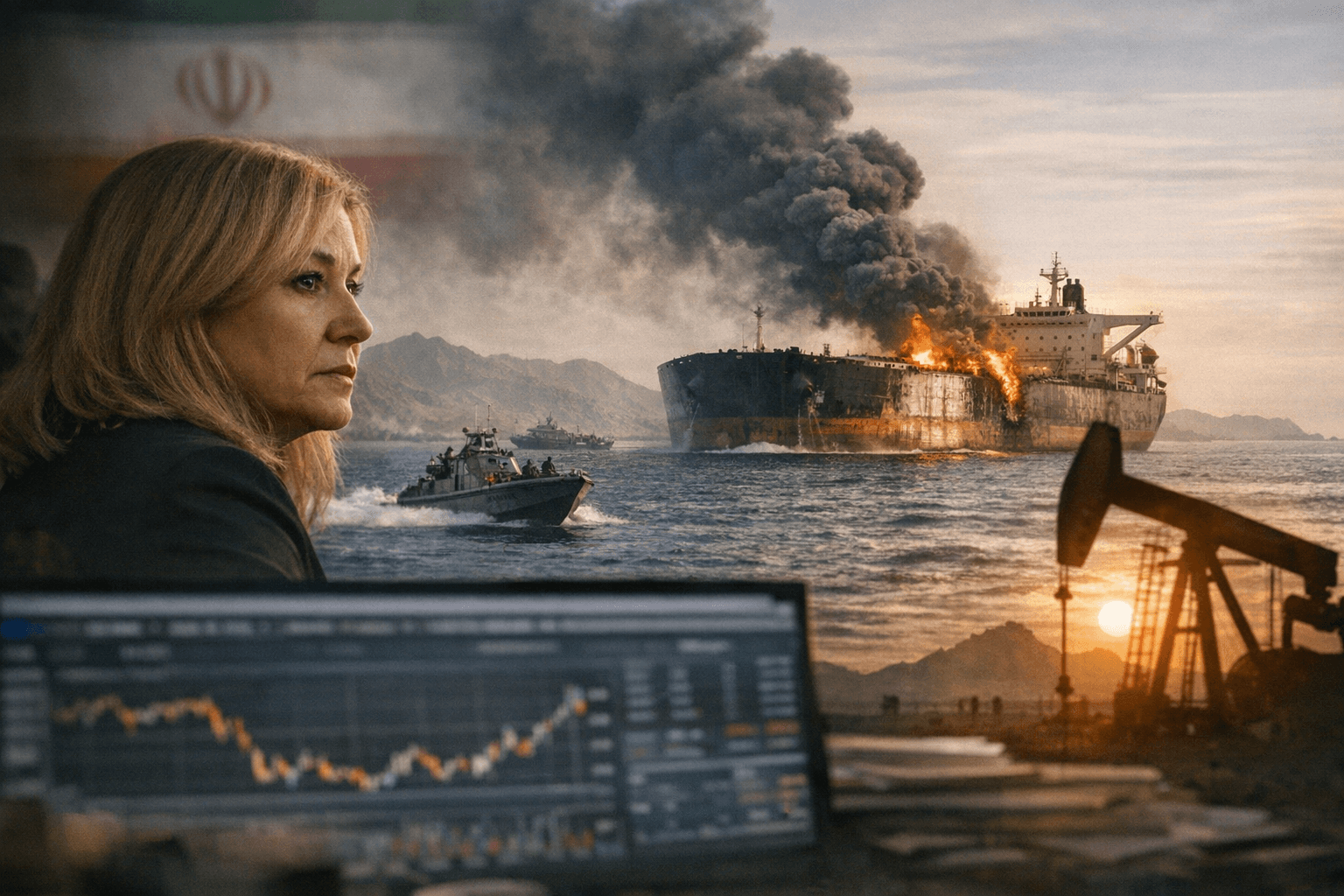

A Strait of Hormuz shutdown that KPMG says disrupted “more than 20 million barrels per day,” about “one-fifth of global supply,” is now the data point showing up behind closed doors in client budget calls and internal resource meetings. Diane C. Swonk, KPMG U.S. chief economist, put that disruption at the center of the firm’s April 8 Economic Compass commentary, framing the Iran-war supply shock as something that “rhymes” with the 1970s oil shocks, with a nod to Jackson Browne’s 1977 “Running on Empty.”

For KPMG teams, the immediate impact is not theoretical: this is the kind of macro shock that changes what clients ask for on Monday morning and what gets deprioritized by Friday. Federal Reserve Bank of Dallas researchers tied the Strait closure to the outbreak of military conflict with Iran on Feb. 28, 2026, helping explain why CFOs have moved from “watching” energy risk to demanding fresh scenarios that assume prolonged disruption.

Swonk’s first indicator is the scale and speed of the energy shock itself. She compares the Hormuz disruption, “more than 20 million barrels per day,” with roughly 4.5 million barrels per day during the 1973 shock. In practice, that pushes more clients toward rapid margin-defense work: price escalation language, customer renegotiations, fuel and freight pass-through assumptions, and fast-turn forecasting updates that land in advisory workstreams and, increasingly, audit planning conversations when operating forecasts drive impairment screens.

The second indicator is the lack of shock absorbers. Swonk argues strategic reserves coordinated by the International Energy Agency “only cover about 20 days of supply,” and that releases move slowly through refineries with limited capacity. That short runway tends to translate into more near-term “keep the business running” asks: liquidity and working-capital stress tests, inventory strategies, supplier substitution, and supply-chain resilience projects that can crowd out discretionary transformation work that is harder to justify when leadership teams feel exposed.

The third indicator is KPMG’s near-term growth path. In the PDF version, the narrative said real GDP growth was expected to rise 1.9% in Q1 2026 and then slow to 1.3% in Q2 2026. For KPMG practices, slower growth paired with supply-side inflation risk usually means a split pipeline: tighter approval for net-new spend, but faster approvals for cost takeout, restructuring readiness, carve-out planning, and risk work that boards will not defer. Swonk has also warned publicly that if stagflation takes hold, “the only clear way out is a deep recession,” a framing that tends to push clients to demand downside cases with harsher assumptions and shorter decision timelines.

Internally, expect more volatility in travel and staffing. The Compass calls the situation “more than an oil shock,” citing shipping constraints and warning disruptions could take “weeks or even months” to normalize, with some infrastructure damage taking “years” to repair. That duration risk often shows up as stop-start client mobilizations, sudden pauses on nonessential workshops, and heavier utilization pressure on teams tied to discretionary growth programs, while restructuring, supply-chain, accounting advisory, and audit specialists see rising demand for estimate and going-concern work.

What to watch: utilization softness in discretionary advisory work as CFOs re-cut budgets mid-quarter; rising requests for downside scenarios tied to freight and fuel assumptions; increased audit effort around impairments, credit losses, and going-concern documentation as forecasts get reworked; more carve-out and restructuring readiness work as boards ask for contingency plans instead of longer-horizon roadmaps.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)