Walmart outperforms rivals as scale and ads boost profits

Walmart is funding its low-price shield with scale, ads and memberships. For stores, that means tighter inventory, faster fulfillment and more pressure to convert shoppers into recurring revenue.

Walmart’s price fight is no longer being won only at the register. The company is using its size, Walmart+ memberships and a fast-growing advertising business to cushion tariff pressure before it reaches shelf prices, and that pushes more responsibility onto stores to keep inventory tight, substitutions clean and digital orders moving.

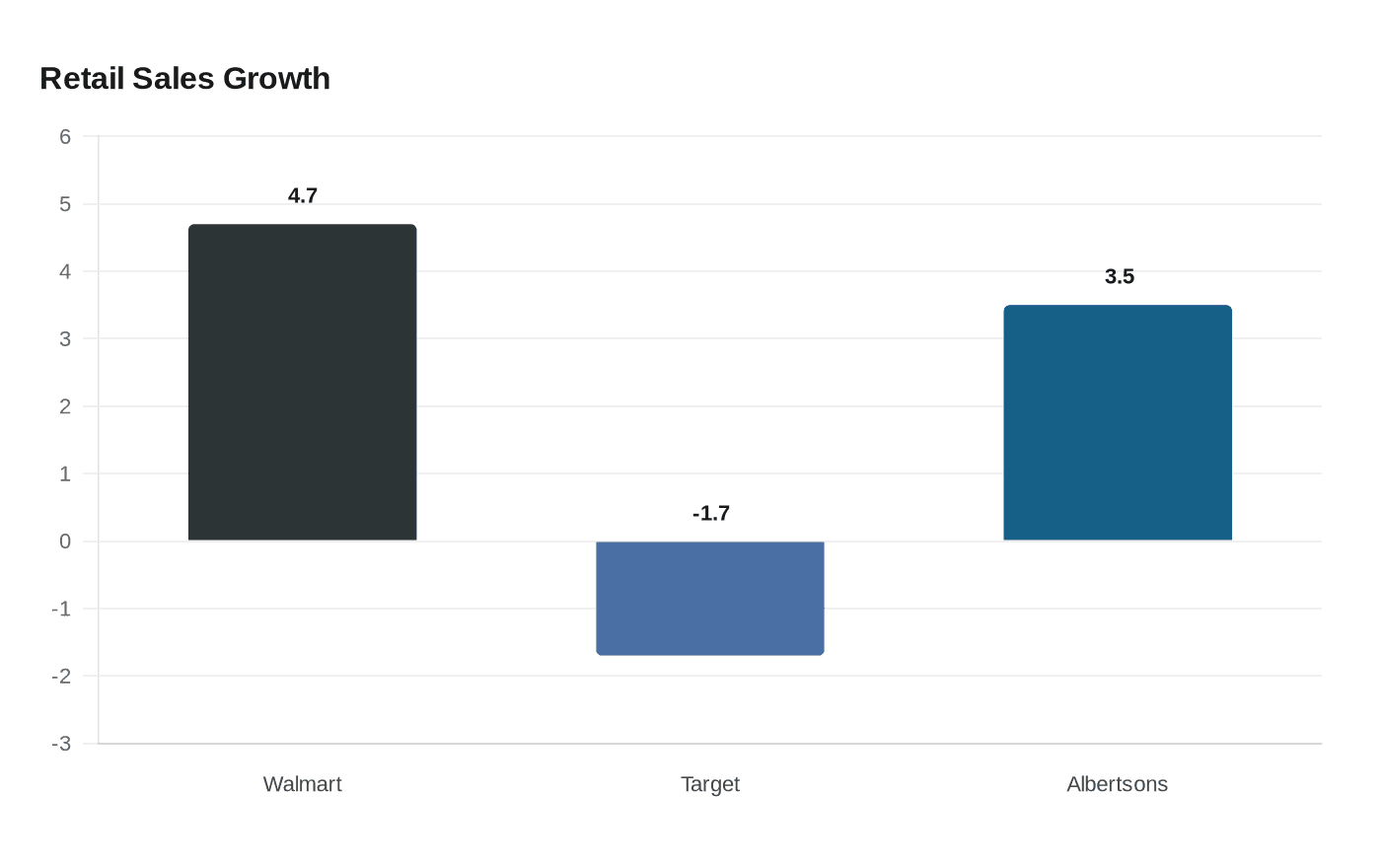

The numbers show why. Walmart said revenue reached $713.2 billion in the fiscal year ended Jan. 31, up 4.7% from a year earlier. In the same period, Target’s sales fell 1.7%, Kroger was roughly flat and Albertsons rose about 3.5%, a sign that Walmart kept widening its edge even as inflation and tariffs kept retailers under strain.

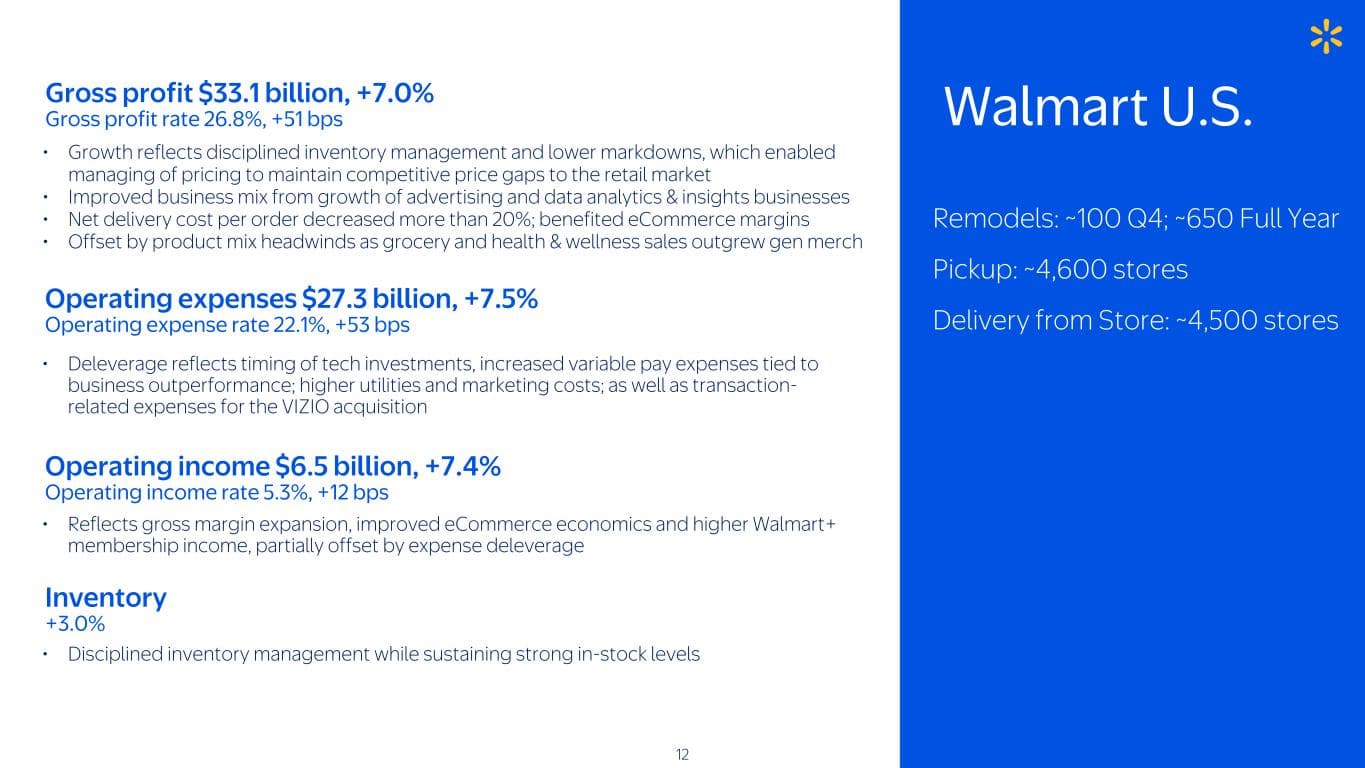

What is changing inside the business is just as important as the sales headline. Walmart said eCommerce sales hit $150.4 billion, advertising revenue came to nearly $6.4 billion and membership-fee revenue was about $2 billion. The company also said its global advertising business grew 46% in fiscal 2026, including VIZIO, while membership fee revenue rose 15.1% globally. Those streams are no longer side businesses. Based on Morningstar data, they accounted for an estimated 27% of operating profit last fiscal year, up from 9% in 2021.

That matters on the sales floor because more of Walmart’s low-price promise is now financed by business that happens outside the traditional checkout lane. When advertising and memberships carry more weight, managers have stronger incentives to drive recurring Walmart+ sign-ups, use retail media to support featured items and push inventory toward products that can support both traffic and margin. That also means less tolerance for empty shelves, slower substitutions or poorly timed replenishment.

Walmart’s own filings point to that operational pressure. Global inventory rose 4.3% in fiscal 2026, or 2.6% in constant currency, while the company said stronger inventory management and better eCommerce economics helped operating income grow faster than sales. Reported operating income rose 1.6% for the full year, and adjusted operating income increased 5.4%, even as the company kept leaning on its price gap to pull in shoppers.

Executives signaled the same priorities at an investor meeting last April: keep prices low, manage inventory well and control costs in a tariff-heavy environment. That is the operating rule associates feel most directly. If shoppers are squeezed, Walmart can win traffic, but stores absorb the work, from picking and packing to shelf execution and in-stock discipline. The company’s new $30 billion share repurchase authorization and higher annual dividend show investors are being rewarded too, but the real test remains whether stores can keep the low-price machine moving without letting service levels slip.

Know something we missed? Have a correction or additional information?

Submit a Tip