e.l.f. Beauty Denies Securities Fraud Claims, Cites Public Inventory Disclosures

A securities fraud case against e.l.f. Beauty narrows to one TV interview where CEO Tarang Amin called demand "strong" as inventory was quietly swelling.

When a beauty brand tells investors demand is booming while stockrooms are quietly filling up, the fallout rarely stays contained to Wall Street. Shoppers feel it in the sudden markdowns, the clearance endcaps, and the slow erosion of trust in a brand that once seemed unstoppable. That is the dynamic at the center of a securities fraud class action now moving into its next phase against e.l.f. Beauty, Inc., and it carries consequences that extend well beyond the courtroom.

On April 3, the Oakland, California-based company filed its formal answer to the surviving claims, denying all allegations and raising affirmative defenses, including a "truth on the market" argument. That defense contends that the inventory metrics plaintiffs claim were concealed were, in fact, visible in public disclosures all along, and that the lawsuit amounts to hindsight re-interpretation of data that was always accessible to the market.

The case has been narrowing since March 2025, when Rottman v. E.l.f. Beauty, Inc. et al accused the company, CEO Tarang Amin, and CFO Mandy Fields of reporting "inflated revenue, profits, and inventory over several quarters." The suit drew on a November 2024 report by short seller Muddy Waters Research, which alleged e.l.f. had materially overstated revenue across multiple quarters and had obscured weakening sales behind explanations tied to sourcing-practice changes. On February 6, 2025, the company's own fiscal third-quarter results confirmed softer-than-expected consumption trends and slower product launches, sending the stock lower and adding weight to the plaintiffs' theory. By May 2025, Boston Retirement System and Metropolitan Employee Benefit System of Nashville had been appointed lead plaintiffs, with Labaton Keller Sucharow as lead counsel.

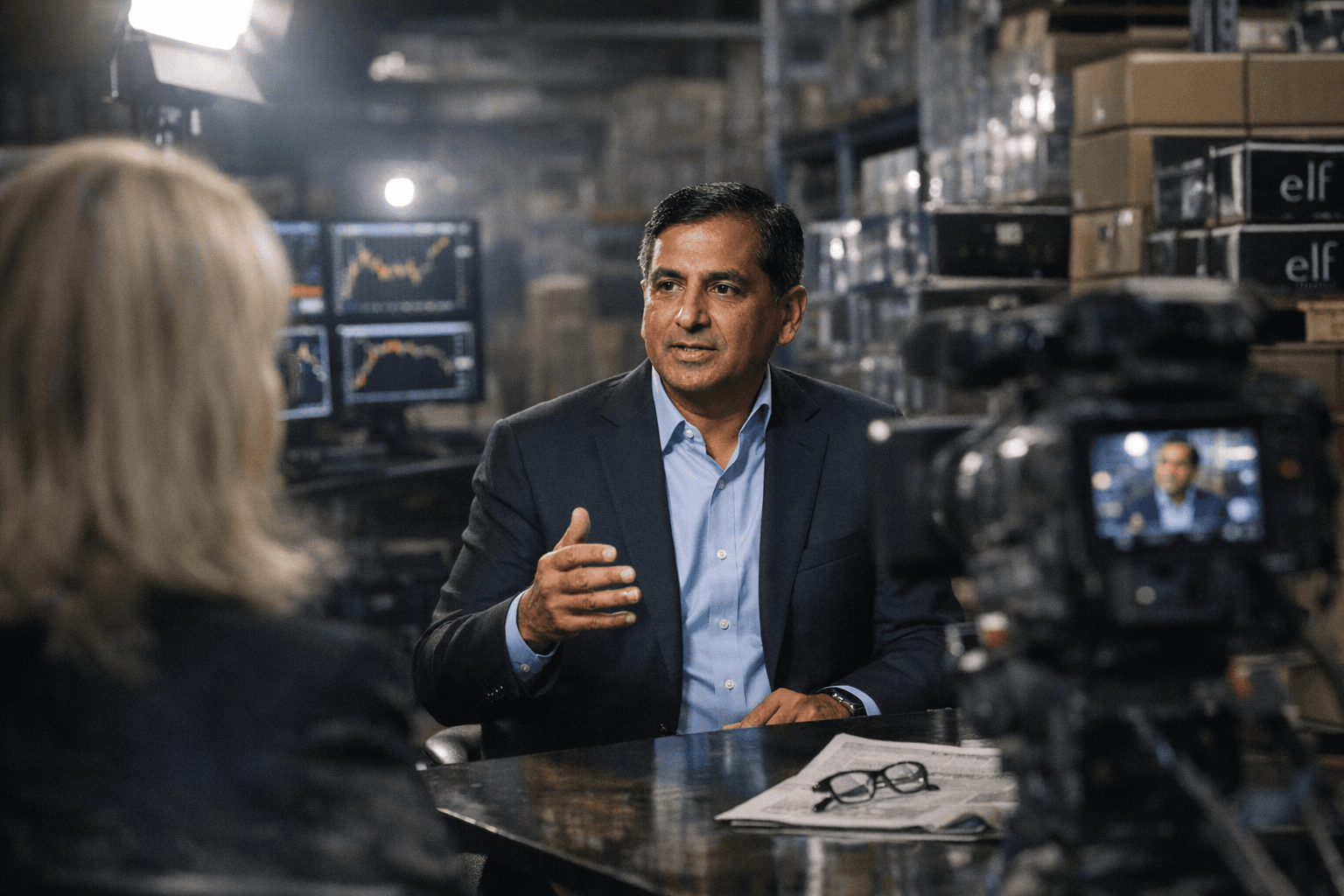

In a February 4, 2026 order, Judge Eumi K. Lee of the U.S. District Court for the Northern District of California pared the case significantly. She dismissed all claims against Fields, finding the complaint failed to establish the requisite intent to deceive on the CFO's part, and she disposed of broad statements about company strength as non-actionable puffery. What survived was a precise, narrow theory: statements Amin made during a November 2024 television interview, in which he characterized inventory as building to meet "strong demand" and described e.l.f.'s relationship with Ulta Beauty as "strong." The court found those specific remarks could plausibly mislead investors if, as the complaint alleges, Amin was already attending monthly internal forecast meetings where declining sales trends and excess inventory were tracked.

e.l.f.'s answer, filed eight weeks after that ruling, rejects those surviving claims entirely. Beyond the "truth on the market" position, the company contests whether plaintiffs can demonstrate material misstatements, prove loss causation, or establish that investors actually relied on Amin's televised remarks.

The pattern alleged here, inflated demand signals feeding overproduction, is one the beauty industry knows well. Excess inventory triggers discounting that undercuts brand equity, strands unsold product, and puts consumers on a price-swing carousel that makes intentional shopping nearly impossible. For investors and shoppers alike, the critical question the case will now force into the record is whether the disclosures e.l.f. points to as exculpatory were ever specific, timely, or prominent enough to count. That answer will arrive through discovery, and the standard it sets could reshape how beauty companies are expected to communicate inventory risk going forward.

Know something we missed? Have a correction or additional information?

Submit a Tip