Luxury brands narrow store footprints, focus on alpha cities

Dior and Gucci are cutting weaker doors and betting big on a tighter circle of alpha cities, where sales-per-square-foot still justifies the rent.

Luxury is getting ruthless about square footage. Dior and Gucci are not chasing more doors; they are chasing better math, closing weaker locations and pouring money into fewer, higher-impact stores in alpha cities where tourist traffic, clienteling and sales-per-square-foot can still make the rent look sane.

That shift is not a store-design story. It is a profitability reset. McKinsey said the luxury industry faced a sharp slowdown in 2025, and for the first time since 2016, excluding 2020, value creation was expected to come in below the prior year. Savills said global luxury store openings fell in 2025 to their lowest level since 2020, a clear sign that brands are choosing quality of presence over scale of network instead of spraying themselves across every semi-decent postcode.

The money is concentrating where the footfall is strongest. Savills said global alpha cities and destination cities regained importance as international travel recovered, with Shanghai, Beijing and Tokyo taking the top three spots for new luxury store openings among alpha cities in 2024. Hong Kong’s Tsim Sha Tsui stayed a core luxury draw, proof that the old tourist circuits still matter when the product is expensive enough and the crowd is international enough.

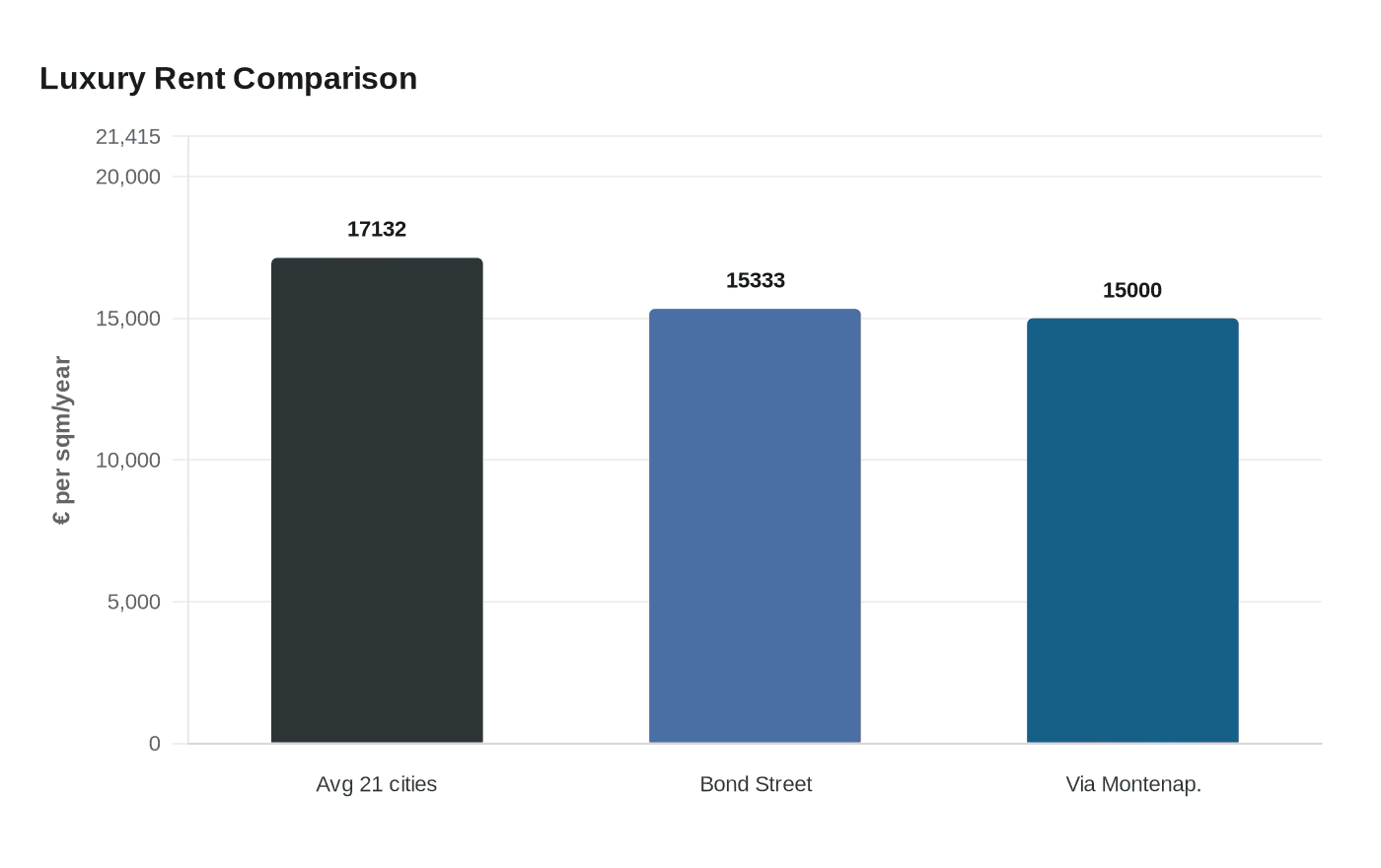

The rent numbers explain why only the strongest locations survive. Across the 21 destinations Savills tracked in 2024, luxury retail rents averaged €17,132 per square metre per year. London’s Bond Street sat at the top of Europe at €15,333 per square metre, just ahead of Milan’s Via Monte Napoleone at €15,000. Those are not ordinary storefronts. They are giant, glossy advertisements with tills attached, and that is exactly how AlixPartners says LVMH, Kering and Chanel are treating them, by increasing capital investment in stores and real estate even in a slowdown.

The U.S. market is still growing, but it is concentrating fast. JLL said newly opened luxury retail square footage in the U.S. rose 65.1% in the first half of 2025 versus the same period in 2024, and 59% of new luxury store openings from July 2024 to July 2025 landed in street retail rather than malls. New York led the pack, with Madison Avenue, Fifth Avenue and SoHo the most active districts. North America accounted for 27% of total new luxury openings in 2025, the first time it has led since tracking began in 2016.

The message for every market outside those hubs is blunt. Luxury is not abandoning physical retail. It is tightening it, defending the addresses that still pull tourists, top clients and global attention, and letting the weaker doors fade out of the picture.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?