LVMH, Kering and Richemont Drive 13% Rise in European Luxury Store Openings

Europe's prime luxury streets saw 96 store openings in 2025, up 13% year-on-year, with LVMH named the most active retailer and Paris accounting for more than a fifth of all new sites.

The traditional relationship between luxury sales performance and physical expansion is breaking down. Sales growth has slowed, yet store openings climbed to 96 in 2025; consumers have become more selective, yet prime rents keep rising. That is the defining tension in Cushman & Wakefield's latest European Luxury Retail report, and it tells you something important about how the biggest houses are choosing to fight back.

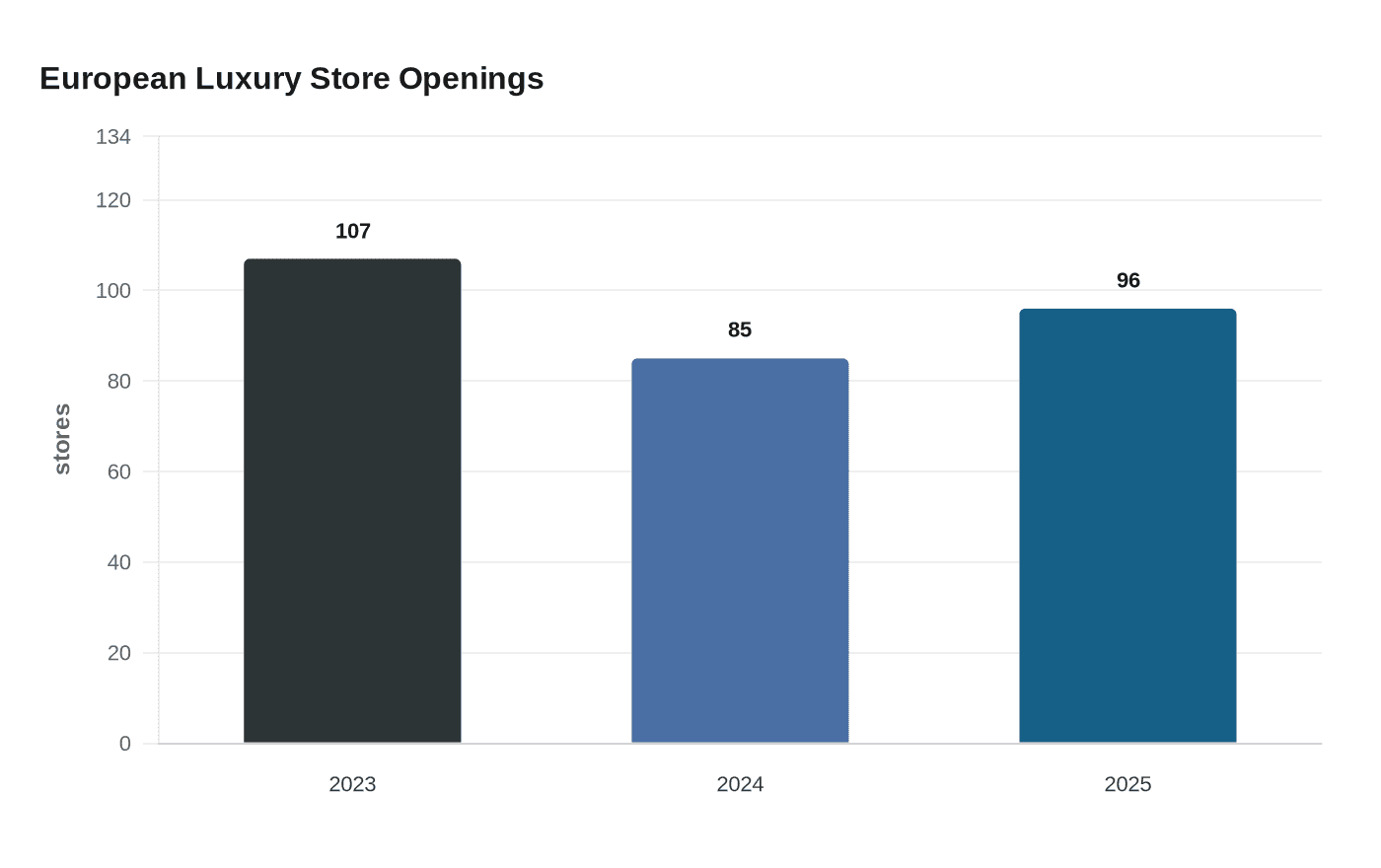

The 13% rise in store openings versus 2024 was driven by brands owned by LVMH, Kering and Richemont, which together accounted for almost one third of all openings. The region saw 96 openings in 2025, up from the prior year but below the 107 seen in 2023. Those new doors spread across 20 benchmark streets, 16 cities and 12 European countries.

LVMH, owner of brands such as Louis Vuitton and Dior, was the most active retailer, followed by Kering, whose store openings included two each for its Saint Laurent and Bottega Veneta brands. Richemont, owner of Cartier and Montblanc, saw fewer openings after a couple of years of strong activity, the report noted. The group's pullback stands out given that its peers were still pressing forward.

The expansion is happening in spite of, not because of, a rosy earnings picture. In January, LVMH reported poor Christmas holiday sales and indicated conditions would not improve significantly in 2026. In Q4 2025, three of the group's five divisions fell short of expectations, prompting CEO Bernard Arnault to tell investors the group would limit expenditures. Gucci, under Kering, experienced a 10% drop in sales during the same period, though this marked the smallest decline in two years. The decision to keep cutting ribbons while flagging tighter spending signals that physical real estate is now treated as a long-term brand asset rather than a short-term sales bet.

Paris, which saw a drop in store openings in 2024 as the city hosted the Olympic Games, made up a little more than a fifth of the new outlets in 2025. The French capital also produced one of the more surprising micro-trends in the data. "We've seen six luxury fragrance stores open this year, all in Paris actually," said Sally Bruer, head of EMEA retail research at Cushman & Wakefield, noting that fragrances have been particularly popular due to their lower price point compared with jewellery and watches.

The fashion and accessories segment remained the largest driver of new openings in 2025, with 48 stores from 40 different brands, representing half of all activity and an uplift of 17% on 2024. The jewellery and watches category saw 28 new boutiques in 2025, flat on the previous year but nearly 30% higher than in 2023.

The real-estate dynamics underpinning all of this are severe. Eight of the 20 profiled streets recorded zero percent vacancy in 2025, with a further six streets below 5% in terms of availability. By the end of 2025, rents on luxury streets were 7% above 2018 levels, reaching or maintaining record highs in several markets. In 2025 alone, rents on luxury streets rose by 3.5%, while non-luxury high streets recorded 3.3% growth.

Duncan Gilliard, head of central London retail at Cushman & Wakefield, said inquiries had not cooled since the start of the year. If deal volumes do drop, he added, it will be "because of the record low availability of locations rather than necessarily demand."

Robert Travers, head of EMEA retail at Cushman & Wakefield, put it plainly: "Luxury brands increasingly see their stores as cultural statements, a physical manifestation of identity, craft and heritage. That's why we're seeing larger, more immersive flagships and multilevel spaces that bring brand universes to life."

The market continues to reflect both consolidation at the top and growing diversification. While the three major conglomerate groups held roughly a third of new openings, 70% of new stores were launched by 57 other brands and groups, highlighting the competitive intensity of European luxury retail. Swedish fashion brand Toteme, for example, opened three stores on the key streets in 2025, the kind of fast-growing contemporary name now competing directly for the same scarce real estate as the heritage houses. That scramble for space, more than any single quarterly earnings call, is what shapes the next chapter of luxury retail in Europe.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?