UNEP FI issues textile finance guide to assess circularity risks

UNEP FI’s new textile guide turns circularity into bank due diligence, rewarding measurable reuse and exposing virgin-heavy risk.

From brand story to balance-sheet test

UNEP FI has pushed textile circularity out of the mood board and into the credit committee. Its new sectoral guidelines give commercial banks and development finance institutions a three-step way to identify, classify and assess the circularity of textile clients, which means lending decisions can now be tied to measurable operating reality rather than polished sustainability language.

Why the pressure has sharpened

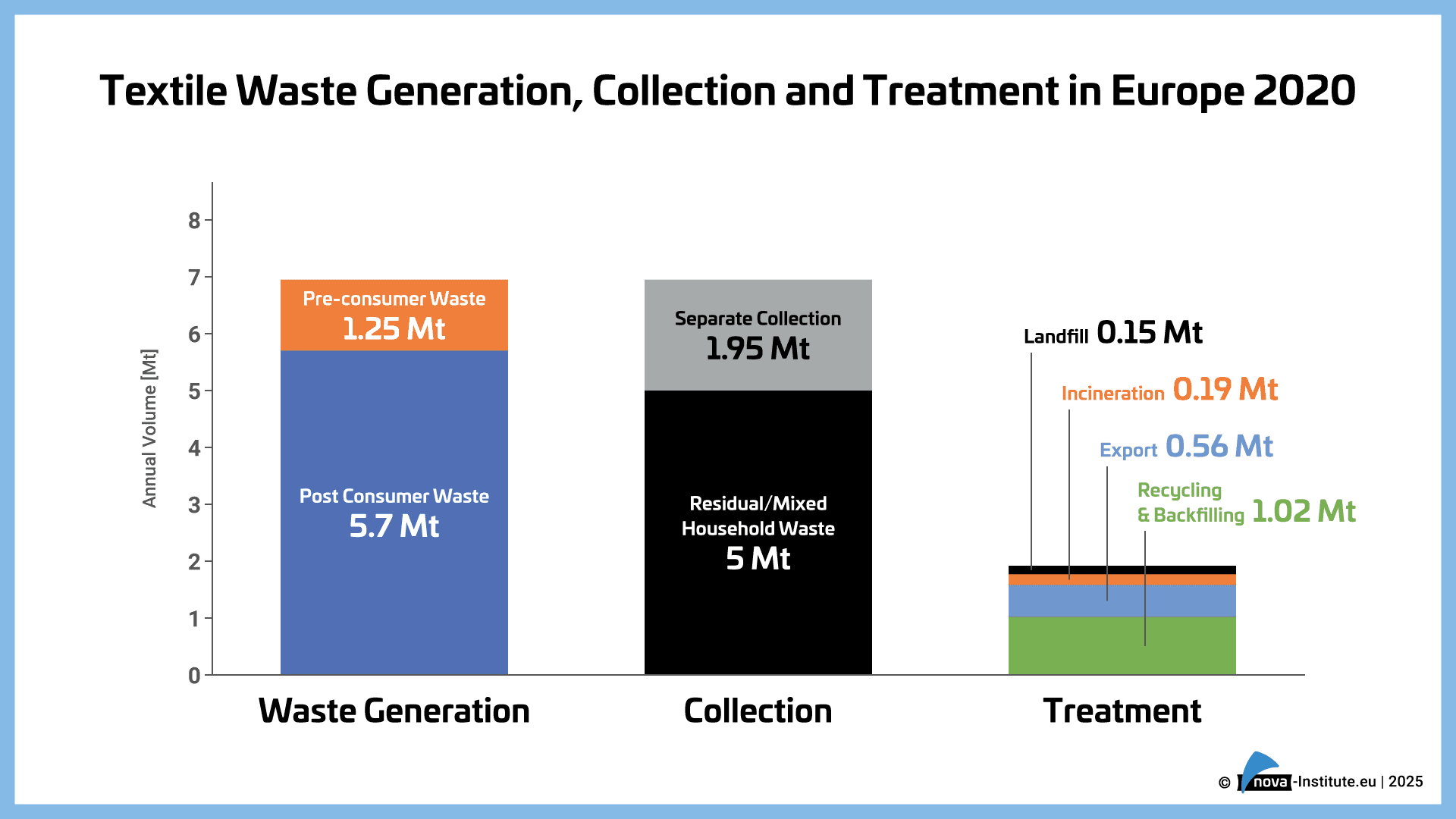

The scale is the reason this matters. UNEP FI says the textile sector consumes about 3.25 billion tonnes of materials every year, and more than 99% still comes from virgin sources. Textile Exchange’s latest market data shows why finance is being asked to look harder: global fiber production rose from 125 million tonnes in 2023 to 132 million tonnes in 2024, has more than doubled since 2000, and could reach about 169 million tonnes by 2030 if business continues as usual.

That is not a subtle sustainability backdrop. It is an expanding resource bill, and it is still dominated by fossil-heavy synthetics. Polyester accounted for 59% of global fiber output in 2024, 88% of that polyester was fossil-based, and recycled polyester remained largely dependent on plastic bottles rather than textile waste. In other words, the industry’s most common raw material story is still linear, even when it is dressed up as recycled.

How the guide works in a bank

The point of the new UNEP FI textile guidance is not simply to label a business as good or bad. It is designed for the people who actually decide where money goes, including client advisors, relationship managers, risk teams and sustainability teams, and it can be used in transaction screening, portfolio exposure mapping, sustainability-linked financing products and engagement on transition plans. UNEP FI also says the framework helps institutions determine which activities are circular and where circularity criteria are not yet met, opening the door to targeted client engagement rather than blanket exclusion.

That distinction matters because circularity is no longer a niche design talking point. It is becoming a credit question: can a textile client show credible circular activity, or is it still leaning on virgin inputs, throwaway cycles and waste at the back end? The guide’s structure suggests that banks will increasingly need to map where a client sits on that spectrum before they decide what to finance, what to price up and what to challenge.

The line between fundable and fragile

UNEP FI’s earlier circular economy work already sketched the kind of behavior that looks financeable. In 2024, it urged banks to embed circularity into internal policies and processes, engage clients in transition, redirect financial flows toward circular solutions and advocate for mainstreaming circularity. It also pointed to practical products such as green loans for businesses committed to circular principles, finance for product-as-a-service models, loans for recycled-input manufacturing and support for closed-loop supply chains.

That is the real sorting mechanism emerging here. Measurable circular practices, especially reuse, repair, recycled inputs and closed loops, start to look like strengths when a bank is assessing resilience and long-term value. Business models that remain dependent on virgin material throughput, especially in a sector where polyester still dominates and fossil-based inputs still rule, begin to look more exposed to regulatory, supply-chain and resource-risk pressure. That is an editorial judgment, but it is grounded in the numbers UNEP FI and Textile Exchange are now putting on the table.

This is part of a longer banking pivot

The new textile guide is not arriving in isolation. It follows UNEP FI’s July 2024 circular-economy series for the 300-plus signatories to the Principles for Responsible Banking, a series designed to move banks from target-setting to delivery. Eric Usher said that guidance would help banks foster circular solutions to address climate change, pollution and nature loss, while building a more sustainable, resilient and inclusive economy.

That earlier series also framed circular economy as an answer to the old linear “take-make-waste” model, and said banks should integrate circular principles into lending and investment decisions, internal policies, client engagement and financial flows. It sits on top of UNEP FI’s 2020 Financing Circularity report, which recommended that financial institutions manage linear and circular risks and opportunities, integrate circularity into ESG criteria, set resource-efficiency targets and re-orient loans and investments toward more sustainable technologies and business models.

What happens next

UNEP FI is inviting banks and DFIs from all regions to join a pilot programme throughout 2026 to test the textile guidelines, share implementation feedback and help refine the methodology and tools. That makes this guide less like a manifesto and more like a live underwriting experiment, with the textile sector serving as one of the clearest places to see whether circularity can finally move from brand promise to bankable proof.

The fashion industry has spent years treating circularity as a capsule collection idea, polished, photogenic and safely aspirational. This framework gives it a harder life in finance, where the question is no longer whether a brand sounds sustainable, but whether its material flow, business model and transition plan can survive scrutiny when capital starts asking for evidence.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?