Cintas Posts Record Margins as Q3 Revenue Climbs to $2.84 Billion

Cintas hit a 51% gross margin in Q3, an all-time high, as revenue climbed 8.9% to $2.84B and a $5.5B UniFirst deal reshapes workwear supply.

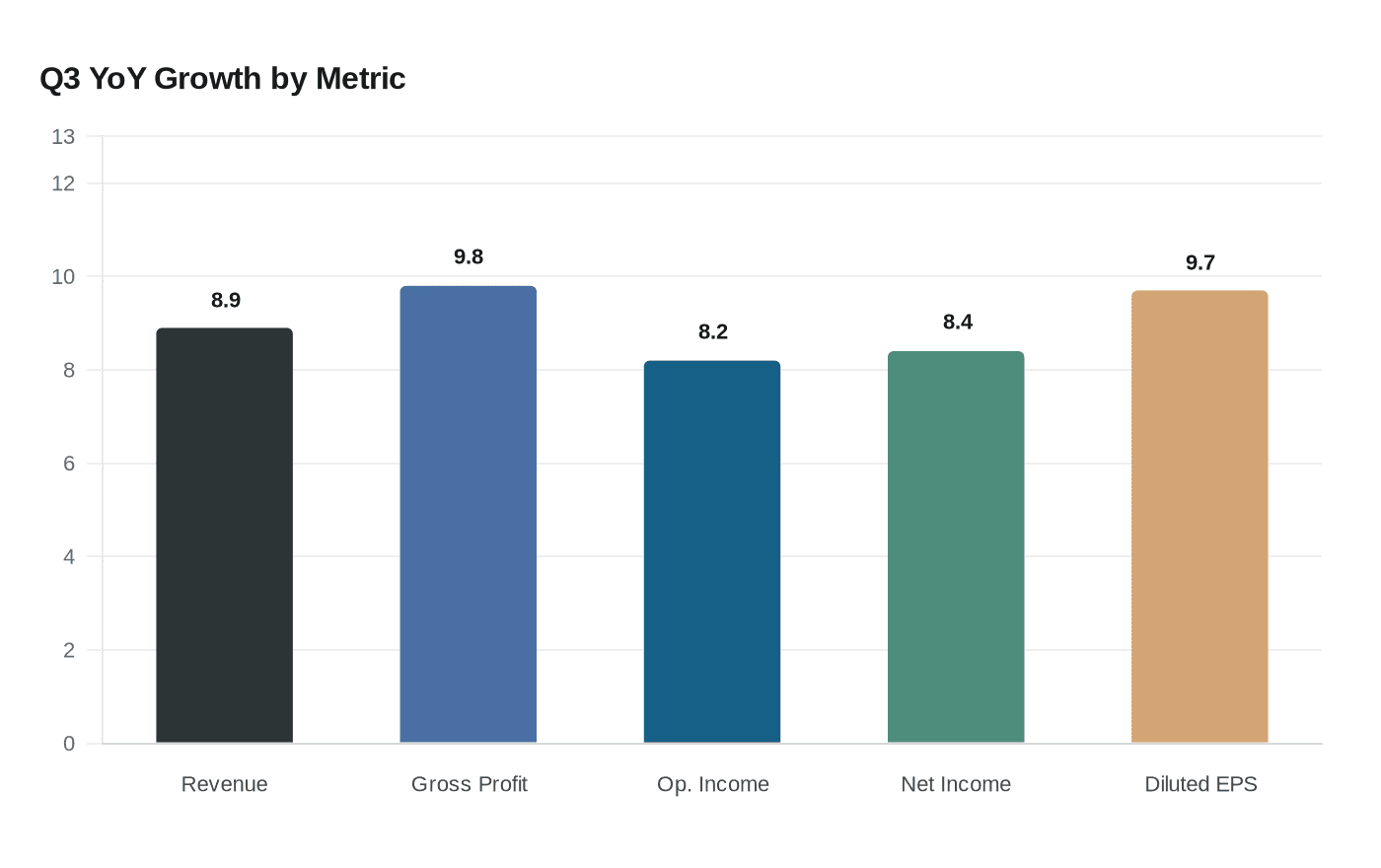

Cintas's gross margin hit 51.0% in the fiscal third quarter ended February 28, the highest in the company's history, as total revenue climbed 8.9% year over year to $2.84 billion and a pending $5.5 billion acquisition of rival UniFirst promises to redraw the map of American workwear supply.

President and CEO Todd Schneider said the company delivered "another successful quarter," crediting the resilience of its value proposition and continued investment for future growth. Organic revenue, stripped of acquisition effects and foreign currency movements, grew 8.2%. Gross profit rose 9.8% to $1.45 billion, with the 51.0% consolidated gross margin arriving 40 basis points above the prior-year quarter's 50.6%.

All three of Cintas's route-based businesses posted record or all-time high gross margins during the quarter, a performance management attributed to targeted investment in technology, capacity and talent. Operating income reached $659.9 million, up 8.2% from $609.9 million a year earlier. Excluding a one-time gain recorded in the prior-year period, operating margin would have expanded 40 basis points year over year. Net income came in at $502.5 million, up 8.4% from $463.5 million, and diluted earnings per share rose 9.7% to $1.24 from $1.13 in last year's third quarter.

Cintas raised its full fiscal 2026 guidance on the back of the strong quarter. Revenue is now projected at $11.21 billion to $11.24 billion, with adjusted diluted EPS expected between $4.86 and $4.90. The updated outlook excludes non-recurring transaction costs tied to the planned UniFirst acquisition, which Cintas estimates will shave $0.03 to $0.04 from full-year earnings per share; the company plans to begin breaking out those costs separately starting in the fiscal fourth quarter.

The UniFirst deal, announced March 10, 2026, at an approximate value of $5.5 billion, is the most consequential development in uniform services in years. Subject to shareholder and regulatory approvals, management expects the transaction to close in the second half of 2026, with pro forma leverage settling near 1.5x debt to EBITDA. The combination would create a dominant force in workwear procurement and route-based distribution, with management flagging operational synergies, expanded service capabilities and plans to integrate UniFirst team partners once the deal is complete.

The strategic stakes extend well beyond Cintas's own balance sheet. This consolidation concentrates pricing power and service coverage in the uniform and workwear sector at a moment when corporate uniform programs are already contending with supply chain complexity and rising input costs. For procurement managers who source through either company today, the merged entity is likely to reshape contract terms and negotiating dynamics across the industry.

Cintas returned $1.45 billion to shareholders through dividends and share repurchases in the first nine months of fiscal 2026, including a $180.0 million quarterly dividend paid March 13, 2026.

Know something we missed? Have a correction or additional information?

Submit a Tip