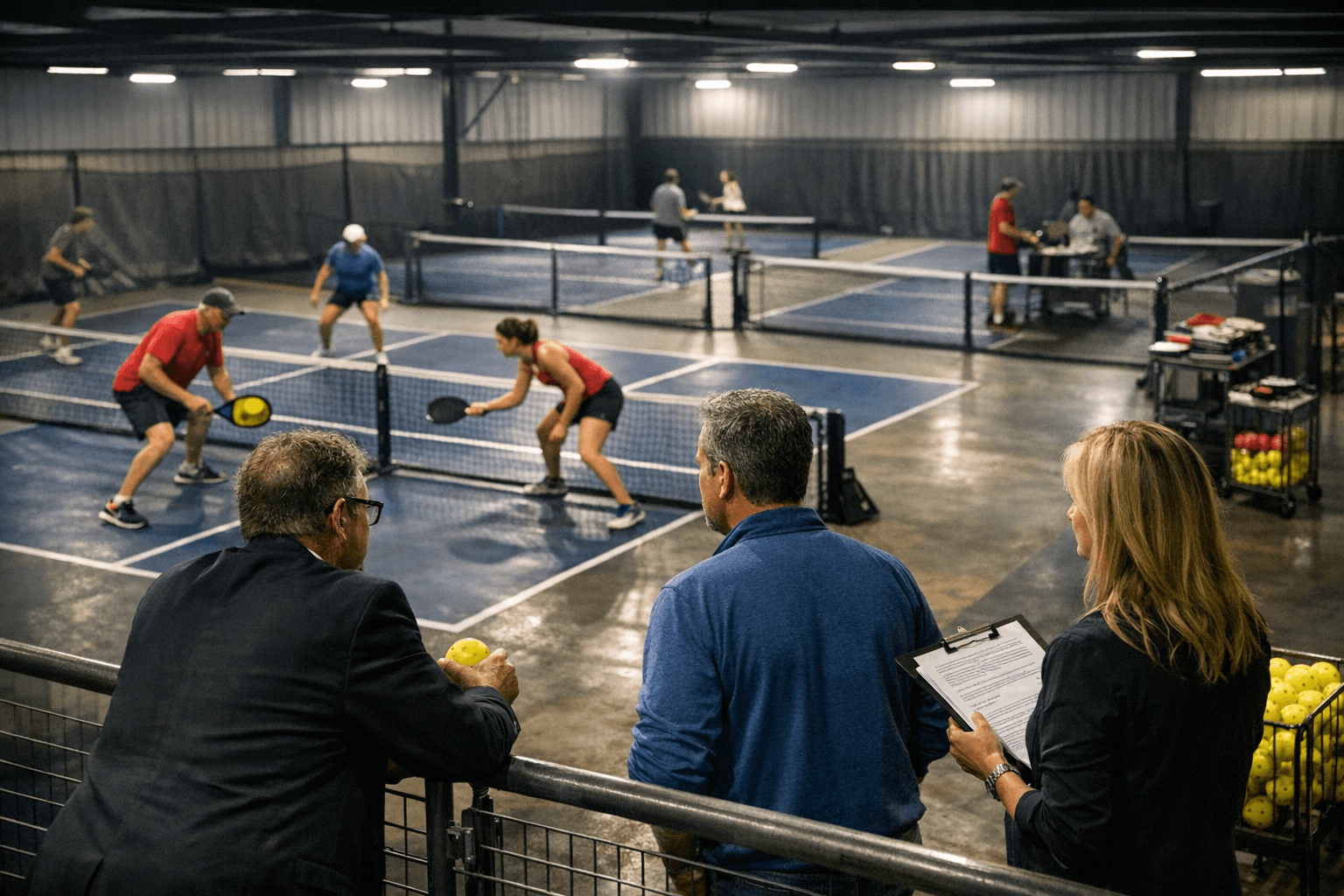

Indoor Pickleball Club Boom Draws Investors, Franchises, and Facility Operators

A potential shakeout looms as investors, franchises, and facility operators flood the indoor pickleball club market, according to a new industry analysis.

The indoor pickleball club industry has attracted a striking convergence of capital, franchise systems, and independent facility operators over the past several years, and a new analysis suggests the sector may be approaching a critical inflection point. Alex E. Weaver's March 18, 2026 deep-dive for The Dink, drawing on data and reporting from sources including David Johnson's Business of Pickleball newsletter, maps the full landscape of who built these clubs, who funded them, and what comes next.

The Money Behind the Courts

The indoor club boom didn't happen organically. Investors saw a sport with explosive participation growth and moved to capitalize, pouring capital into dedicated facilities that could monetize court time, memberships, leagues, and food-and-beverage operations simultaneously. Weaver's analysis traces how that financial interest shaped the physical footprint of indoor pickleball across the country, funding everything from boutique single-location clubs to multi-unit franchise rollouts.

What makes this investment wave notable is the range of players involved. It isn't just private equity or venture capital operating at a distance; facility operators, franchise developers, and individual entrepreneurs all became part of the same expansion story, each bringing different models and different assumptions about how indoor pickleball would scale.

Franchises Enter the Picture

Franchise systems represent one of the most consequential developments in the indoor club space. By packaging a replicable club model, complete with branding, operational playbooks, and court configurations, franchise operators made it easier for investors without deep pickleball backgrounds to enter the market. This accelerated growth in markets that might otherwise have waited years for a locally-owned facility to materialize.

The franchise angle also introduced a new layer of accountability and standardization. Operators within a franchise system have to meet brand standards, which can raise the floor for customer experience, but they also carry the overhead of franchise fees and royalties, which can compress margins in a business already navigating high real estate and construction costs.

Facility Operators: The Independent Track

Not every club that opened during the boom came with a franchise flag above the door. Independent facility operators, often local entrepreneurs with deep ties to the pickleball community, built and ran their own clubs outside any larger system. These operators move with more flexibility, able to tailor their programming, pricing, and court mix to specific local demand without corporate approval.

The tradeoff is that independent operators tend to have shallower capital reserves and less brand recognition, which can make the early months of operation especially precarious. Weaver's analysis, informed by Johnson's reporting in the Business of Pickleball newsletter, considers how both franchise and independent models stack up as the market matures and competition intensifies.

Signs of a Coming Shakeout

Perhaps the most pointed takeaway from the Weaver analysis is the suggestion that the indoor pickleball facility sector may be heading toward a shakeout. The logic is straightforward: rapid capital inflows and franchise expansion tend to produce oversaturation in specific markets, and when too many courts chase too few players, facilities start competing on price, convenience, and amenities in ways that strain margins and push weaker operators toward closure or consolidation.

A shakeout doesn't mean the sport is in trouble. It's a normal feature of any industry that grows quickly, and pickleball's participation base remains large and enthusiastic. What it does mean is that the facilities that survive will likely be those with stronger unit economics, better locations, more compelling membership products, and operators experienced enough to manage costs through a difficult competitive period.

What Drives Viability in an Indoor Club

Drawing on the industry data aggregated in The Dink's analysis, a few factors emerge as likely differentiators for clubs navigating the next phase:

- Court utilization rates during off-peak hours, not just prime-time weekend slots, matter enormously for covering fixed costs like rent and staffing.

- Membership models that create predictable recurring revenue give operators more financial stability than purely pay-to-play court rental.

- Food-and-beverage and social programming have become competitive battlegrounds, with clubs using lounge spaces and league nights to build community stickiness.

- Locations that anchor to underserved suburban or exurban markets, rather than stacking up in already-saturated urban cores, tend to face less direct competition.

The Role of Industry Intelligence

One of the more interesting aspects of Weaver's piece is its reliance on and citation of David Johnson's Business of Pickleball newsletter as a source of industry data. That a dedicated newsletter covering the business side of pickleball has become a key input for facility-level analysis reflects how rapidly the sport's commercial infrastructure has matured. Investors and operators are no longer navigating this space with anecdote and intuition alone; there is now a layer of specialized journalism and data aggregation that tracks openings, closures, investment rounds, and operating models in real time.

For anyone considering entering the indoor pickleball space, whether as an operator, a franchisee, or a financial backer, that kind of intelligence has become a baseline requirement for making informed decisions.

Where the Market Goes from Here

The boom phase for indoor pickleball clubs is not over, but it is evolving. The era of easy growth, where almost any new facility in almost any market could fill courts and attract members simply by existing, appears to be giving way to something more competitive and more selective. Operators who built their clubs on solid fundamentals and genuine community engagement will be better positioned than those who entered primarily on the thesis that pickleball's rising tide would lift all boats.

Weaver's analysis, rooted in the aggregated data and reporting that The Dink and Business of Pickleball have assembled, makes clear that the indoor club sector is at a genuine crossroads. The investors, franchises, and facility operators who understood from the start that building a sustainable club requires more than courts and a banner will be the ones still standing when the shakeout runs its course.

Know something we missed? Have a correction or additional information?

Submit a Tip