Luckin Coffee’s rapid China expansion faces rising delivery cost pressure

Rising delivery fees are squeezing Luckin’s cheap-doorstep coffee model just as its China store count tops 33,000 and same-store sales turn slightly negative.

Luckin Coffee’s growth machine is still roaring, but the economics behind its bargain coffee are getting harder to ignore. Rising third-party delivery costs are pressuring the ultra-convenient, app-led model that helped the chain flood China with stores, raising a bigger question for the coffee market: how long can Luckin keep pairing low prices with doorstep convenience before margins force a reset?

The company said first-quarter 2026 net revenue rose 35.3% year over year to RMB11,995.5 million, while its global store base reached 33,596 locations. Luckin added 2,548 net new stores in the quarter, including 2,531 in mainland China, with smaller additions in Singapore, Malaysia and the United States. Average monthly transacting customers climbed to 93.1 million, up 25.3% from a year earlier, underscoring how deeply the brand has penetrated China’s daily coffee habit.

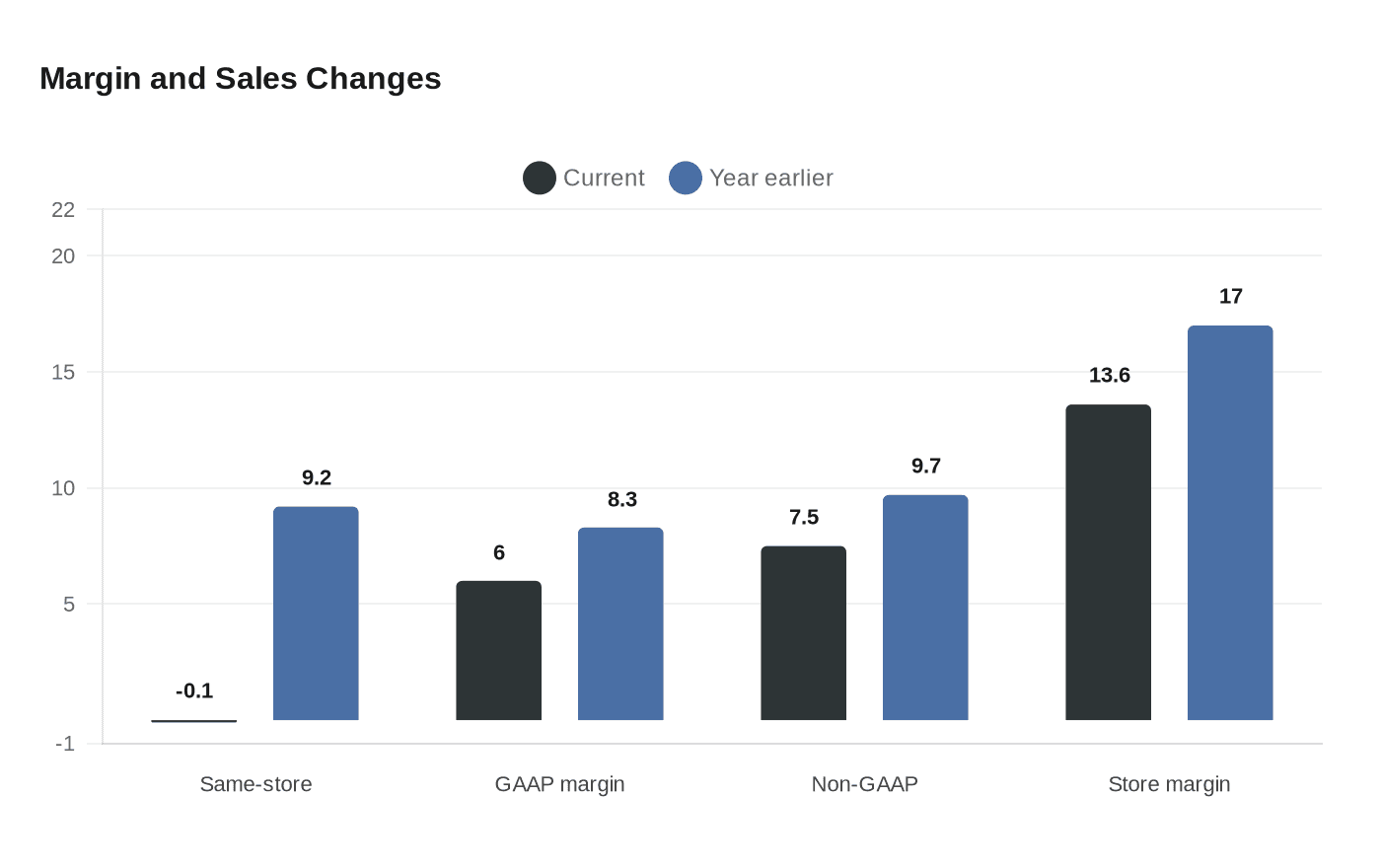

But the profitability picture was softer. Same-store sales growth for self-operated stores slipped to -0.1% from 9.2% a year earlier, a sign that expansion is doing more of the heavy lifting than mature-store demand. GAAP operating margin fell to 6.0% from 8.3%, non-GAAP operating margin declined to 7.5% from 9.7%, and store-level operating margin for self-operated stores dropped to 13.6% from 17.0%. Luckin also said net profit fell 3.6% year over year to about RMB510 million, even as revenue kept rising.

That margin squeeze is drawing attention because delivery is central to the company’s promise. World Coffee Portal said soaring third-party delivery expenses are leaving margins thinner, turning Luckin’s convenience advantage into a test of scale economics. Jinyi Guo, Luckin’s chief executive, said competition among delivery platforms was at its most intense in the second and third quarters of 2025, and the company warned that performance metrics may continue to fluctuate in the short term as the price war cools.

Luckin is already signaling that it may need more than store openings to keep growing. On April 29, 2026, it announced its first share repurchase program, worth up to US$300 million over one year. A day earlier, it had moved into bottled coffee with three products priced between RMB7 and RMB10 in Beijing, sold through selected convenience stores and other channels. After adding 8,708 net new stores in full-year 2025 and finishing that year with 31,048 outlets, Luckin is now facing the harder part of the China coffee race: proving that fast expansion can still pay for itself when delivery gets expensive.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?