Pop Mart's Labubu Supply Chain Boom Gives Way to Operational Strain

Pop Mart scaled Labubu production tenfold in a single year, then watched shares plunge 22% when a Q4 slowdown revealed how fragile viral demand can be.

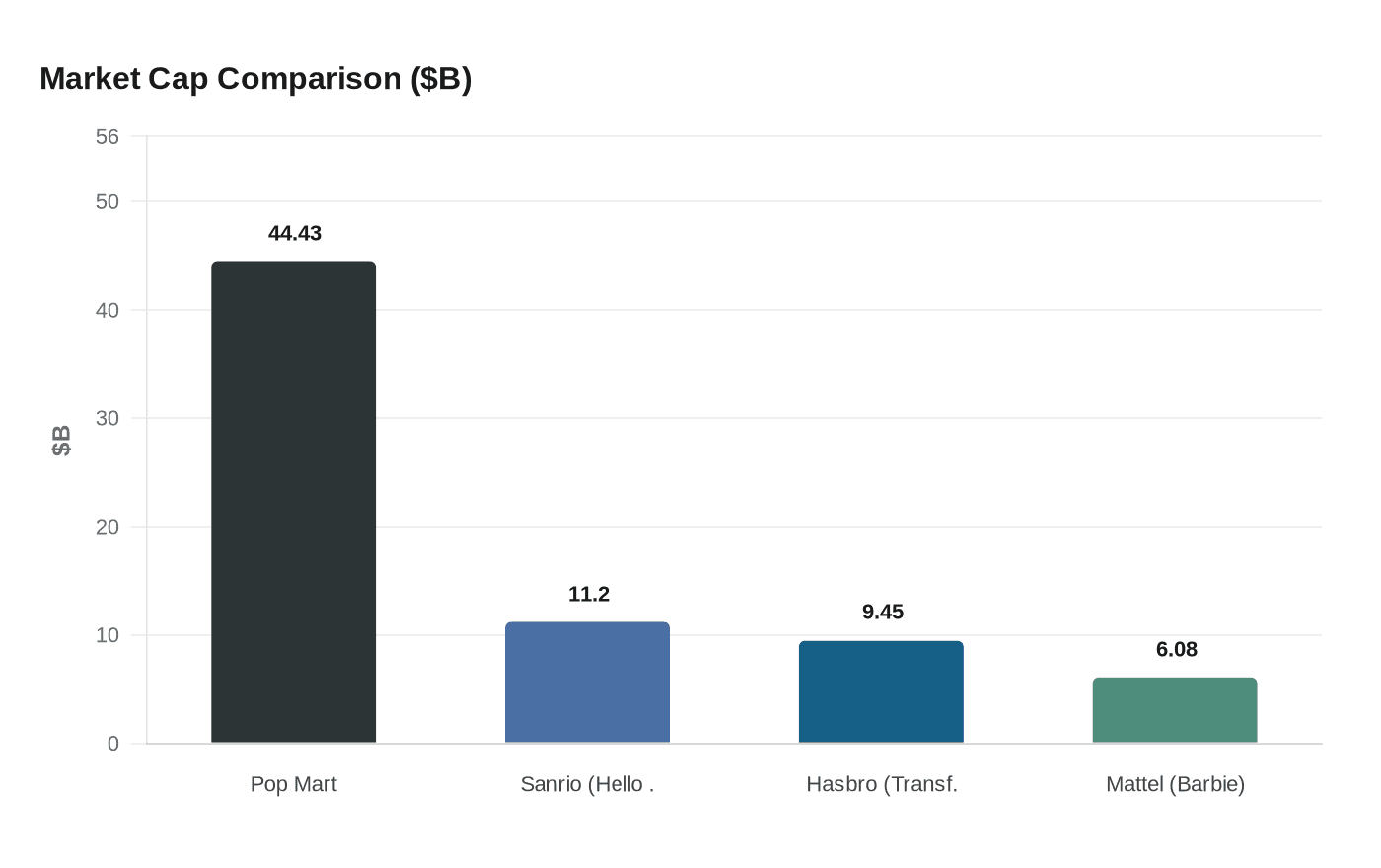

When Pop Mart's valuation hit US$44.43 billion by June 2025, it had eclipsed the combined market caps of the companies behind Transformers (Hasbro at US$9.45 billion), Hello Kitty (Sanrio at US$11.2 billion), and Barbie (Mattel at US$6.08 billion). That single number, surfaced in a Procurement Magazine analysis published March 30, 2026, captures both the extraordinary height of the Labubu craze and the steep distance the company had to fall once momentum stalled.

A Phenomenon Built on Procurement Risk

While the Labubu doll was conceived in 2015 and began its collaboration with Pop Mart in 2019, it did not achieve global phenomenon status until last year. The speed of that ascent left procurement teams with almost no runway. The launch of Labubu 3.0 was so impactful it added US$1.6 billion to the net worth of Pop Mart CEO and founder Wang Ning in a single day. Revenue from The Monsters franchise reached 14.16 billion yuan in 2025, up 365.7% year-on-year, making it the company's first IP franchise to surpass 10 billion yuan in annual revenue. Plush products became Pop Mart's largest category in 2025, with revenue of 18.71 billion yuan, up 560.6%.

The company reported annual revenue of 37.1 billion yuan (US$5.4 billion), a 185% increase from 2024, with net income quadrupling to 12.8 billion yuan (US$1.85 billion). To keep pace, Pop Mart scaled manufacturing to 30 million plush units monthly by late 2025, a tenfold jump from 2024. Rather than operating its own factories, Pop Mart works with local manufacturing partners, and it expanded beyond production limited to China and Vietnam by establishing new facilities in Cambodia, Indonesia, and Mexico.

The Operational Cost of Going Viral

Classic supply chain theory warns that IP-driven demand surges are uniquely hazardous: manufacturers chasing capacity face quality control lapses, volatile lead times, and working capital overextension. Pop Mart lived out that warning at scale. Amid the media frenzy caused by Labubu in the UK, Pop Mart was forced to pause in-store sales due to safety concerns surrounding crowd management and overnight queuing. Globally, the scenes were no less chaotic. Retailers battled long queues and chaotic "frenzies" in-store, where physical altercations broke out and secondary market resale prices skyrocketed.

This is following 2025's issues of meeting customer demand, with retailers witnessing long lines and resale frenzies as delivery times for the dolls increased. Pop Mart had to limit stock online and in its stores. The blind-box format, which gives each drop its speculative charge, made forecasting nearly impossible. Random assortment releases amplify buying surges; influencer-driven spikes on TikTok can materialize and dissipate within days, leaving procurement teams perpetually one step behind.

One of the most difficult balances to strike has been between scarcity, which drives demand, exclusivity, and hype, and meeting consumers' expectations for availability. Artificial scarcity such as limited product drops has proven to be a sound commercial model, but only if it doesn't tip over into customer frustration.

Resale Markets: From Premium to Plunge

The secondary market reflected every tension in the supply chain in real time. During peak demand, resellers commanded steep markups on sought-after figures, and Pop Mart's share price mirrored the frenzy, rising over 200% year-to-date at its high point. By the time manufacturing caught up, the dynamics had already reversed. Shares in Pop Mart dropped 40% from their August peak, reflecting concerns about the brand's long-term mainstream appeal. The second-hand market, which saw significant activity during the summer of 2025, began experiencing declining resale prices.

That sequence, from scarcity-driven premium to oversupply-driven correction, is the textbook outcome when a company scales production aggressively to meet a demand curve that is itself peaking. For collectors who had timed entries into the secondary market, the shift from speculative frenzy to declining valuations was a direct consequence of supply chain decisions made months earlier.

The Q4 Stumble and Investor Fallout

When Pop Mart released its full-year 2025 results on March 25, 2026, the headline growth figures were extraordinary by any conventional standard. The company's revenue came in at 37.1 billion yuan, just shy of LSEG estimates of 38 billion yuan, while net income more than quadrupled to 12.8 billion yuan, slightly above the 12.6 billion yuan forecast. Despite those numbers, Pop Mart shares lost more than a fifth of their value in a single session. Hong Kong-listed shares plunged 22.5% to HK$168.30, marking the biggest drop since April 2025.

The most precise public diagnosis came from Jeff Zhang, equity analyst at Morningstar. Zhang noted that "a material slowdown in the fourth quarter [has amplified] investors' concern on the durability of top IP's popularity," and flagged a structural signal embedded in Pop Mart's capital allocation: a pullback in dividend payout ratio to 25% in 2025 from 35% in 2024. For investors reading the tea leaves, the combination of a Q4 deceleration, conservative dividend posture, and ongoing supply chain investment costs converged as a set of compounding risk factors rather than temporary noise.

Diversification as the Long Game

Wang Ning's message to investors was direct. The CEO told investors on the earnings call that "Pop Mart has more than just Labubu." The data behind that claim is real: six major IPs surpassed 2 billion yuan in annual revenue in 2025, and 17 IPs crossed the 100 million yuan mark. The company operated 630 stores globally by year-end, a net increase of 109, along with 2,637 robot stores after adding 165 during the year. It also opened its first physical stores in Germany and Denmark.

Procurement Magazine frames this case as a cautionary example for any company attempting to scale fan-driven IP globally. The supply chain pressures are not incidental; they are structural. Blind-box mechanics, celebrity-driven viral spikes, and regional distribution mismatches make demand visibility genuinely difficult, and no amount of manufacturing expansion fully resolves a forecasting problem that is partly cultural and partly algorithmic.

What Comes Next for Collectors

The chaotic sellouts, overnight queues, and resale premiums that defined 2025 were not design features of the Labubu experience; they were symptoms of a supply chain that hadn't yet caught pace with the cultural moment. New manufacturing capacity across three continents and a monthly output of 30 million plush units suggests the era of true scarcity may be giving way to something more predictable. The long-term health of the collection ultimately hinges on whether Pop Mart can deliver consistent restocks without flooding the market so thoroughly that the Labubu mystique dissolves entirely. That balance between authentic scarcity and genuine availability is precisely what the next chapter of Pop Mart's supply chain story will be judged on.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?