Updated Global Nuclear Market Map Projects $380 Billion Opportunity by 2050

Third Way and Energy for Growth Hub's updated nuclear market map puts a $380B price tag on global opportunity by 2050, with Meta's multigigawatt Oklo/Terrapower deal as Exhibit A.

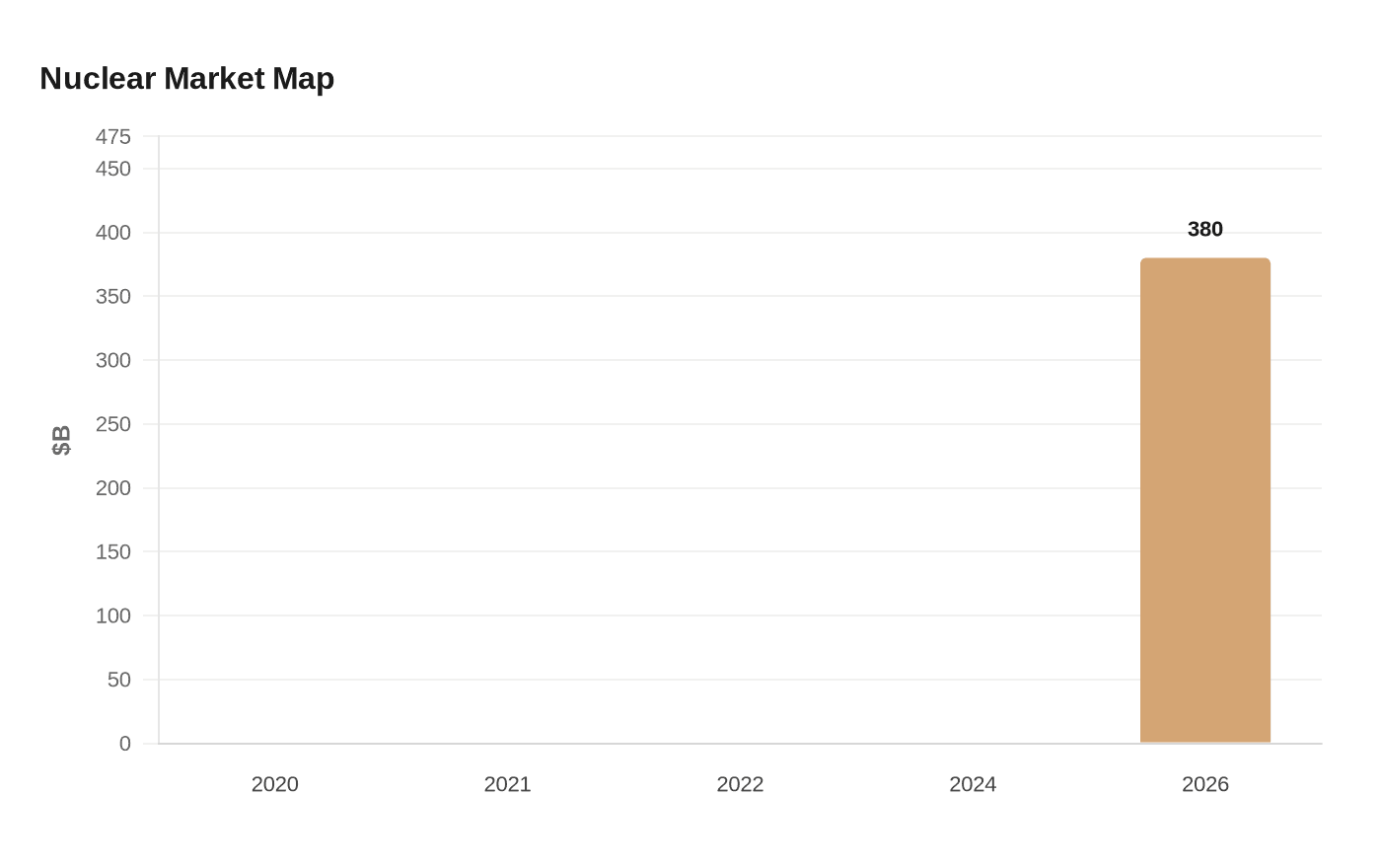

Third Way and the Energy for Growth Hub dropped a striking number on the nuclear industry this week: $380 billion. That is the projected global market opportunity for nuclear power by 2050, according to the 2026 update to their Global Nuclear Market Map, published March 19 and authored by Hamna Tariq and Todd Moss.

The update, which builds on prior iterations from 2020, 2021, 2022, and 2024, does not frame that figure as a distant abstraction. "The global nuclear market has grown substantially in the last two years," the report states, pointing to commercial momentum as evidence. "Multi-unit commercial deals are picking up steam, including Meta's new multigigawatt deal with Oklo and Terrapower and the advancement of AP1000 projects in Poland and Bulgaria." The authors are direct about what those examples mean: "new nuclear deployments are accelerating with billions of dollars at stake."

The map tracks two parallel variables: how ready individual country markets are for advanced nuclear deployment, and how much electricity demand those countries will need to meet through 2050. On readiness, the picture is improving. "More than ever have achieved 'ready' or 'potentially ready' by 2030 status in our metrics," the update notes, with the geographic concentration of new demand lining up favorably: "Most new electricity demand will be in countries that will likely be ready to add new nuclear capacity over the next decade."

That alignment of demand growth and market readiness underpins the bullish $380 billion projection, with emerging markets in Africa and Asia playing a central role. A related Energy for Growth Hub product, its 2025 update to the Global Map of Civil Nuclear Cooperation Agreements, which Marli Kasdan co-authored with Tariq, tracked 20 years of nuclear agreements signed by China, Russia, and the United States and found "a continued push into emerging markets in Africa and Asia" alongside "a growing focus on advanced reactors."

The competitive picture, however, is more complicated for the United States. Despite growing interest in US reactor technology abroad, "China and Russia still lead in critical readiness metrics for supply chain and financing," the report warns. China holds a more dominant position still in raw construction terms: "China also dominates both the US and Russia in new large reactor construction." The cooperation agreements data reinforces this, finding Russia "still well ahead of the US on hard nuclear construction agreements."

Third Way does not present these findings as settled geopolitical fate. The warning embedded in the update is explicit: "Without decisive action, Russian and Chinese leadership will continue in one of the most geopolitically important energy sectors." The policy stakes are framed in terms of timing: "US policy decisions made today will have ripple effects for years to come, and it's crucial the US does everything it can to be the leader in nuclear and capture the benefits of global leadership."

The 2026 map represents the fifth iteration of a tracking effort that Third Way and the Energy for Growth Hub first launched in 2020. Each successive version has incorporated updated readiness data and demand projections; the 2026 release adds what the authors describe as "brand-new analysis" on top of the most recent available inputs. With large-scale deployments now characterized as "a near-term reality," the trajectory the map has tracked since 2020 has moved decisively from hypothetical to contractual.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?