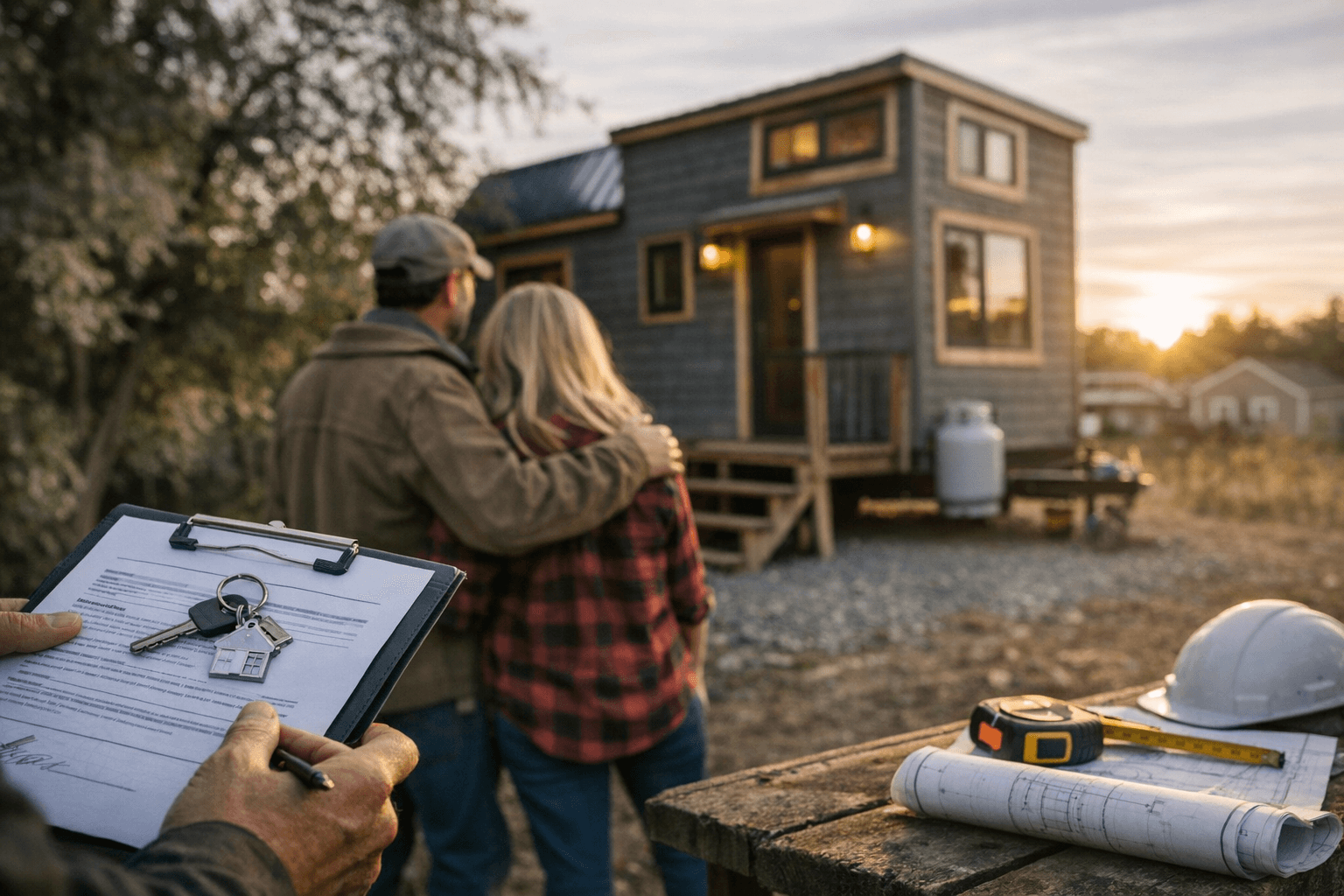

How tiny house insurance is changing in 2026 and what to do

Learn how zoning, code compliance, and dwelling type affect insurance options and practical steps to secure homeowners-style coverage.

1. Why zoning and code recognition matter

Zoning and local code recognition are the hinge points for insurance. When a jurisdiction formally recognizes tiny homes, whether via ADU rules or permits for small permanent dwellings, insurers treat those units more like houses and less like recreational vehicles, which opens up more stable policy options and clearer premiums. For community organizers and builders, pushing for explicit local rules directly improves residents’ ability to get standard coverage.

2. Permanent foundations and ADU pathways unlock homeowners-style policies

A tiny home on a permanent foundation or classified as an accessory dwelling unit (ADU) frequently qualifies for homeowners-style insurance instead of RV or “misfit” coverage. That matters because homeowners policies usually offer broader property and liability protections, better replacement-cost terms, and underwriting that reflects the dwelling’s true use. If you’re planning a build, designing for a permanent foundation or ADU compliance should be front-of-mind for both financing and long-term insurance costs.

3. THOW versus permanent small dwelling: classification changes everything

Whether a unit is a THOW (tiny home on wheels) or a permanently sited small dwelling materially affects available policy options and premiums. THOWs often end up in the RV or specialty market with different limits and exclusions, while permanent dwellings can access standard homeowner risk pools. Be explicit about classification early with local permitting, lenders, and insurers to avoid surprise denials or premium hikes.

4. State and county zoning updates are improving insurability

Across many states and counties, updated zoning that explicitly allows tiny homes or ADUs makes it easier to get residential-style underwriting. Those updates reduce ambiguity around legal status, and insurers respond to that clarity by offering products with more competitive rates and clearer terms. Keep tabs on local code changes, what’s a policy barrier today can become an insurability pathway tomorrow.

5. How underwriters are shifting from RV to homeowners frameworks

Insurers are increasingly willing to underwrite homeowners-style policies as regulators and municipalities adopt tiny-home-friendly codes. This underwriting shift isn’t universal, but it’s growing: underwriters look for evidence of permanent siting, code compliance, and standard systems to justify residential treatment. Builders and buyers should expect a mix of options for a while and plan to demonstrate residential equivalency where possible.

6. Document code compliance: electrical, plumbing, IR, and energy standards

Insurers want proof that a tiny house meets relevant building and safety codes. Documenting electrical work, plumbing, IR, and energy standards is essential to qualify for standard residential coverage and reduce underwriting friction. Create a compliance packet with permits, signed inspection reports, and contractor invoices so you can hand a single file to insurers or underwriters when requested.

- Local permit or ADU approval showing legal status

- Final inspection reports and certificates for electrical and plumbing

- Energy compliance or efficiency certification where applicable

- Photos of permanent connections, foundations, and installed safety devices

7. Practical documentation checklist to carry to the insurer

When shopping coverage, bring clear documentation to speed approval and lower risk of rejection:

This checklist turns abstract assurances into verifiable facts insurers can rely on.

8. Steps to take when shopping for coverage

Start by confirming the legal status of your unit with municipal code officers and get any ADU or foundation permits in writing. Next, assemble code-compliance documentation and then contact insurers knowledgeable about small dwellings or specialty markets. Always disclose solar and battery systems and discuss rental use upfront; non-disclosure is the fastest way to void coverage.

9. Rental use and liability: consider umbrella coverage

If you plan to rent your tiny home, long-term or short-term, treat liability as a central decision point. Standard homeowners policies may limit coverage for rental activities, so an umbrella liability policy is often a prudent layer of protection for hosts. Talk specifics with brokers: declaring rental use and buying proper liability limits protects both personal assets and community projects that host short-term stays.

10. Solar and battery systems need to be declared

Solar panels and battery storage affect underwriting and must be declared to insurers. These systems can raise replacement costs and pose different risk profiles, but when documented and installed to code they often qualify for coverage rather than exclusion. Get equipment specs, installation certificates, and maintenance records to present to carriers.

11. Work with builders, lenders, and community organizers early

Successful tiny-home deployments coordinate builders, lenders, local officials, and insurers from the start. Builders should construct to code with permit-ready plans; lenders will want to see that legal status and insurance pathways exist; organizers should push for clear local rules to benefit the whole community. This team approach prevents last-minute reclassification that can derail financing or coverage.

12. Record-keeping and ongoing compliance preserve coverage

Insurance isn’t a one-and-done transaction, maintain records of inspections, repairs, upgrades, and any changes in use. Keep digital and hard copies of permits, inspection reports, and proof of safety devices so you can respond quickly to questions or claims. Regular maintenance and documentation are low-effort ways to keep premiums predictable and claims smooth.

The takeaway? Treat tiny-house insurance like a build-spec item: plan for legal status, build to code, document everything, and tell your insurer about systems and use up front. Our two cents? Get the paperwork in a single folder, lean on local code clarity, and buy liability you can’t outgrow, small homes, big responsibility.

Know something we missed? Have a correction or additional information?

Submit a Tip