Tiny house trends, financing, and regulations shaping 2026

Learn what’s driving tiny house demand, how prefab and financing options are evolving, regional hotspots, and practical steps to navigate land and zoning.

1. Demand forces fueling adoption

Tiny houses are poised for continued interest into 2026 because affordability pressures, remote-work mobility, and multi-generational living needs are converging. Rising housing costs push people to consider lower-cost footprints, while remote work untethers buyers from commute constraints and makes mobility a selling point. Multi-generational interest, parents downsizing, families adding accessory units, and adult children seeking independent spaces, keeps the market diverse, from weekend cabins to full-time homes.

2. Expanded prefab and modular capacity

Manufacturers are scaling prefab and modular production to meet growing demand, shortening build timelines and improving quality control. Factory-built modules let buyers avoid long site construction delays and benefit from standardized energy, insulation, and wiring systems. That industrial approach also opens up more price points: entry-level factory shells for DIY finishers and high-end turnkey units for buyers seeking an all-in-one solution.

3. Regulatory shifts accelerating adoption

Regulatory change is the wildcard that will determine where tiny housing takes hold fastest; look for localized ADU updates and more permissive tiny house on wheels (THOW) allowances in select cities. Cities adjusting accessory dwelling unit rules lower barriers for backyard builds and multi-unit lots, while municipalities revising vehicle-based rules make THOWs legal living options in more places. Pay attention to local planning meetings, policy updates often move at the municipal level and create immediate opportunities or constraints.

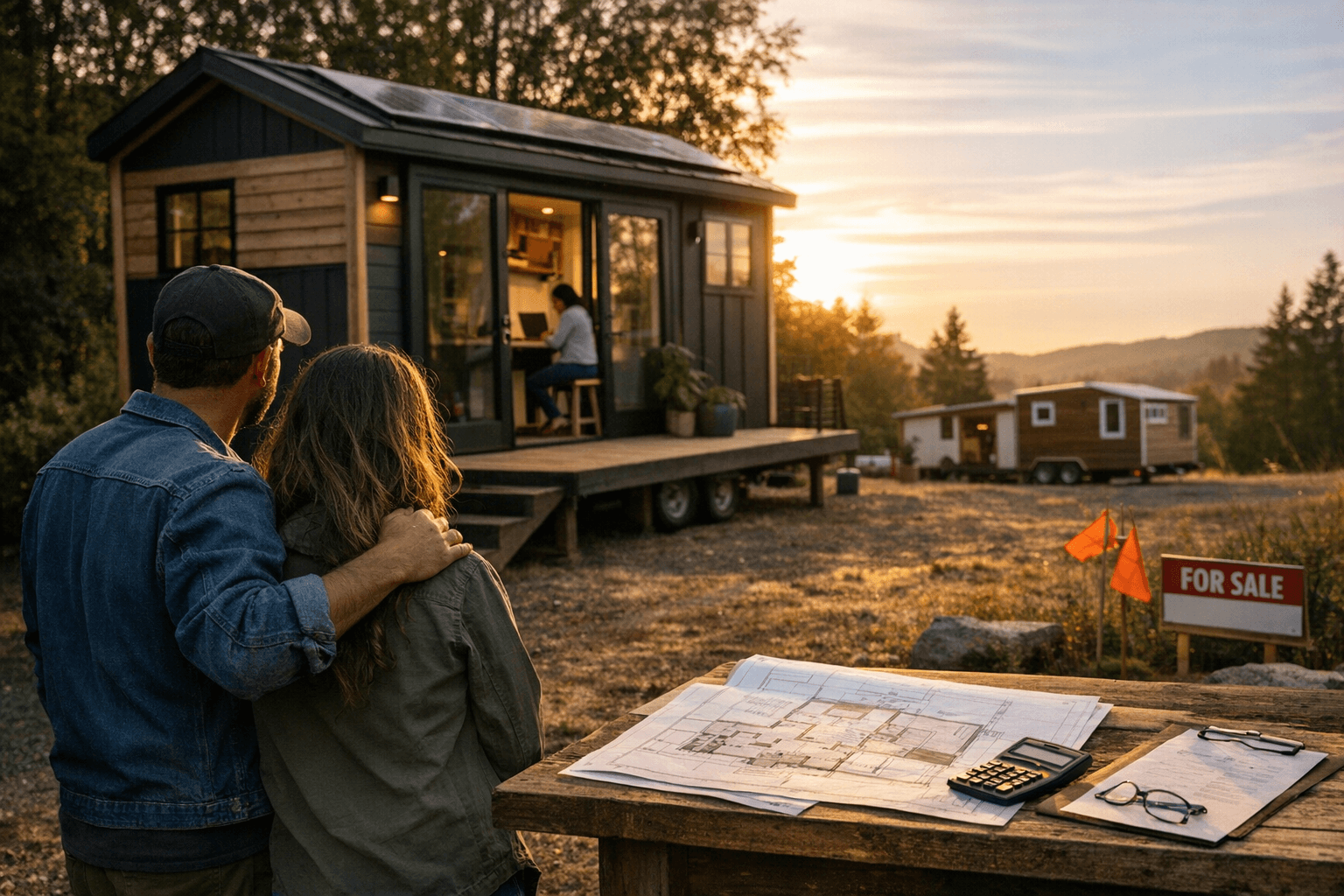

4. Pricing ranges to expect

Tiny home pricing varies widely depending on size, finish, and delivery model, from modest DIY builds to premium prefab units. Expect basic shell-and-deliver options to sit at the lower end, while fully finished, high-spec tiny homes with custom cabinetry, efficient HVAC, and solar can reach prices that mirror small conventional homes. Factor in land costs, utility hookups, permit fees, and transportation when comparing sticker prices; those add-ons often double or triple total project cost in high-demand areas.

5. Financing trends and creative lending

Financing for tiny houses is becoming more inventive: builder partnerships, RV-certification loans, and rent-to-own options are all gaining traction. Builder partnerships may offer staged payments or bundled land-and-home packages that lower upfront risk and simplify logistics. RV-certified loans suit wheel-based tiny homes but can carry different interest and term structures than traditional mortgages, and rent-to-own paths help buyers hedge against conventional lending barriers and build equity or test a community fit before committing.

6. Regional hotspots and why they matter

Adoption clusters in regions where land availability, local policy, and lifestyle match: think sunbelt metros with permissive ADU rules, mountain towns with cottage tourism demand, and coastal communities experimenting with backyard units. Each hotspot has its own pull, job markets and cost-of-living pressures, tourism-driven short-term rental markets, or experimental zoning that encourages infill. For buyers and builders, picking a region means balancing resale prospects, permitting complexity, and community reception.

7. Land availability, zoning friction, and insurance hurdles

The biggest recurring barriers are access to suitable land, zoning friction, and insurance/financing limitations. Small lots and infill parcels are scarce in many cities, and zoning or minimum square footage rules can block tiny projects outright. Insurance companies and lenders still treat many tiny homes inconsistently; coverage may require special endorsements or be unavailable unless a unit meets specific construction or certification standards. Plan contingencies: consider land trusts, lease agreements, or communities that already accommodate tiny builds.

8. Practical steps for buyers and builders

1. Research local zoning and ADU rules first, permits make or break feasibility and differ by neighborhood and municipality.

2. Decide on delivery model: DIY, prefab, modular, or builder turnkey; each changes timeline, cost predictability, and financing options.

3. Vet financing early: explore RV loans for THOWs, builder-backed financing, and rent-to-own if conventional mortgages aren’t available.

4. Budget for site costs, utility hookups, foundation or wheel permits, transport and crane fees, and impact or connection fees often surprise buyers.

- Tip: Join local tiny house groups or community land trusts to find pooled land opportunities and learn from neighbors' permit experiences.

- Tip: Ask builders for insurance and financing references, experienced shops can often point to lenders or insurers familiar with tiny models.

9. Community relevance and practical value

Tiny housing isn’t just a design trend; it’s a neighborhood-level tool for flexible housing supply and intergenerational solutions. When done well, tiny homes add gentle density, enable aging-in-place ADUs, and create affordable stepping-stone paths for younger households. Engaging with local planning boards, shadowing a neighbor’s build, or participating in pilot programs helps normalize tiny housing and reduces the NIMBY friction that stalls projects.

The takeaway? Tiny houses are more than a lifestyle garnish; heading into 2026 they’re a pragmatic response to affordability, mobility, and family needs, but success depends on matching the right product (THOW vs. modular), financing path, and location-specific rules. Our two cents? Start with permits and financing before falling for the cutest floorplan, land and legal clarity saves time, money, and heartache down the road.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?