Games Workshop Stock Rises on Warhammer Licensing and IP Momentum

Games Workshop stock jumped ~2.9% on March 23 as Warhammer's expanding licensing pipeline — from Dawn of War 4 to an Amazon Prime deal — fuelled fresh investor confidence in the FTSE 250 standout.

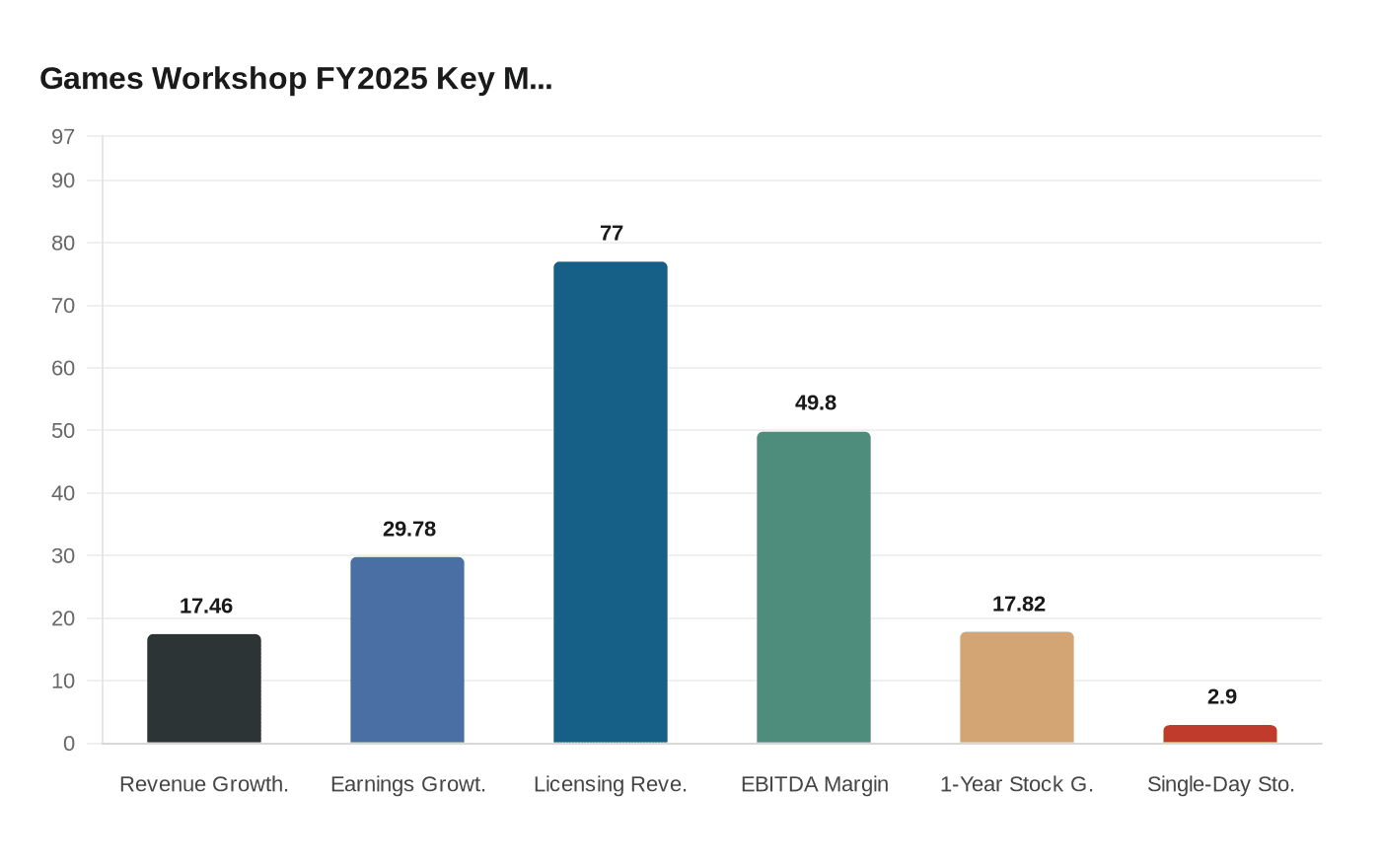

Games Workshop Group PLC (LSE:GAW) climbed approximately 2.9% on March 23, 2026, with a Kalkine analysis by Ankur Sharma pointing to Warhammer IP momentum and high-margin licensing revenues as the primary engines behind the move. For a stock that has already gained roughly 17.82% over the past year, a single-session pop of that size signals something beyond routine buying.

Games Workshop delivered double-digit growth across all segments in its most recent fiscal year, with licensing revenue up 77%, driven by strong IP monetization and video game success. The licensing pipeline backing that growth is now broader than it has ever been. Warhammer has expanded far beyond its tabletop origins to become a multimedia franchise spanning video games, novels, streaming series, and an ever-growing array of licensed products. Dawn of War IV, developed by King Art Games and published by Deep Silver, is set to release for Windows PC in 2026, adding to a video game slate that already includes ongoing seasons for Space Marine 2 and Darktide. Creative Assembly is simultaneously building out Total War: Warhammer 40,000, extending the collaboration between Creative Assembly and Games Workshop into console territory for the first time in the franchise's history.

On the media side, the live-action endeavour remains in development with Amazon MGM Studios, Henry Cavill, and Vertigo. A standalone Warhammer Age of Sigmar episode is also on the way for Prime Video. Those deals represent exactly the kind of high-profile, recurring-royalty arrangements that institutional money chases in a growth name.

The Kalkine analysis frames the stock's appeal in the context of Games Workshop's structure. The company operates what it describes as a "unique vertically integrated business model, combining product manufacturing, retail, and global licensing," and that architecture gives it pricing power most peers cannot replicate. Games Workshop has already pushed through approximately 3.5% price rises on miniatures and books, absorbing tariff headwinds without sacrificing margin. The company's current EBITDA margin sits at 49.80%, a figure that keeps both institutional and retail investors anchored to the thesis.

Games Workshop operates through two segments: Core, which covers all revenue from the design, manufacture, and sale of fantasy miniatures and related products; and Licensing, which covers all revenue from licences granted to external partners. The licensing segment, while smaller in absolute terms than Core, is the one investors are pricing for growth. In fiscal year 2025, Games Workshop's revenue reached £617.50 million, an increase of 17.46% year on year, with earnings up 29.78% to £196.10 million.

The March 23 move also reflects a broader shift in how fund managers are positioning within the FTSE 250. With Warhammer 40,000 functioning as a transmedia franchise generating royalties across PC, console, mobile, streaming, and merchandise simultaneously, Games Workshop offers the recurring-revenue profile that growth-oriented UK equity investors have been seeking. The grimdark universe that started as a tabletop hobby has become, in financial terms, one of the most efficiently monetized IP portfolios on the London Stock Exchange.

Know something we missed? Have a correction or additional information?

Submit a Tip