Natural diamond prices soften in Q1, lab-grown declines deepen sharply

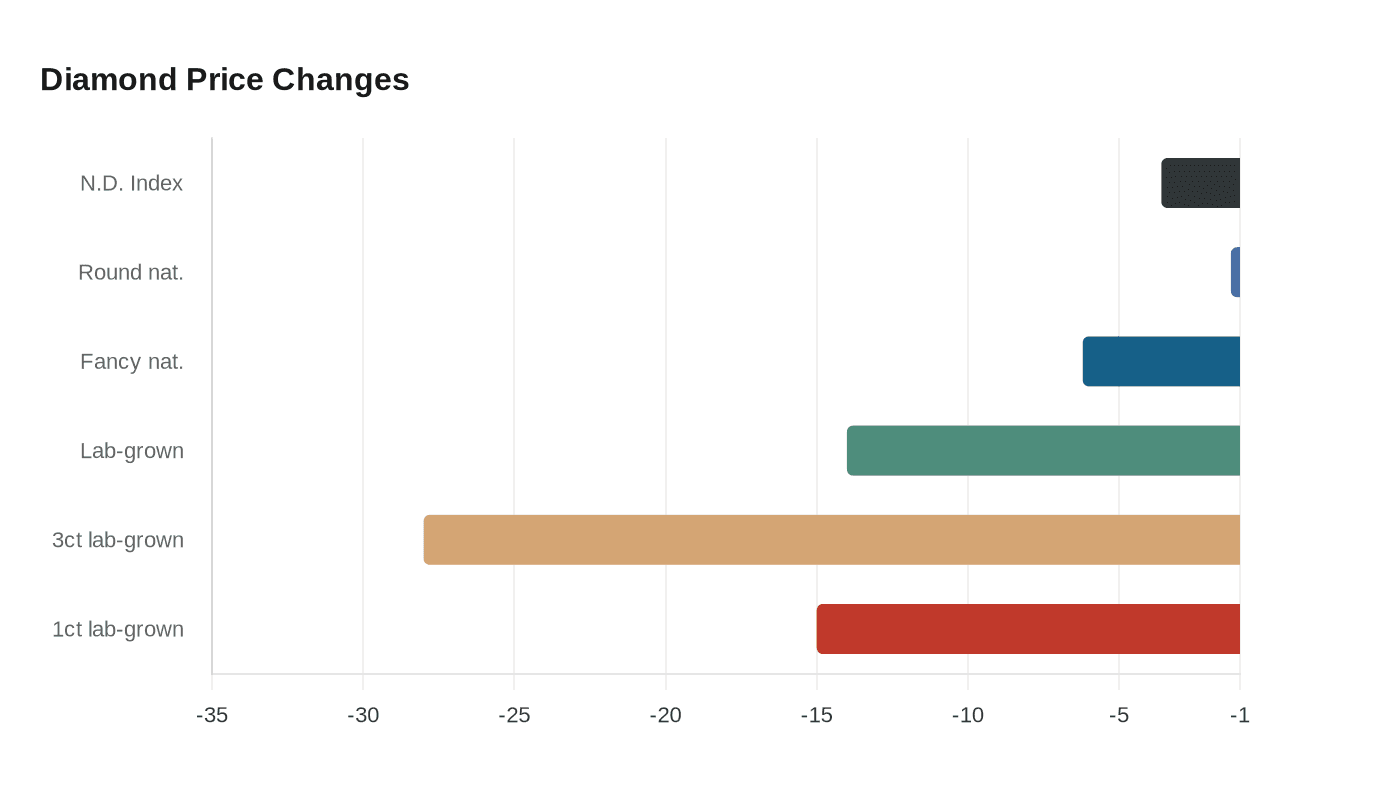

Smaller natural rounds held up in Q1 even as the index slipped 3.6%, while lab-grown wholesale prices fell 14% and 3-carat stones sank 28%.

The clearest signal for buyers in the opening quarter was not just that diamonds got cheaper, but that pricing power split sharply by size and category. David Blomquist and Edahn Golan at UNI Market Insights tracked a market that softened without losing order, with the Natural Diamond Index down 3.6% and round diamonds down only 1.3% in Q1 2026. Fancy diamonds moved lower at a steeper 6.2%, setting up a market where the smallest, most commercial natural goods proved more resilient than the broader basket.

That resilience was most visible in 0.30-carat and 0.50-carat rounds. Prices slipped just 2% and 1.5% respectively, while supply fell 19% and 13%. That is the kind of tightening that matters in the trade: when available goods shrink faster than prices, negotiating room narrows and inventory turns into leverage. For buyers hunting natural stones, the message is clear. Smaller rounds did better than expected because supply was tighter, not because demand suddenly surged, and that kept those categories relatively balanced through the quarter.

The picture was much harsher in lab-grown. Wholesale prices fell 14% in Q1, with the deepest cuts in larger sizes. Three-carat rounds dropped 28%, compared with a 15% decline for 1-carat rounds. Inventory has also been building far faster than sales, with the inventory-to-sales ratio climbing from the high single digits in 2020 to nearly 50% now. That is the kind of stock overhang that pressures wholesalers first and then cascades into retail, especially where stones are large enough to feel discretionary rather than essential.

The backdrop helps explain why the market now looks bifurcated. De Beers Group said rough diamond production fell 35% in Q4 2025 to 3.8 million carats as it produced into prevailing demand levels, reinforcing the discipline that has supported higher-quality natural stones. At the same time, March jewelry sales rose 5% year over year, but the lift came mainly from higher average selling prices rather than unit growth. Natural diamonds at the top end are holding their ground; smaller commercial goods and lab-grown stones are where prices are still vulnerable.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?