Natural diamonds face Gen Z pressure as lab-grown gains ground

Lab-grown stones now dominate engagement rings, but natural diamonds are fighting back with tighter pricing, sharper storytelling, and a harder sell on value.

The new fight is not over rarity alone

Lab-grown center stones now account for 61% of engagement-ring purchases, a number that has forced natural diamonds into a far more complicated conversation. The pressure is not just about losing share; it is about losing the old assumption that rarity automatically justifies the price.

That is why the natural-diamond trade is being pushed to rethink three things at once: pricing discipline, the language used at the counter, and what value is supposed to mean when a younger, budget-conscious buyer is comparing mined and lab-grown side by side.

What the market signal really says

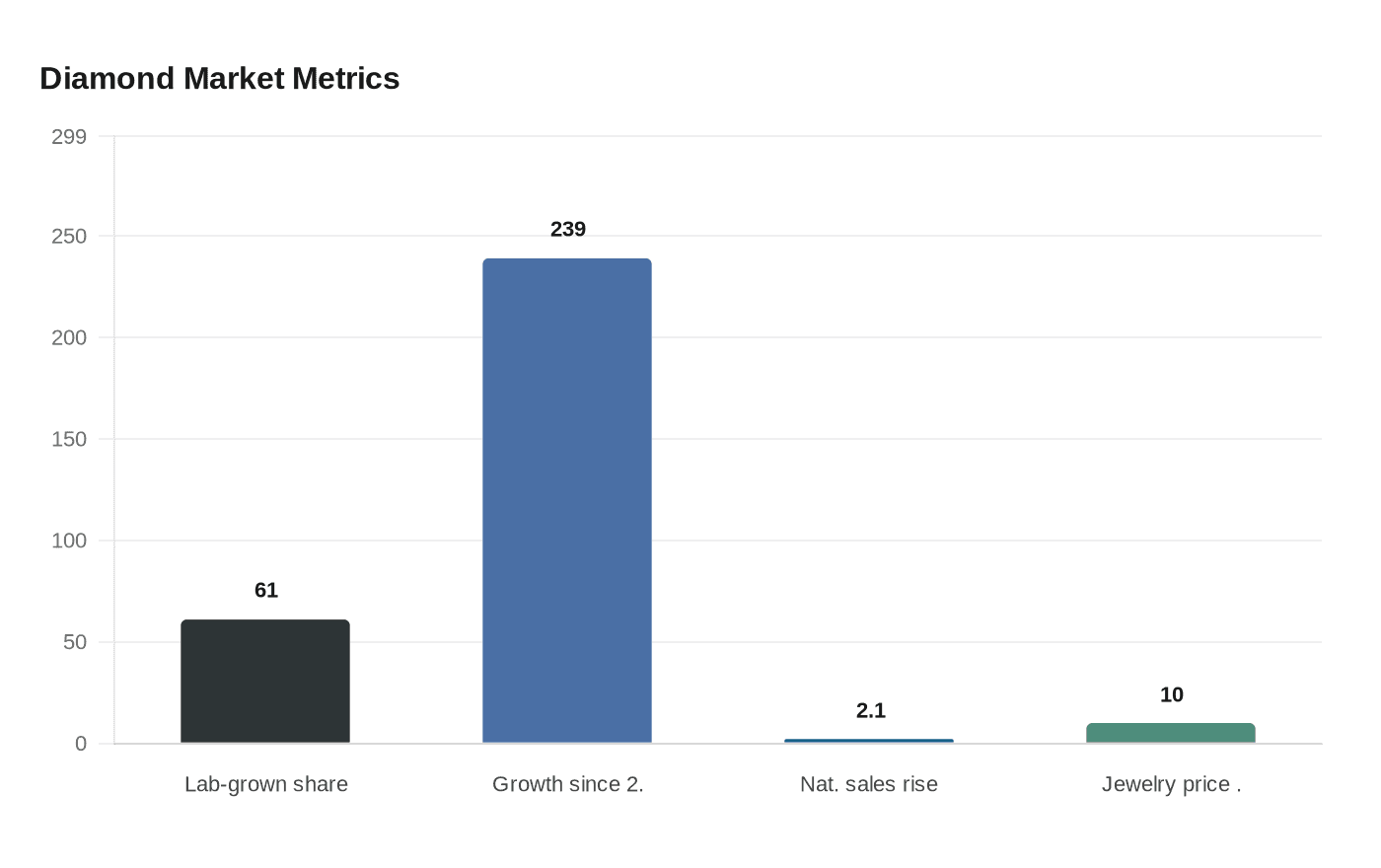

The clearest read on the shift comes from The Knot Worldwide’s 2026 Real Weddings Study, which captured self-reported responses from 10,474 U.S. couples married between January 1 and December 31, 2025. In that sample, lab-grown center stones appeared in 61% of engagement-ring purchases, a 239% jump since 2020. Industry coverage also points out that 2024 was the first year lab-grown center stones passed 50%, which makes the move feel less like a blip and more like a structural reset.

That does not mean natural diamonds have collapsed. It does mean the category can no longer rely on legacy prestige to close the sale. When a buyer can see a larger lab-grown center stone for less money, the natural diamond pitch has to work harder and faster, especially in stores where the first question is no longer “Is it real?” but “Is it worth it?”

Natural diamonds are holding up, but the story is more selective

The counterpoint is important. The Natural Diamond Council’s 2025 trend reporting says U.S. natural-diamond demand proved resilient despite tariffs, inflation, and sharply higher gold prices. In that data set, specialty-jeweler natural-diamond sales in the United States rose 2.1%, while the average price of natural-diamond jewelry increased 10%. The report draws on more than four million jewelry transactions across 2,500 U.S. specialty jewelers, so this is not a narrow anecdote dressed up as a trend.

The engagement-ring market is showing the same split. The Natural Diamond Council says the average engagement-ring price reached $7,364 in 2025, nearly 10% higher than in 2024. Some shoppers are still trading up, but they are doing so in a category that is increasingly polarized: one path leads to larger-looking lab-grown stones at a lower entry price, the other to mined diamonds that must justify their premium more explicitly than before.

Why pricing discipline matters now

For retailers, pricing discipline has become a strategic tool, not just a margin decision. If the natural-diamond category raises price without sharpening the offer, it risks sounding detached from the realities of younger buyers and tighter household budgets. If it discounts too aggressively, it undermines the very scarcity and prestige it is trying to preserve.

This is where the sales pitch has to become more precise. Natural diamonds cannot win on “bigger for less.” They have to win on cut quality, provenance, craftsmanship, and the emotional weight attached to a mined stone. That does not mean vague sustainability language or the kind of feel-good messaging that collapses under scrutiny. It means specific answers about what the stone is, where it came from, and why this piece costs what it costs.

De Beers is leaning into category marketing for a reason

De Beers Group has been clear that it wants to shift toward category marketing to revive desire for natural diamonds. That is a telling move, because it suggests the company sees the challenge as bigger than one brand or one campaign. The broader category needs reinforcement, not just louder advertising.

The backdrop is not friendly. De Beers said rough-diamond trading conditions remained challenging in the third quarter of 2025, and it said the improvement in rough demand during the first half of the year was undermined by new U.S. tariffs on diamond imports from India. That matters because India is the main cutting center for natural diamonds and the United States is the largest end-market for diamond jewelry, so tariffs ripple through the supply chain quickly and visibly.

At the same time, De Beers has emphasized that no new mines have been discovered in the past decade and that global supply is declining. That is the strongest argument the mined-diamond trade still has: not just sentiment, but scarcity. The problem is that scarcity alone no longer closes the sale when lab-grown stones can offer a different kind of value proposition right there in the showcase.

What value has to mean in-store

In practice, value now has to be explained in a way that feels concrete rather than rhetorical. A buyer facing a natural diamond and a lab-grown alternative needs to understand what changes when the stone is mined, not just what changes on the tag. That includes how the diamond was selected, whether the retailer can speak clearly about origin, and whether the price reflects quality in a disciplined way rather than old assumptions.

It also means retailers need to be specific about materials and craftsmanship. The setting, the metal weight, the cut proportions, and the overall construction matter more when the center stone itself is no longer the only headline. If the natural diamond is being sold as the better long-term choice, the rest of the piece has to support that claim with visible quality, not marketing fog.

What this battle is really testing

The real question is whether the natural-diamond industry is making a genuine strategic change or simply refining the old pitch for a new generation. The numbers suggest both momentum and vulnerability: lab-grown center stones dominate engagement rings, yet natural-diamond sales in specialty stores are still growing and prices are rising.

That tension is exactly why the next phase of the market will be won by retailers who can explain value without sounding defensive. Natural diamonds still have a story to tell, but now that story has to survive a price comparison, a lab-grown alternative, and a buyer who expects the answer to be specific.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?