Rapaport Research Report: India’s Showdown with Lab-Grown

Before you spend a single dollar on a diamond this year, a major new Rapaport analysis of India's lab-grown standoff is already reshaping what sits in your jeweler's case, and at what price.

Before you spend a single dollar on a diamond this year, understand this: the country that cuts, polishes, and certifies nearly nine out of every ten diamonds sold anywhere on the planet is in the middle of a structural identity crisis; the aftershocks are headed straight for your local jewelry counter. The March 2026 edition of the Rapaport Research Report, the diamond industry's most closely watched trade publication, maps three distinct scenarios for how India could navigate a surge in lab-grown supply hitting its most vibrant consumer market simultaneously. None of the outcomes are trivial. Each one carries direct consequences for what you find in a display case, how long you wait for a custom piece, what a salesperson tells you about value, and whether the ring you buy today holds meaning, or just sentiment, a decade from now.

India Is the Axis the Diamond World Turns On

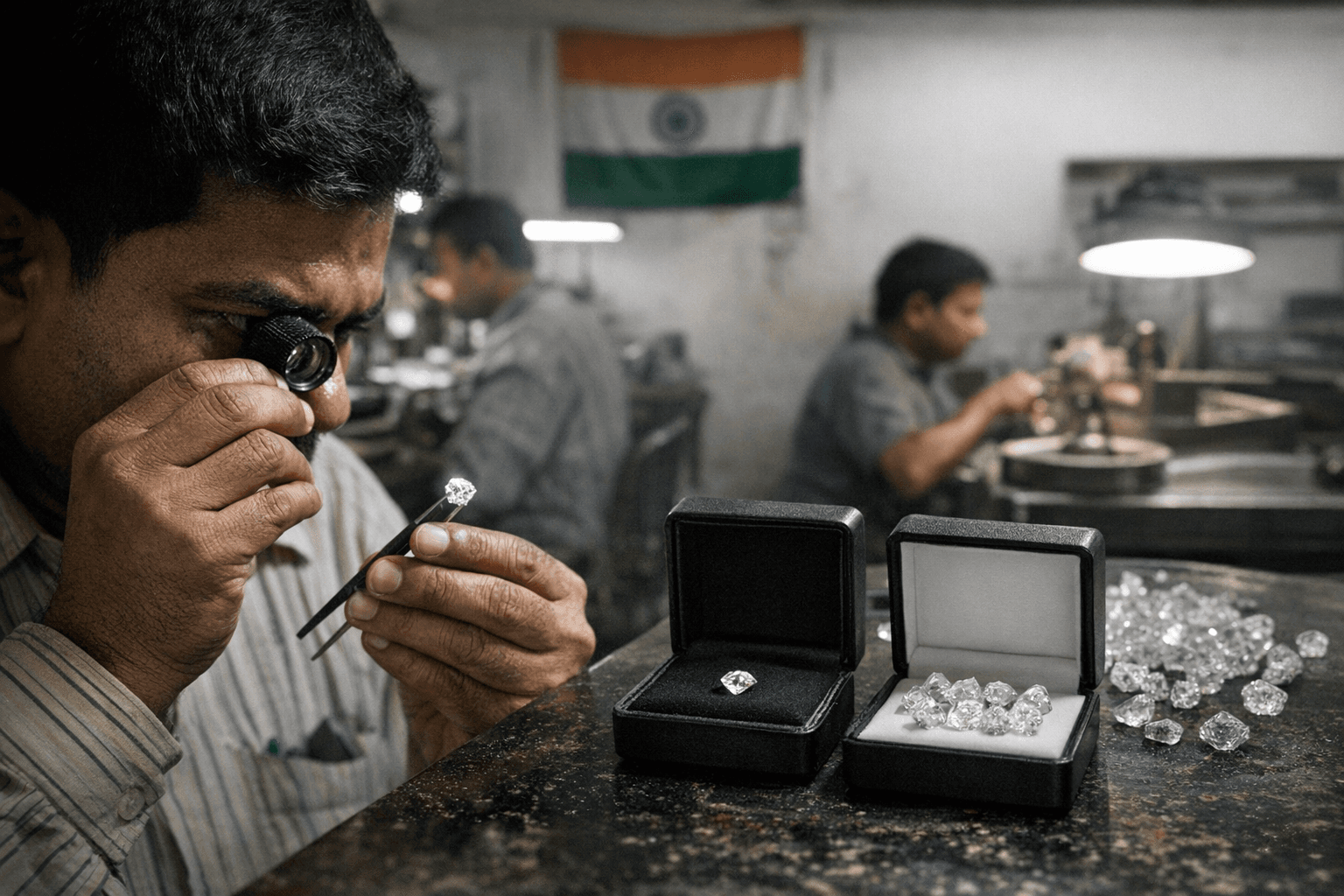

The scale of India's dominance in the global diamond pipeline is almost impossible to overstate. Surat, the diamond polishing capital of the world, processes an estimated nine out of ten of the world's diamonds. The industry there has industrialized cutting and polishing over generations, employing somewhere between 250,000 and 400,000 workers at any given time, and has cultivated a workforce whose skill at handling small stones remains unmatched globally. When rough diamonds leave the mines of Botswana, Canada, or Russia, they almost invariably pass through Indian hands before reaching a jeweler in New York, London, or Tokyo.

India is not just a manufacturing hub; it is also one of the world's fastest-growing consumer markets for finished diamond jewelry. As the country's population grows wealthier and an expanding middle class reaches for traditional markers of celebration and status, diamond jewelry has been central to that aspiration. The Rapaport Research Report assesses how likely each scenario is given Indian consumers' traditional focus on jewelry's long-term value. A bridal set is not just an aesthetic choice; it is a financial commitment expected to hold worth across generations.

That cultural weight is precisely what makes the lab-grown surge so complicated on Indian soil.

The Three Scenarios and What They Mean for Your Purchase

India's natural-diamond sector will encounter three possible outcomes as competition from synthetics emerges in the vibrant local market. Each represents a different set of pressures on supply chains, retail shelves, and price tags. Understanding all three is the most honest preparation you can do before walking into a jeweler.

Scenario One: Managed Coexistence

In this scenario, the natural and lab-grown categories successfully segment into distinct product lines. Retailers carry both, but the communication around each is clear: lab-grown diamonds are positioned as accessible, modern, and design-forward, while natural diamonds retain their premium positioning rooted in rarity, heritage, and resale value. In December 2025, Titan Company officially entered the lab-grown market with the launch of "beYon," opening its first exclusive LGD store in Mumbai, a real-world signal that this segmentation strategy is already taking shape among major retailers. Lab-grown store networks have mushroomed in recent years as venture-capital and private-equity investors have pumped funding into the sector. Titan Company and other publicly listed jewelers have also launched brands selling the product.

For shoppers, coexistence is the most navigable outcome: your retailer is more likely to be transparent about what you're buying, disclosure language on receipts and certificates is cleaner, and the two categories can be honestly compared side by side. The question you must still ask, however, is whether that segmentation holds at the counter you're standing at, or whether the conversation is being driven by margin rather than clarity.

Scenario Two: Price Disruption and Demand Shift

Lab-grown diamonds have been repricing at breathtaking speed. The growth in business has led to rampant discounting, with lab-grown diamonds trading at a discount of 97 off RapNet prices, a collapse in wholesale pricing that reflects a fundamental supply-demand imbalance as reactor capacity scales faster than demand can absorb. If price pressure intensifies in India's consumer market and natural diamond retailers respond by discounting rather than differentiating, the result could be a destabilizing race to the bottom that erodes perceived value across both categories.

In this scenario, employment in Surat's natural diamond polishing sector faces real risk. It is estimated that India's natural diamond cutting and polishing factories converted 20 percent of their production to lab-grown due to the shortage of natural rough diamonds. When structural economics rather than temporary disruption drive that shift, the labor implications are significant. And for a shopper, the risk is subtler but real: a market where prices move unpredictably makes it harder to assess whether a piece is fairly priced at all, and makes resale expectations far more speculative.

Scenario Three: Regulatory and Policy Intervention

The third scenario involves India's government and trade institutions taking a more active hand in shaping outcomes through tariffs, traceability requirements, and formal certification standards. This is not hypothetical: the Bureau of Indian Standards issued standard IS 19469:2025, legally defining a diamond as a naturally occurring substance, a definitional line in the sand with direct implications for how retailers label and disclose products. The Rapaport report examines how traceability frameworks, import tariff structures, and consumer education campaigns could collectively determine which of the three scenarios plays out. India's capacity for lab-grown diamond production has doubled in recent years, and trade bodies like the Gems and Jewellery Export Promotion Council have established dedicated Lab-Grown Diamond Committees, signaling that the industry is actively trying to build guardrails around the category.

For shoppers, a policy-driven environment is ultimately the most protective one, even if it feels abstract. Clearer standards mean more consistent disclosure. Mandatory certification language means the words "lab-grown" cannot be buried in fine print or softened with ambiguous terminology like "cultured" or "created." The risk is timing: standards take years to fully embed in retail practice, and the period before they do is precisely when confusion is most likely to benefit the seller rather than you.

What Actually Changes at the Jewelry Counter

Regardless of which scenario gains the upper hand, several immediate shifts are already detectable at retail level. Lead times on custom natural diamond pieces are becoming less predictable as supply chains absorb the ripple effects of slower rough production and shifting polishing capacity. Lab-grown availability, by contrast, has never been broader: the India lab-grown diamond jewelry market is valued at USD 453.7 million in 2026 and is projected to reach USD 1,798.6 million by 2036, growing at a CAGR of 14.8%. That trajectory virtually guarantees the product will be in more stores, in more styles, and at more accessible price points with each passing season.

Value positioning language is also shifting noticeably. Natural diamond retailers are leaning harder into concepts of rarity, provenance, and cultural meaning, precisely the things Indian consumers have historically valued. At January's IIJS Bharat Signature show in Mumbai, two main topics dominated conversation: the gold price, which was on its way to a record high, and the lab-grown question. Both were being treated as investment-grade decisions, not just aesthetic ones. Richa Singh, Managing Director for India and the Middle East at the Natural Diamond Council, says that "in India, where natural diamonds hold deep cultural and emotional significance, there is a growing need to address rising consumer curiosity and confusion."

That confusion is being created partly by inconsistent retail language and partly by the speed of the market's evolution. Lab-grown diamonds offer identical chemical, physical, and optical properties to mined diamonds, verified by the Gemological Institute of America (GIA) and the International Gemological Institute (IGI). But the terminology on those certificates is not always the same as what appears on a retail tag or receipt. That gap is where shopper vigilance matters most.

The Questions to Ask Before You Buy

The Rapaport report's three scenarios, taken together, function as a practical prompt list for anyone making a diamond purchase this year. Carry these into any jewelry conversation:

- Origin: Is this stone natural or lab-grown? Do not accept "diamond" as a complete answer. Ask for the word to be used precisely on any written documentation, and ask which country the rough was sourced from if buying natural.

- Certification: Which independent laboratory graded this stone: GIA, IGI, or another body? And can you see the actual certificate? A certificate number should be laser-inscribed on the girdle of any responsibly sold stone. The standard IS 19469:2025 in India now provides a legal framework for what "natural diamond" means; ask whether the retailer's documentation aligns with it.

- Disclosure language: What does the receipt, packaging, or tag say exactly? "Lab-grown," "lab-created," and "synthetic" are all acceptable terms. "Cultured," "real," or an unqualified "diamond" without origin disclosure are not sufficient. If the store cannot show you written disclosure language, treat that as a red flag.

- Upgrade and resale expectations: For a natural diamond, ask the retailer explicitly whether they offer any resale or upgrade program, and get the terms in writing. For a lab-grown stone, be realistic: given that wholesale prices for lab-grown have declined sharply and continue to do so, resale value is not a reliable feature of the purchase. If a salesperson implies otherwise, ask them to put it in writing.

India's diamond reckoning is not a distant trade story. It is the upstream condition of every diamond piece sold in every market. The country that shapes the stone also, increasingly, shapes the story around it. How that story gets told, and how honestly, will be decided by the policy choices, retail disclosures, and consumer expectations forming right now.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?