How to pay for an engagement ring, cash, credit or financing

The cheapest ring is the one you can pay off without carrying it for months. Once interest enters, a $4,600 purchase can cost hundreds more.

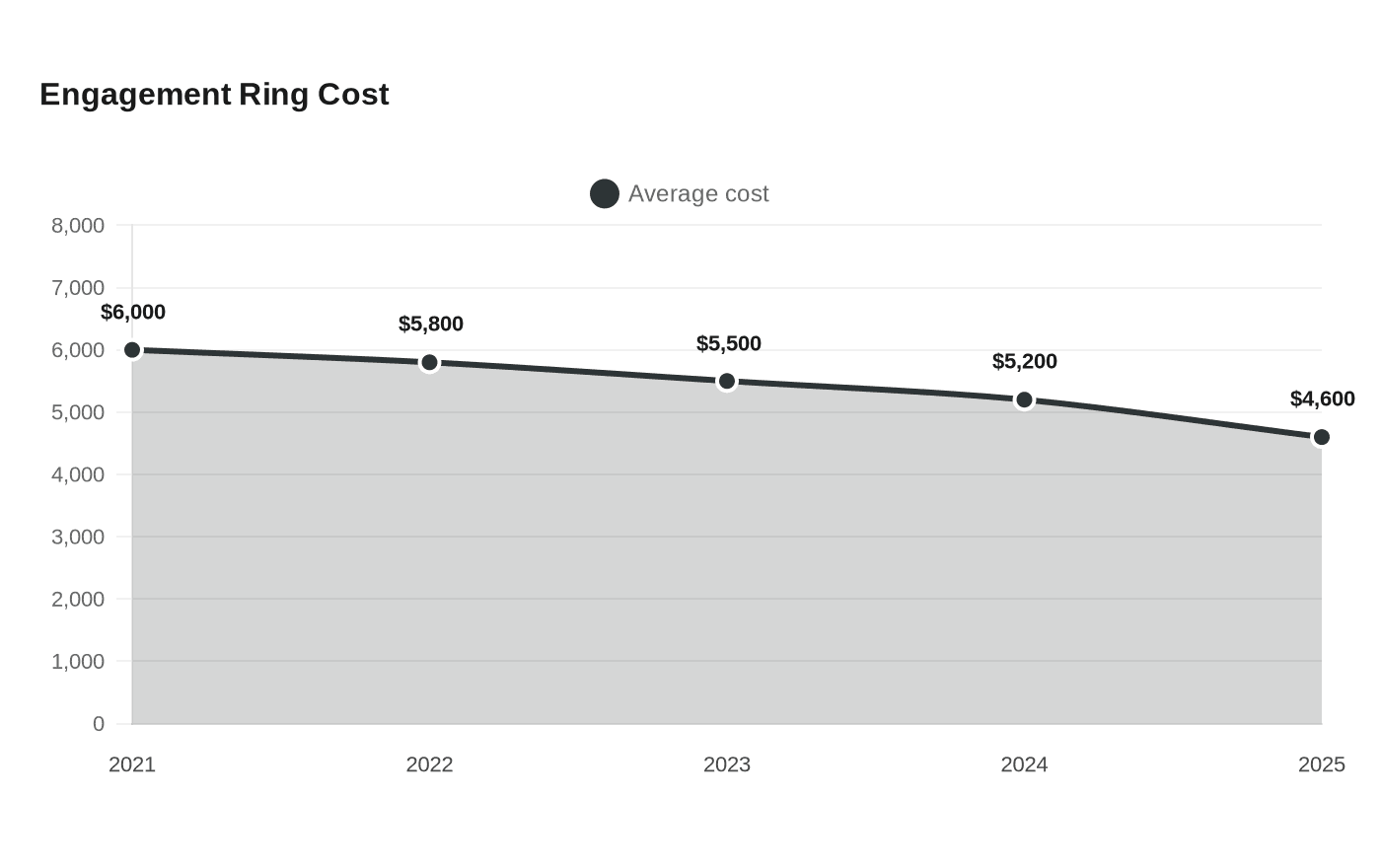

Ring shopping is where romance and arithmetic meet. The average engagement ring cost $4,600 in 2025, and the payment method you choose can change the final price almost as much as the center stone itself. Cash keeps the tally clean; credit, BNPL, store financing and personal loans stretch the purchase, but they also stretch the risk.

The ring price is the first decision

The Knot’s figures show a market that has been easing down: $6,000 in 2021, $5,800 in 2022, $5,500 in 2023, and $5,200 in 2024 before landing at $4,600 in 2025. That same survey work found that 16% of respondents negotiated engagement-ring prices, which is a useful reminder that the sticker price is a starting point, not a law of nature. The final cost also reflects more than the center stone. Precious metals like gold and platinum, labor, craftsmanship and a build that can take two to six weeks all sit inside the number you see in the case.

That matters because financing magnifies every extra dollar. If the ring is already a several-thousand-dollar purchase, the cheapest path is the one that does not add time, interest or penalty fees. NerdWallet’s guidance is blunt on the point: cash is ideal when possible.

Cash: the cleanest close

Cash is the top choice when you can pay without draining the money you need for rent, repairs or an emergency. It leaves no balance behind, no payoff calendar to manage and no chance that a proposal is followed by months of statements. It also gives you a cleaner comparison when you are negotiating, because you are talking about the true price of the ring, not the price plus financing friction.

That does not mean cash is always the most comfortable option. A ring should not raid the account that keeps your life stable, especially when the average purchase already sits at $4,600. Cash is the least expensive route only if it preserves the rest of your financial flexibility.

Credit cards and 0% promos: useful only if you beat the clock

NerdWallet says the right credit card can buy you an interest-free runway or rewards on the purchase, and that is the logic that makes promo cards attractive for engagement rings. Used well, a card can protect savings while you spread out the bill over a short window. Used badly, it turns into revolving debt with a rate that can make a ring far more expensive than it looked under the showroom lights.

The Federal Reserve’s G.19 data show why that matters. Commercial-bank credit-card APRs are 14.60% for all accounts and 16.45% for accounts assessed interest, so the cost of carrying a balance can climb fast once a promo expires or a payment is missed. The Fed also says G.19 consumer-credit data are released around the fifth business day of each month, which is a reminder that borrowing conditions move while you are still shopping.

BNPL and jeweler financing: simple on the surface, tricky in practice

Buy-now-pay-later plans look gentle because the CFPB describes them as typically four-payment, zero-interest loans used for retail purchases, and the market expanded rapidly in the United States from 2019 to 2023. That convenience can make BNPL feel almost invisible, which is exactly why it deserves scrutiny. The CFPB withdrew several BNPL guidance documents, including its 2024 BNPL Interpretive Rule, on May 12, 2025, so the fine print matters more, not less.

Jeweler financing sits in the same middle ground. NerdWallet includes financing offered directly through the jeweler among the main ways to pay for a ring, and that can preserve cash in the short term. The question is not whether the checkout flow is easy. It is whether the total repayment is still comfortable after the novelty fades and the first bill arrives.

Personal loans: fixed payments, real interest

Personal loans are the more formal, less romantic option, but they can be useful when you want a fixed monthly payment and a clear end date. The Federal Reserve’s latest G.19 release lists 24-month personal-loan rates at 9.38%, which is lower than the card rates above, but still a cost you are paying for time. On a $4,600 ring, that rate works out to about $211 a month and roughly $463 in interest over 24 months.

That is the point where financing stops being a convenience and becomes a long-term obligation. A personal loan can preserve flexibility if it fits comfortably into your budget and ends before wedding expenses pile up. It becomes a drag if the monthly payment forces tradeoffs elsewhere or if you are borrowing simply because the ring feels emotionally nonnegotiable.

How to choose without turning the ring into debt

In cost and risk terms, the order is clear: cash comes first, then a 0% promo card that you can erase before interest starts, then BNPL or jeweler financing if the installment schedule truly fits your cash flow, and finally a personal loan if you need predictability and can live with the interest. The right answer is the one that leaves the ring as a symbol, not a liability.

The smartest purchase is the one that lets you admire the setting without worrying about the statement that follows it. When the payment plan is chosen with the same care as the stone, the ring keeps its meaning and your balance sheet stays intact.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?