Anglo American pushes ahead with De Beers sale as diamond output rises

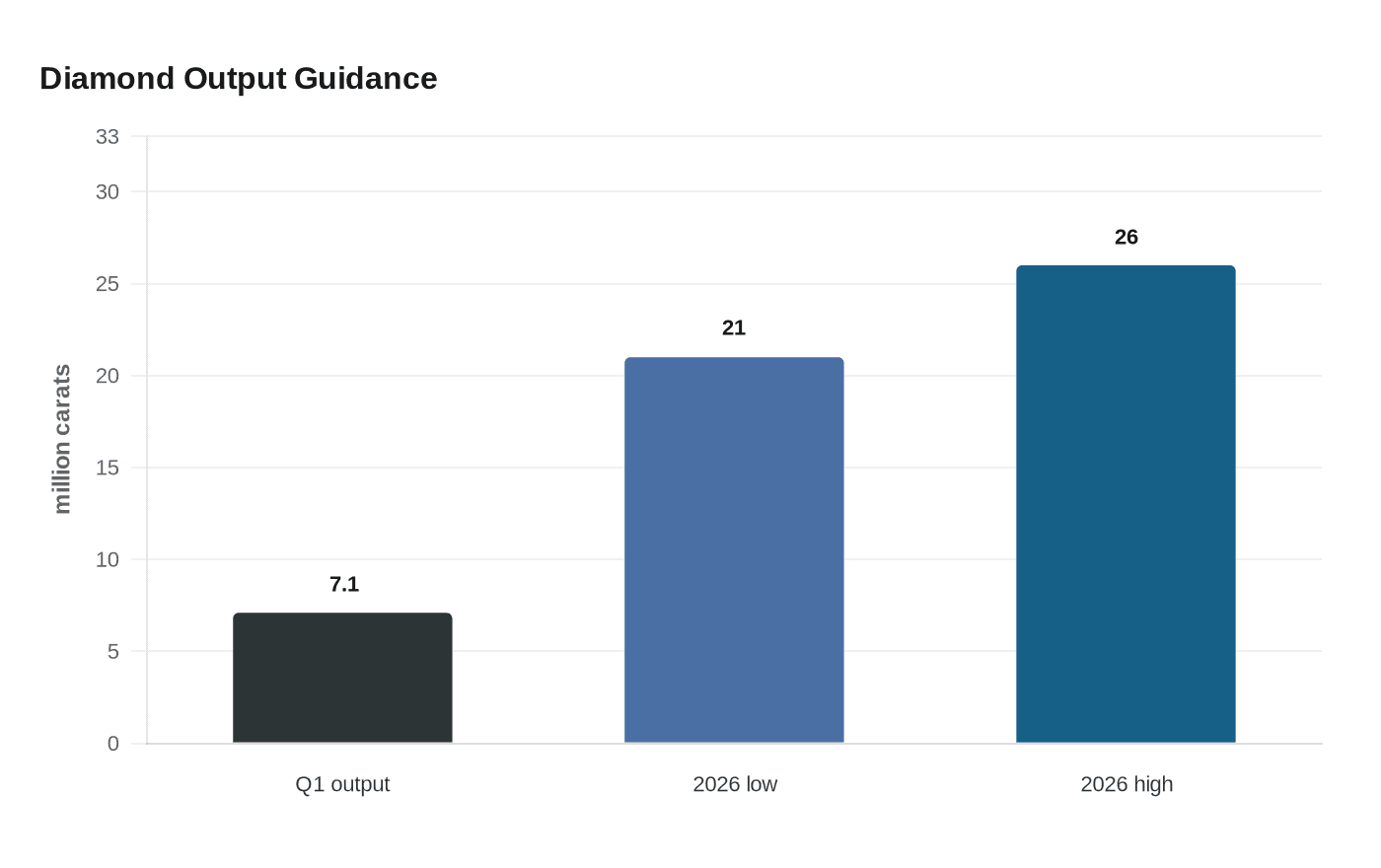

De Beers output rose 17 percent to 7.1 million carats as Anglo American pushed its sale forward, keeping diamond pricing, supply confidence and provenance in focus.

Anglo American kept the De Beers sale moving, but gave no hard deadline, even as first-quarter diamond output climbed and sales value steadied. In its 28 April 2026 production report, the miner said it was “committed to divesting De Beers” and expected to provide an update “through the course of 2026.” For the jewelry market, the immediate question is not the transaction itself but whether a new owner changes how natural diamonds are priced, supplied and sold.

The quarter brought mixed signals. Rough diamond production rose 17 percent to 7.1 million carats, lifted mainly by planned ore release at Gahcho Kué in Canada and higher volumes from Venetia underground in South Africa. Consolidated rough diamond sales revenue reached $648 million from two Sights, up from $520 million a year earlier, but the consolidated average realized price fell 19 percent to $101 per carat. Anglo left 2026 production guidance unchanged at 21 million to 26 million carats and kept unit-cost guidance at about $80 per carat.

Those numbers sit against a softer backdrop for the natural-diamond trade. De Beers said trading conditions remained challenged by industry, geopolitical and tariff headwinds. Its preliminary 2025 results showed group revenue of $3.493 billion, underlying EBITDA of minus $511 million and rough-diamond sales of $3.0 billion. The company said demand for smaller and lower-quality diamonds was under pressure, and that sentiment weakened sharply after US tariffs on Indian exports. Anglo had already written down De Beers’ carrying value by $2.9 billion in its 2024 full-year results, a blunt sign of how much value the brand had lost in a weaker market.

For independent jewelers and shoppers, the stakes are practical. De Beers remains one of the best-known names in natural diamonds, and Botswana is central to its business. Botswana holds a 15 percent stake in De Beers through the broader ownership structure, while the Debswana joint venture between Botswana and De Beers is split 50:50 and accounted for roughly 70 percent of De Beers’ annual rough diamond supply. In February 2025, the two sides extended Debswana mining licenses to 2054, pushing far beyond the 2029 expiry date that had once loomed over the asset. Interest from Botswana, Angola and Namibia in taking equity, alongside business-led groups, shows how any sale could reshape supply relationships as much as ownership.

The next 6 to 12 months will matter most if the sale changes who controls the narrative around natural diamonds: whether supply confidence holds, whether rough pricing stabilizes, and whether retailers lean harder on provenance, Botswana’s role and the long view of mined stones rather than on glamour alone.

Know something we missed? Have a correction or additional information?

Submit a Tip