De Beers CEO warns on lab-grown diamond bubble, supply slump, tariffs

Lab-grown diamond prices have collapsed as mined supply tightens, forcing retailers to explain origin, value, and resale with much more honesty.

The diamond market is splitting into two very different stories: one about lab-grown stones that have become dramatically cheaper, and another about natural diamonds facing tighter supply and renewed scarcity language. For shoppers, that means the most important question is no longer just how bright a stone looks in the case, but what kind of diamond it is, where it came from, and what the market is really promising.

The lab-grown reset

Al Cook’s warning lands in a market already under pressure. In an interview in Las Vegas with National Jeweler editor-in-chief Michelle Graff, the De Beers chief talked about the burst of the lab-grown bubble, the timeline for zero percent tariffs, and why the coming years may bring even less room for confusion between mined and synthetic stones.

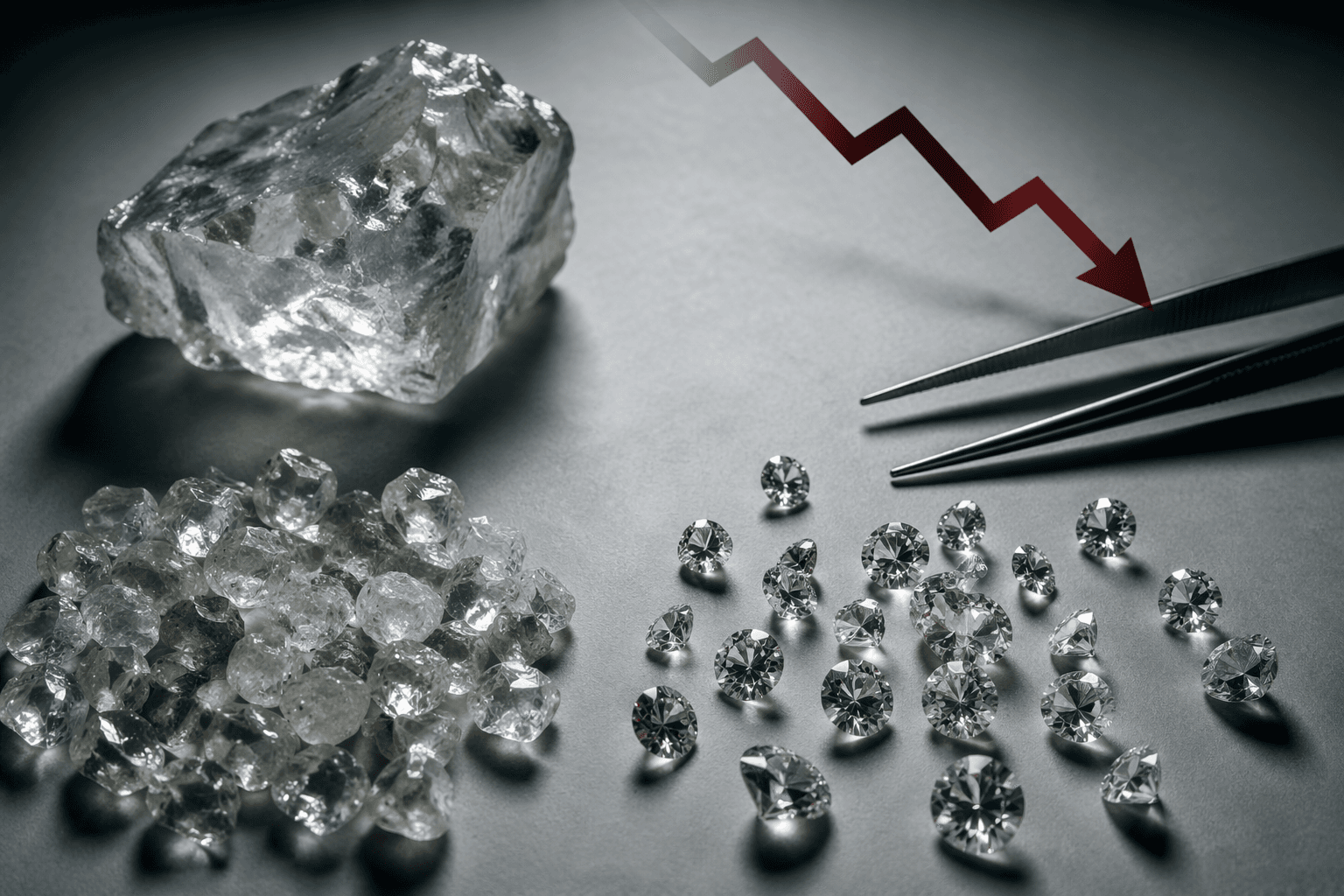

The clearest signal is price. Reuters reported in October 2025 that World Diamond Council president Feriel Zerouki said lab-grown diamonds were losing appeal because of oversupply, and that average wholesale prices for one-carat and two-carat stones had fallen by as much as 96% since 2018. That kind of collapse changes the shopper conversation fast. A lab-grown diamond can still offer impressive size and clarity for the money, but it should no longer be sold as if it behaves like a scarce luxury asset.

That is the part many jewelers still do not explain well enough. If a lab-grown diamond costs far less than a natural stone of the same size, that is not just a bargain story, it is a market-structure story. Oversupply has pushed prices down, and resale expectations need to stay modest. The cleanest language is plain language: a lab-grown diamond is a diamond, but its price path is tied to manufacturing and wholesale competition, not geological rarity.

De Beers has already acted on that reality. In 2024, the company said it would stop producing lab-grown diamonds for jewelry and focus its synthetic-diamond activity on industrial technology uses, while continuing to sell existing Lightbox inventory for the time being. That retreat matters because De Beers helped legitimize the category when it launched Lightbox in 2018, then turned away from growing jewelry stones once the economics stopped looking compelling.

Why natural diamonds are getting louder

The other side of the market is not stable either, but its pressure runs in the opposite direction. De Beers’ mined output fell to 21.7 million carats in 2025 from 24.7 million carats in 2024, while Anglo American reported that the average rough price ended 2025 at $142 per carat, down from $152 the year before. Anglo also said De Beers lost more than $500 million in 2025, after earlier writedowns of $1.6 billion in 2024 and $2.9 billion in February 2025.

For the shopper, that does not mean every natural diamond suddenly becomes a better investment. It does mean the supply narrative around mined stones is changing. De Beers lowered its 2026 production guidance to 21 million to 26 million carats from 26 million to 29 million, citing a difficult rough-diamond market and maintenance shutdowns at key mines. Botswana’s Jwaneng mine, the world’s richest diamond mine, was offline for the entire fourth quarter of 2025, while Canada’s Gahcho Kué was the only bright spot in that period, with production rising to 949,000 carats.

That shrinking supply is exactly why De Beers has leaned into a different kind of natural-diamond storytelling. The company launched its “desert diamonds” campaign in 2024 to highlight off-white, light yellow and brown natural stones, a way to separate mined diamonds from the colorless look that dominates much of the lab-grown category. The campaign is smart branding, but shoppers should not let it substitute for disclosure. A retailer should say whether a stone is mined or lab-grown first, then explain color, cut, clarity, and why the price sits where it does.

There is also a broader geological warning buried in the numbers. Reuters reported in February 2026 that Angola’s De Beers joint venture discovered a new kimberlite cluster, the first in three decades in the country, yet that discovery comes against a backdrop of pressure on established mines. National Jeweler has also reported Cook’s warning that 2027 could be the last year for diamond mining in Canada, which makes the supply story less like a short-cycle dip and more like a structural shift.

Ownership, tariffs, and the price you actually pay

The sale of De Beers adds another layer of uncertainty. Anglo American publicly confirmed in May 2024 that it was seeking to divest or demerge the business, and Reuters reported in February 2026 that Angola was pursuing a 20% to 30% stake in De Beers, while Botswana was also seeking a majority stake. Those talks reportedly involved closed-door discussions among Angola, Botswana, Namibia and South Africa.

That ownership fight matters because who controls De Beers will shape everything from mining strategy to marketing language. Anglo’s 2025 revenue for De Beers was $3.5 billion, including $3 billion in rough diamond sales, so this is still a major asset even in a weakened market. If a buyer or a new partner pushes harder on natural-diamond promotion, the consumer will see it first in the language at the counter: more origin stories, more scarcity claims, more pressure to see mined stones as the only authentic luxury.

Tariffs fit into that same pricing puzzle. Cook’s discussion of a timeline for zero percent tariffs is a reminder that the final sticker price on a ring is not driven by the stone alone. Trade policy can affect imported loose diamonds, settings, and finished jewelry differently, so the smartest retail conversation is specific: what is being imported, from where, and how much of the final price reflects the stone versus the metalwork and duty structure.

How jewelers should explain the difference

The best diamond sales conversation in 2026 should feel calmer, not louder. Fear-based messaging around lab-grown stones helps no one, and mushy origin language helps even less. The categories deserve honest, simple explanations.

- Say whether the diamond is mined or lab-grown before anything else.

- Explain resale expectations plainly, especially for lab-grown stones, where wholesale prices have already fallen sharply.

- If a natural diamond is being positioned as rare, describe the actual origin story, not just the romance of it.

- If tariffs are affecting price, spell out whether the impact comes from the stone, the setting, or both.

- Use color thoughtfully. Off-white, light yellow and brown natural diamonds are distinct from colorless lab-grown stones, but the story should be about material reality, not marketing fog.

The market is forcing a useful cleanup. Lab-grown diamonds are no longer the easy hedge they once looked like, and natural diamonds are no longer shielded by old assumptions about automatic scarcity. The stores that win trust now will be the ones that name the difference without dramatizing it, because buyers deserve provenance, not slogans.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip