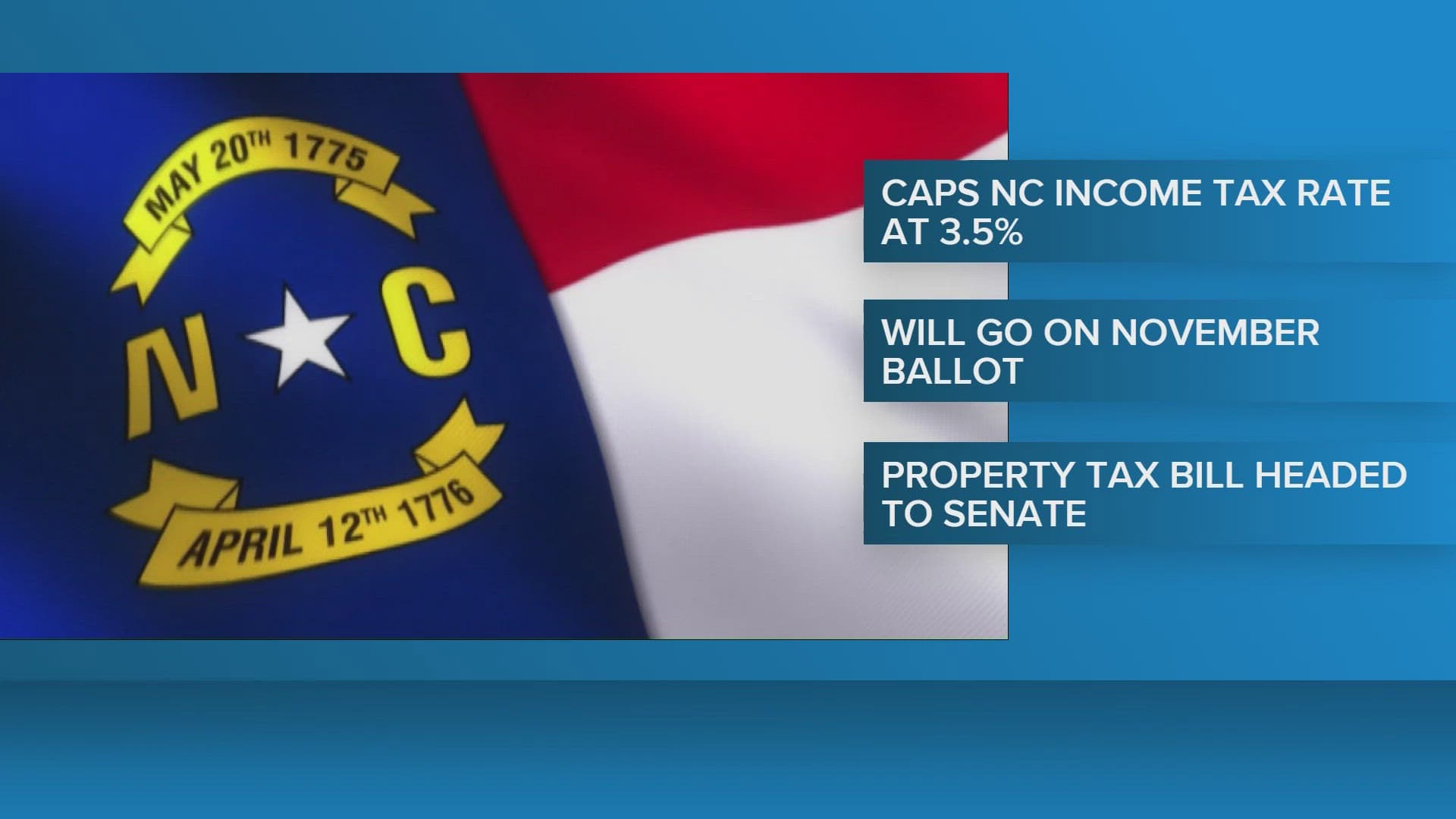

North Carolina Senate backs amendment to cap income tax at 3.5%

A 3.5% income-tax cap could lock in lower rates statewide, but in Buncombe County it may tighten the money available for schools, roads and disaster recovery.

Buncombe County residents who are already watching their property tax bills climb could soon face a second, statewide pressure point: a constitutional cap that would lock North Carolina’s income-tax rate at 3.5%. The North Carolina Senate approved the amendment as Senate Bill 1080, even as county leaders in Asheville weigh a higher property-tax rate and local families worry about school funding and housing costs.

The proposal would rewrite Article V of the state constitution so the tax rate on incomes “shall in no case exceed” 3.5%. North Carolina’s constitution now caps income taxes at 7%, and that limit has been in place since 1920, when the ceiling was first set at 6%. Legislative staff notes also show that the state’s individual income-tax rate is already scheduled to fall to 4.25% in 2025 and 3.99% in 2026 under current law.

Supporters, including Senate Republicans who advanced the measure, say the amendment would protect lower taxes from future legislatures. Senate leader Phil Berger has pushed the idea of embedding the ceiling in the constitution, while Democratic Gov. Josh Stein opposes it. WRAL reported that the proposal moved forward Tuesday.

For Buncombe County, the debate is less abstract than the constitutional language suggests. County government depends on a mix of local taxes and state support to help pay for schools, roads, transit and emergency response. A tighter statewide income-tax cap would not change local property taxes directly, but it could restrict how much room future lawmakers have to raise state revenue if demands grow for services that Buncombe and other counties rely on. That matters in Western North Carolina, where storms, rebuilding and public infrastructure needs have repeatedly tested government budgets.

State tax history shows how much North Carolina has changed over the last century. A legislative analysis says the modern system was largely set in the 1920s and 1930s, when lawmakers enacted a personal income tax in 1921 and a retail sales tax in 1933. The state’s corporate income-tax rate is scheduled to fall to 2% for taxable years beginning on or after Jan. 1, 2026, then to 1% after 2028 and 0% after 2029.

In Buncombe County, where every budget season already brings fights over what residents can afford and what public services can absorb, the question is not just whether taxes go down. It is who keeps the flexibility to pay for the next crisis, the next school need and the next round of basic services local residents use every day.

Know something we missed? Have a correction or additional information?

Submit a Tip