Fresno County housing stays active as affordability draws buyers

Fresno County homes are still moving, but the affordability story looks thinner once mortgage payments and insurance costs enter the math.

The market is still moving, but the bargain is narrower

Fresno County real estate is holding up in a way that feels almost contradictory: prices are elevated, financing is expensive, insurance is strained, and yet homes are still selling. In March 2026, Realtor.com pegged the county’s median listing price at $443,725, with homes spending a median 44 days on the market and 3,086 active listings. Redfin put the median sale price at about $430,000 and said 544 homes sold in March, up from 494 a year earlier.

That combination matters because it shows a market that has not frozen. It has simply become more selective. Buyers are still acting, but they are doing so with more caution, more math, and less room for error than they had when rates were lower.

Why Fresno County still attracts buyers

The county’s draw starts with scale and affordability relative to coastal California. Fresno County’s population was estimated at 1,035,456 on July 1, 2025, up from 1,024,125 a year earlier, so demand is not coming from nowhere. More people means more household formation, more turnover, and more pressure on a housing stock that the Census Bureau estimated at 350,647 units in 2024.

The long view also helps explain why investors still circle the market. The Federal Reserve Bank of St. Louis’ Fresno County house price index reached 333.77 in 2024, a reminder that local home values have climbed substantially over time even if individual years move up and down. Countywide building permits totaled 2,439 in 2024, which shows construction is ongoing but not at a pace that would erase pressure quickly.

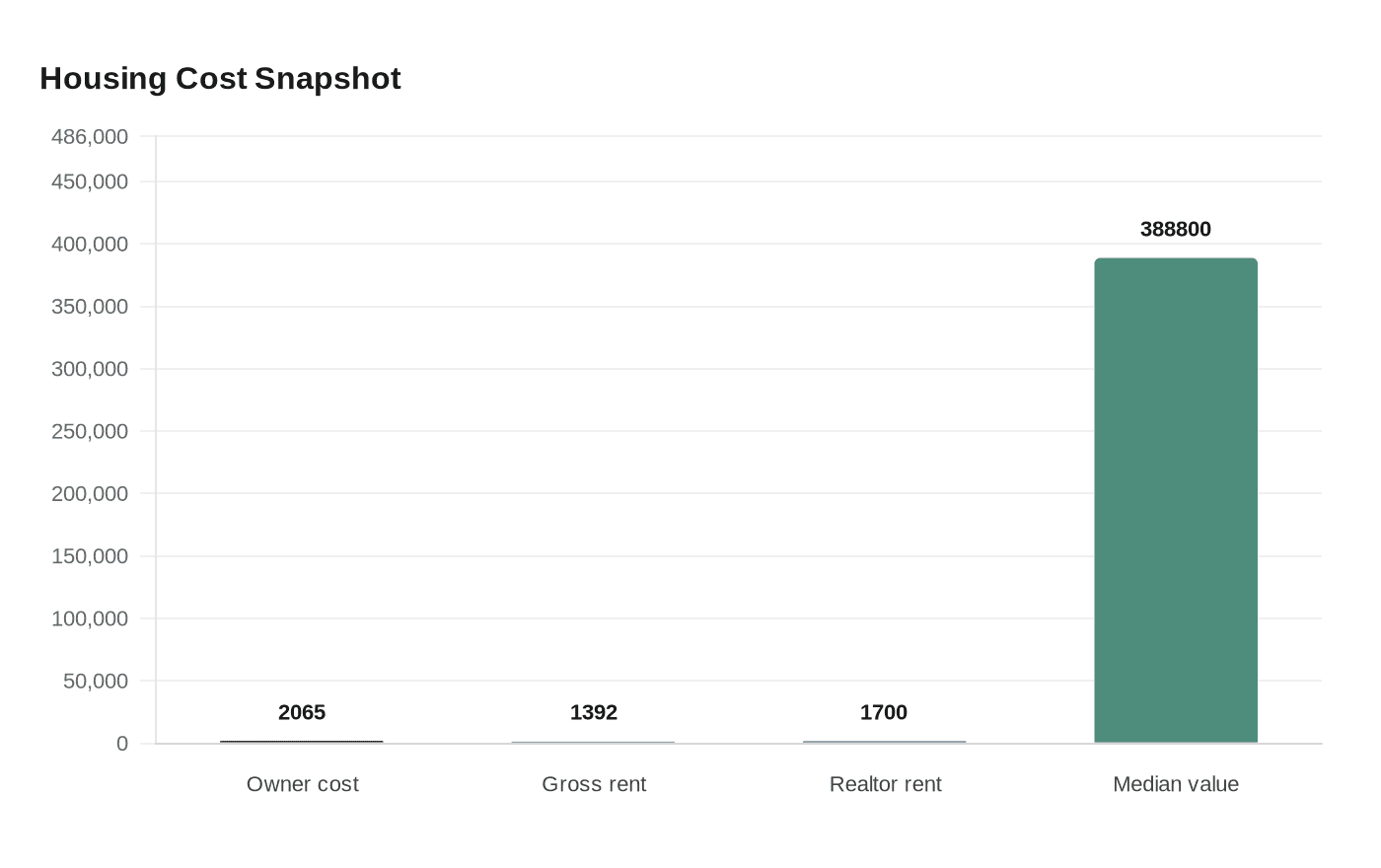

Fresno County also still looks comparatively affordable by California standards. The Census Bureau estimated the median value of owner-occupied housing units at $388,800 for 2020-2024. That is far below what many buyers face in the state’s major coastal metros, and it is the reason Fresno remains on the radar for people who have been priced out elsewhere.

Who is still winning in this market

The buyers with the clearest advantage are cash buyers and investors. They can move faster, avoid the full bite of today’s mortgage rates, and absorb higher insurance costs more easily than a household trying to stretch into its first home. In a market where the median listing price is above $443,000 and the median sale price is about $430,000, speed and certainty still buy leverage.

First-time buyers face a much tougher calculation. The Census Bureau estimated Fresno County’s median monthly owner cost with a mortgage at $2,065 for 2020-2024, compared with a median gross rent of $1,392. That means the typical mortgaged owner is already paying about $673 more per month than the typical renter, before factoring in maintenance, repairs, and the increasingly unpredictable cost of insurance.

For renters, the market is not painless either. A median rent of $1,700 in the Realtor.com data is not far above the Census Bureau’s longer-run estimate of $1,392, which suggests the rental market has also tightened. If landlords face higher premiums, those costs can flow into future lease renewals, making the rental side of the affordability story less comfortable than the headline numbers imply.

Affordability is real, but it depends on how you pay

The central question for Fresno County is not whether housing is cheaper than in much of California. It is. The real question is whether it is still affordable once financing and insurance are included, and for many households the answer is increasingly conditional.

That is where the county’s “thriving” label starts to break down. A median sale price near $430,000 may sound manageable next to coastal markets, but at current borrowing costs the monthly payment can climb quickly. Add insurance, taxes, and ordinary upkeep, and the gap between the home-price headline and the actual monthly bill widens fast.

That gap is especially important because the broader local economy is not exactly running hot. Fresno County’s unemployment rate was 8.9% in January 2026, a sign that plenty of households are still feeling strain. In that environment, even a market with active listings and decent turnover can feel strong for sellers while remaining difficult for wage earners trying to break in.

Insurance is the hidden cost that changes the equation

The insurance backdrop may be the most underappreciated force shaping local housing decisions. California’s FAIR Plan had 668,609 policies in force in December 2025, up 146% from September 2022. That surge reflects a state insurance market under heavy stress, and the pressure does not stop at the coast.

In February 2025, California’s insurance commissioner approved a $1 billion assessment of admitted-market insurers to help support the FAIR Plan after Southern California wildfires. California has also moved to reform the FAIR Plan in 2025, which shows how serious the problem has become statewide. For Fresno County owners, the practical result is clear: even inland properties can carry higher insurance-related uncertainty than they did a few years ago.

That matters to everyone in the housing chain. Investors factor insurance into expected returns. Cash buyers may be able to absorb surprises more easily. First-time buyers have to fit those costs into a monthly budget that already stretches against rates, taxes, and home maintenance.

What the numbers say about the road ahead

Fresno County’s housing market is not booming in a speculative sense, but it is active enough to keep drawing money and attention. The data point to a market supported by population growth, relative affordability, and a housing stock that still needs expansion. At the same time, the county’s unemployment rate, higher mortgage costs, and insurance pressure are making the market harder for ordinary buyers than the word “affordable” suggests.

The shareable bottom line is this: Fresno County is still one of California’s more accessible home markets, but the real affordability test now comes after the listing price. Once insurance and financing are added, the advantage looks strongest for cash buyers and investors, while first-time buyers and renters are left doing harder math on thinner margins.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?